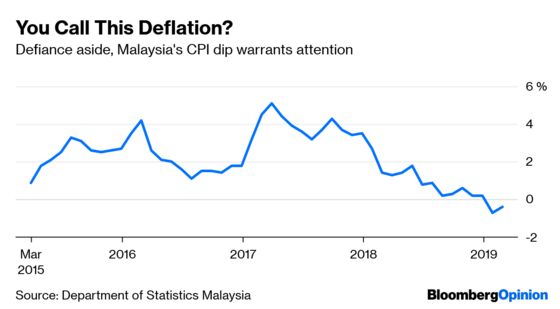

(Bloomberg Opinion) -- Just to be completely clear: There's no deflation in Malaysia.

Don't even think about it happening, Bank Negara Malaysia insists in its annual report. Categorically, there is no risk, Governor Shamsiah Yunus told reporters Wednesday. The two consecutive declines in the consumer price index aren't indicative of a broad-based, sustained decline in prices or a jarring collapse in demand. And most components of the CPI basket are in the black, not red.

Public enemy No. 1. Right. Got it.

Leaving aside whether she doth protest too much, Shamsiah's emphasis is a sign of the times. Inflation is also coming down across East Asia, as in much of the world. Federal Reserve Chairman Jerome Powell has called the struggle with entrenched low inflation “one of the major challenges of our time.” When I asked Shamsiah for her perspective on Powell's sense of mission, she was broadly in agreement. Inflation will average 0.7 percent to 1.7 percent in Malaysia this year, compared with 1 percent in 2018.

Being so certain of something not happening is a risky proposition when you are the custodian of an economy. You can't control everything and you certainly can't stand in the way of forces pushing down inflation across the globe.

Shamsiah is in a delicate situation: Malaysia's new/old government has taken stick from the new/new opposition – the same crowd that ran the country for six decades – for the CPI declines. The spooky superlative is that this hadn't happened since 2009. Nobody wants that size and scope.

Shamsiah identifies and concedes the same kind of headwinds cited by Powell, and for that matter, pretty much every central banker: a cooling global scene, trade friction, a downdraft in the technology-manufacturing cycle and volatility in financial markets.

There wasn't much attention given to tailwinds. The implication is that, while there are things that can support growth, there isn't a lot that’s likely to speed growth. In this, too, Malaysia is a sign of the times.

One popular narrative Bank Negara isn't buying is that there is no ammunition left for authorities to combat a downturn. “We still have the policy space,” Shamsiah said. In addition to interest rates, fiscal allocations can be redirected if necessary. There are prudential steps that can be taken, too.

The talking points for a rate cut are already in hand. Malaysia hasn't touched its benchmark rate since raising it in January 2018. Rather than wait to be asked, Shamsiah addressed prospects for lower borrowing costs in her opening statement and was pressed (a bit) during Q&A. In the event there is a cut, she said, it won't be because things are dire or the bank has reassessed its certainty on deflation. It's all about risk management, what Shamsiah called the “interplay” of global and local factors.

On the last point, it could have been Powell in front of the cameras. Malaysia is firmly in the mainstream. The big contours of the economic landscape reflect forces beyond national boundaries. The differences are in the shading.

The last time I sat in the briefing room at Bank Negara was March 1998, and I was Bloomberg News’s bureau chief in Kuala Lumpur. The Asian financial crisis had begun nine months earlier. The worry then was whether interest rates were high enough to stem capital flight and prevent the ringgit’s slide fueling a surge in inflation.

That conversation belongs in a museum. Good thing there's zero chance of deflation.

Now, about that rate cut …

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.