(Bloomberg Opinion) -- Investing legend Sir John Templeton said that bull markets are born on pessimism, grown on skepticism, mature on optimism and die on euphoria. Whether markets are in the optimistic or euphoric phase is certainly debatable, but there's no debating that investors are feeling better now about the outlook than any time since mid-2014 — and it's probably justified.

That's seen in a custom Bloomberg index that combines 18 indicators tracking equities, bonds, currencies, commodities, volatility and liquidity calibrated back to the financial crisis to measure whether markets are in a "risk-on" or "risk-off" mode. The gauge just surpassed its previous high of the year set in late January and its high before that in June 2015. Yes, late January was when risk assets took a nasty tumble and the same thing goes for mid-2015, so there's a case to be made for too much complacency having crept back into markets. But it’s understandable, given that markets have weathered many events that just a few months ago were seen as potential triggers for a bear market, or at least some pretty major headwinds. The strategists at BNY Mellon say those events included doubts over a soft Brexit, the renegotiation of the North American Free Trade Agreement, Italian politics, an escalating trade war between the U.S. and China and turmoil in such emerging markets as Turkey. Of course, these issues aren't resolved, but almost nobody expects the worst case scenarios that were predicted just a few months ago will come to pass.

“The beginning of this summer saw a number of extremely well-flagged risks come into focus for investors," Simon Derrick, the chief currency strategist at BNY Mellon, wrote in a research note Tuesday. "The cumulative effect was that the market collectively — and understandably — positioned itself for risk aversion over the summer. However, since mid-August one of the defining themes has become the often muted market reaction to fresh developments." To Derrick, this all suggests that investors were positioned defensively. If true, then the recent strength in riskier assets may have some legs as investors unwind some of those defensive positions and take more risk.

TURMOIL TEMPERED

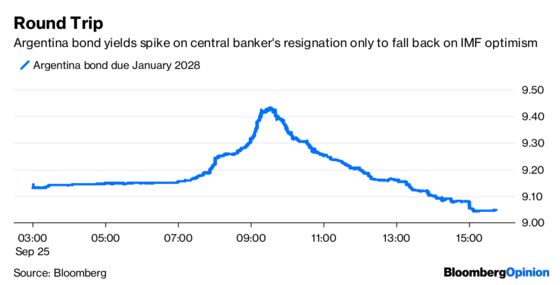

Argentina and Brazil are prime examples of the improving sentiment toward risk assets. On Tuesday, seemingly negative news events — at least for investors — were quickly digested and dismissed, which is something that wouldn't have happened a month or two ago. In Argentina, markets were quickly thrown into disarray after central bank president and former JPMorgan and Deutsche Bank trader Luis Caputo stepped down after only three months on the job, and with the country still in tense negotiations with the International Monetary Fund for much-needed funds. Yields on the country's bonds due in January 2028 went from about 9.15 percent to as high as 9.44 percent before reversing and dropping below 9.10 percent. In Brazil, the real opened lower and fell as much as 1.23 percent after the latest presidential election survey showed that leftist candidate Fernando Haddad gained ground less than two weeks before voters head to the polls. Haddad is the heir to former President Luiz Inacio Lula da Silva, who is serving jail time for corruption. But then, the real reversed those losses and was higher in late trading. For many investors, it's hard to see emerging-markets getting much worse after more than four-month-long selloff. Even with the turmoil, the Organization for Economic Cooperation and Development this week said it was trimming its estimates for global economic growth this year by just 0.1 percentage point to 3.7 percent and by just 0.2 percentage point in 2019 to 3.7 percent. Morgan Stanley has removed its “bearish call” on the fixed income and currencies of developing countries and Standard Chartered says emerging markets are the cheapest in 10 to 15 years, according to Bloomberg News's Yumi Teso.

BOND BEARS CALMED

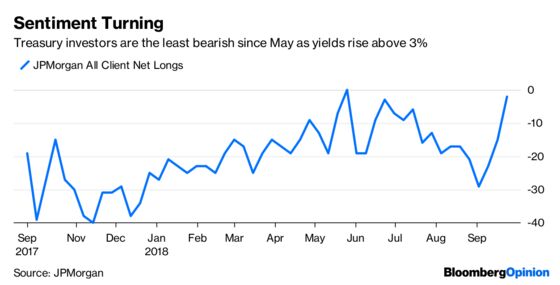

There hasn't been a lot for bond traders to be happy about lately. Yields on benchmark 10-year Treasury notes have surged in recent weeks, reaching as high as 3.11 percent on Tuesday, less than two basis points from their highest since 2011. As everyone knows — or should know — yields move inversely to bond prices, which means prices have been going down. As such, the Bloomberg Barclays U.S. Treasury Index has lost 1.07 percent in September through Monday, the most for a month since it tumbled 1.36 percent in January. It's also now down for the year, losing 1.80 percent. About the best thing that can be said about the bond market these days is that traders are getting less bearish. The widely followed JPMorgan Chase & Co. weekly survey of sentiment toward U.S. Treasuries rose to -2 from -15 on Sept. 17. Sentiment has improved for four straight weeks, and the only better reading this year was in May, when it came in at zero. If that doesn't move you, then consider that 21 percent of respondents say they expect Treasuries to rally, the most since the start of July and above the long-term average of 16 percent. Conversely, just 23 percent expect the market to fall, matching the lowest since last September. One of the things that the bond bulls believe is that higher rates will weigh disproportionately on businesses and consumers, who have accumulated a record amount of debt since the financial crisis.

BREAKING OUT

The euro has become one of the most intriguing currencies in the global foreign-exchange market, shrugging off political intrigue in Italy to rally to its highest level since early May, as measured by the Bloomberg Euro Index. Much of the recent gains are the result of some hawkish talk by European Central Bank officials. For example, ECB President Mario Draghi told the European Parliament in Brussels on Monday that there’s a “relatively vigorous” pickup in underlying euro-area inflation. Such talk has investors increasing bets that the ECB will soon start boosting policy rates up from near zero while pulling back on bond purchases, both of which should firm up support for the euro. And if those wagers continue, it's not absurd to think that the currency could go much higher. That's because, as Bloomberg News's Todd White and Richard Jones reported, hedge funds and other large speculators have been adding to their euro short positions, reaching a 19-month high in August as measured by Commodity Futures and Trading Commission. The more the euro strengthens, the more costly it becomes for these hedge funds to maintain their bearish bets. At some point, they will likely be forced to unwind those trades, putting further upside pressure on the currency. “A short squeeze is certainly possible,” said Craig Erlam, senior market analyst at online trading firm Oanda Corp. “A lot of what can hold the currency down appears to have been priced in, be it an economic slowdown, trade war risks, Brexit negotiations or emerging-market volatility.”

$100 OIL IN SIGHT

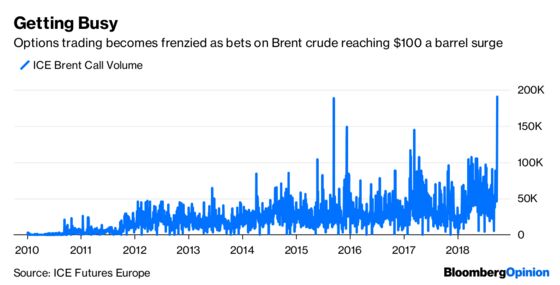

U.S. President Donald Trump took another swipe at OPEC on Tuesday, saying in an address to the United Nations General Assembly that the cartel and its allies "are as usual ripping off the rest of the world.” In short, he wants OPEC to ramp up production and set oil prices lower. But the real issue is that new U.S. oil sanctions against Iran will curb production, helping to spurt prices. Brent crude has just risen back above $80 a barrel for the first time in four years, and the options market shows increasing bets that prices will reach and exceed $100 fairly soon. Contracts equivalent to more than 28 million barrels of Brent crude oil traded on Monday that would profit a buyer from the global benchmark rising above $100 a barrel in the next six months. They included 10 million barrels betting that Brent would top $110 by the end of November and 11 million barrels that it would surpass that level by the end of next month, according to Bloomberg News's Alex Longley. There were more than two bullish call options traded for every bearish put, as call trading surged to a record 191 million barrels, according to Intercontinental Exchange data. Rising oil prices have the potential to either act as a drag on growth or add to inflation, depending on the strength of the economy. Neither would be a welcome scenario.

TEA LEAVES

Most everybody expects the Federal Reserve to raise interest rates Wednesday for the eighth time since December 2015, boosting its target for the federal funds rate to a range of 2 percent to 2.25 percent from the current 1.75 percent to 2 percent. The real action will be the Fed's updated Summary of Economic Projections, which shows how fast the central bank expects the economy to grow. as well as its outlook for inflation. As veteran Fed watcher and Bloomberg Opinion columnist Tim Duy wrote Friday, the trajectory of the economy suggests that the so-called SEP will lean slightly more hawkish than the last round of estimates in June. In line wiht that thinking, a poll of economists conducted Sept. 18-20 showed they expect the Fed to continue its quarterly drumbeat of 25-basis-point increases through June 2019, according to Bloomberg News's Christopher Condon and Catarina Saraiva. That’s a more aggressive pace of hikes over the coming months than Fed watchers anticipated in June, when they predicted policy makers would skip a move at its December meeting. Such a pause won’t come until next September, economists now say.

DON'T MISS

Emerging-Market Rebound Depends on China, India: Komal Sri-Kumar

Europe Has a Pretext To Challenge the Dollar: Leonid Bershidsky

When Pot Smoke Clears, Old Hands May Hold Profits: Nir Kaissar

Argentine Banker's Exit Hints That IMF Pact Is Near: Daniel Moss

Matt Levine's Money Stuff: Maverick Contrarian Bears Are Lonely

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.