China’s Claims on Trade With U.S. Don’t Add Up

Beijing says its current relationship with the U.S. plays to comparative strengths, but the future is another matter.

(Bloomberg Opinion) -- China has marked the latest ratcheting-up of trade tensions with a misplaced history lesson.

Far from worrying about its economic role in the world, the U.S. should recognize just how well the two nations already support each other, according to a white paper released by China’s State Council:

China-U.S. bilateral trade has a strong complementarity. The U.S. stands at the mid- and high-end in global value chains and it exports capital goods and intermediary goods to China. Remaining at the mid- and low-end in global value chains, China mainly exports consumer goods and finished products to the U.S. The two countries play to their comparative strengths and the two-way trade is highly complementary.

I’ve argued frequently in recent months that the Trump administration’s push for a trade war with China is misguided and likely to fail, lacking in compelling justifications, and driven by a dangerous radicalism. At the same time, Beijing’s going to need to do better than this to defend its position.

The white paper seems to restate a trade model developed by Swedish economists Eli Heckscher and Bertil Ohlin in the early 20th century. Countries with a lot of capital and land (such as the U.S.) will specialize in exports of capital- and land-intensive goods, such as advanced manufacturing, services, agricultural produce and materials. Those with a big work force, like China, will focus on labor-intensive products like consumer goods and basic manufacturing.

That’s a good description of the bilateral relationship that developed over the past two decades. The trouble is, both sides expect the coming years to be very different.

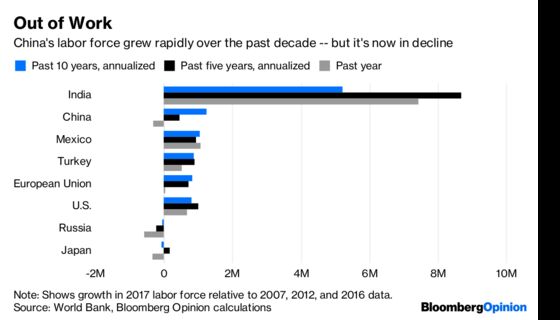

For one thing, China’s labor boom is coming to an end. Its workforce fell last year for the first time in five decades, putting it alongside Russia, Japan, Italy and Spain as one of the handful of major economies with a shrinking employment pool. Over the past five years, the U.S., Turkey, Mexico and the European Union — not to mention more than a dozen developing countries — each added more workers than China. That won’t change the fact that China still hosts more than a fifth of the world’s labor force, but it illustrates how its economy is changing.

Capital is shifting in a similar way. China’s stock overtook that of the U.S. in 2012, according to data compiled by the University of Groningen, and has continued to grow ever since. Even adjusting for the size of its population, the shift has been dramatic: In 2000, the U.S. capital stock per person was about 12 times the level in China. By 2014, the ratio had fallen to about three times. China’s investment boom in 2016 and 2017 may well have led that ratio to slip further.

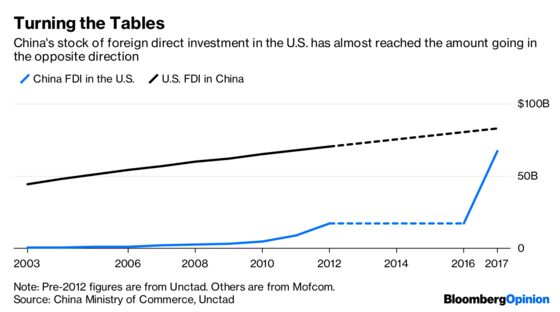

One figure in the State Council’s white paper — foreign direct investment — illustrates that the issue isn’t so much the history of China's complementary relationship with the U.S., but the future of its growing wealth and looming demographic changes. Both factors upend the very model Beijing proposes.

In 2003, Chinese foreign direct investment in the U.S. was just $65 million, little more than a rounding error.This makes sense — after all, the People’s Republic was a developing economy seeking investment from richer nations.

Since then it’s changed dramatically. Having hit $17 billion at the end of 2016, it jumped to $67 billion a year later, according to Ministry of Commerce data. That’s on a trajectory to overtake the sum invested by the U.S. in China, which came to $83 billion in 2017.

Many of Beijing’s actions that most annoy Washington — its high-tech foreign acquisitions, or the desire to upgrade manufacturing expertise through the Made in China 2025 program — are ultimately attempts to offset the gradual decline of China’s labor force with a shift toward higher value-added, capital-intensive products. That desire is perfectly understandable, but so is the alarm in rich countries. In moving up the value chain, China switches from being a complementary partner to a competitive rival.

That moment could still be some years off. While its capital stock per head has grown rapidly, the level still leaves China a middle-income country on a par with Mexico and Russia, and somewhat behind Brazil.

Even so, it’s little wonder that both the U.S. and China have an eye on more distant prospects — and disingenuous of Beijing, given its ambitions of global leadership by 2050, to put so much focus on a model that peaked a decade ago.

The world’s primary exporters of capital-intensive goods — and, ultimately, capital itself — have always been powerful. When the U.K. and its empire passed that baton to the U.S. in the wake of World War I, their shared culture and the trauma of European conflict eased the transition.

To make this next shift easier, the U.S. needs to accept that it’s inevitable. But China also needs to be honest about what’s happening. Focusing on a past Beijing is desperate to escape won’t inspire confidence in the partners China needs to support its rise.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.