(Bloomberg Opinion) -- Emerging markets are in a bad way. The MSCI EM Index of stocks fell Tuesday to bring its decline to 18.4 percent since peaking in January. MSCI’s index of EM currencies is down 8.51 percent since April. If that isn’t depressing enough, Morgan Stanley predicted in a research report Monday that it will only get worse for investors. Everyone seems to be talking “contagion” — perhaps prematurely.

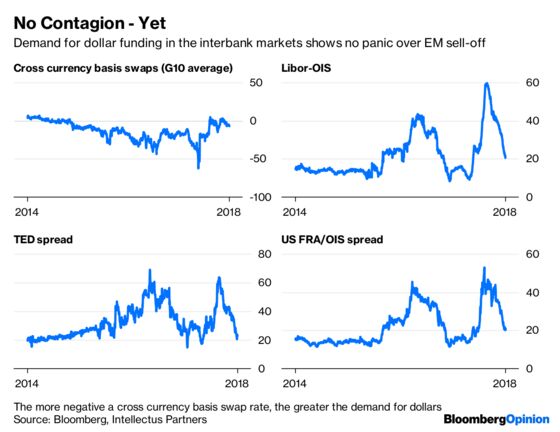

If your definition of contagion is an asset class that is getting battered regardless of the fundamentals, then the gut-wrenching slump now engulfing EM would qualify. But if you’re old school and contagion means something that spreads into a global crisis that threatens the economy and financial system by catching a few key hedge funds napping, then you can relax. That can be seen in the interbank-funding markets. In a true crisis, demand for dollar funding among financial institutions would skyrocket if they thought that one — or more — of their own was in trouble. And yet Intellectus Partners’ chief economist Ben Emons points out that the cost to convert foreign cash flows into dollars with cross-currency basis swaps has barely budged and actually shows less demand for dollars relative to last year. It’s also notable that other measures of stress, such as the so-called TED spread, which measures the gap between the London interbank offered rate for dollars and U.S. Treasury bill rates, has shrunk to its lowest level of the year along with the Libor-Overnight Index Swap spread.

Even a decade after the worst financial crisis since the Great Depression, investors are prone to caution by selling first and asking questions later. That’s a good thing, especially with estimates from the Institute for International Finance that dollar-denominated debt in 21 major emerging-market economies has surged to about $6.4 trillion from $2.8 trillion in 2008. And while it’s possible the EM slump could eventually infect the global financial system, the sell-off at this point looks more like a repricing of the strong rebound in 2016 and 2017 that followed the much deeper, more painful EM rout of 2014 and 2015. “Global markets so far see (the EM problems) as local issues without systemic implications, but the risk for broader contagion through the global financial system is certainly there,” Emons wrote in a research note.

SELF-INFLICTED WOUNDS

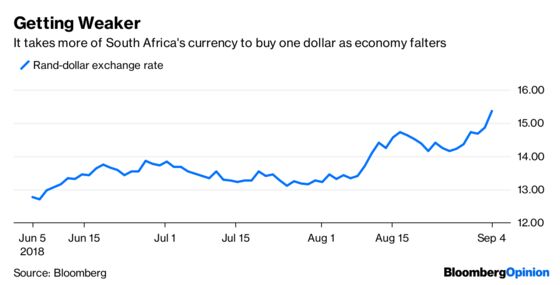

Such sentiment is little solace to investors in South Africa. That country led EM financial assets lower on Tuesday after government data showed that Africa’s most-industrialized economy has entered into its first recession since 2009. The news pushed the country’s currency, the rand, down as much as 3.56 percent toward its weakest level in more than two years. South Africa’s government bonds fell the most in nine months as investors assigned greater odds that Moody’s Investors Service would cut the country’s local-currency debt rating to below investment grade, or junk, according to Bloomberg News’s Robert Brand and Colleen Goko. The nation’s benchmark stock index tumbled 1.40 percent. And yet, as Emons suggests, much of South Africa’s problems are self-inflicted. The economic slowdown casts a pall over the country’s new leadership, providing an uncomfortable parallel with the initial nine years of former President Jacob Zuma, who was succeeded by Cyril Ramaphosa in February, Bloomberg News reports. Ramaphosa’s rise to power since December initially boosted sentiment and the rand after Zuma’s tenure. That optimism faded as economic reforms weren’t implemented fast enough. “We are in desperate need for policy certainty and structural reform to get us onto a growth path,” Elize Kruger, an economist at NKC African Economics, told Bloomberg News.

ITALY’S OUTLOOK BRIGHTENS

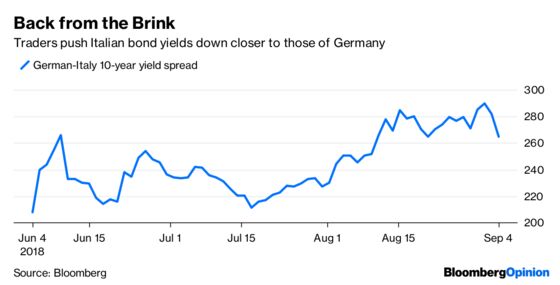

It wasn’t too long ago — just a few weeks, in fact — that investors were on edge over Italy. The nation’s financial markets took a tumble as its new government suggested it may ramp up spending to juice the economy and take the country out of the euro zone. With some $2.28 trillion of government debt, investors were right to be concerned that there was a chance, however slim, that they might be paid back in devalued liras rather than euros. But now it’s looking as if such talk was just posturing. The League, one half of the populist coalition running Italy, aims to send a reassuring message about its spending plans and is discussing a 2019 budget deficit below 3 percent of GDP, according to Bloomberg News’s Lorenzo Totaro and Alessandra Migliaccio. Investors reduced the yield on Italy’s 10-year bonds to within 2.70 percentage points of similar German bunds, from 2.91 percentage points on Friday even though Fitch Ratings downgraded its outlook on Italy that day to negative from stable citing budget concerns. Italy’s FTSE MIB index rose as much as 1.2 percent on Tuesday. Strategists at Citigroup Inc. wrote in a report that they are constructive on the Italian stock market. “Overall, it is likely to be an uptrend bumpy ride,” the strategists wrote, according to Bloomberg News.

HISTORY FAVORS BULLS

The performance gap between U.S. and non-U.S. stocks keeps getting wider. While the MSCI All-Country World Index excluding the U.S. was down about 0.90 percent in late trading, the MSCI USA Index was down a more modest 0.15 percent. The U.S. index has gained 7.66 percent since late May while the rest of the world has dropped 3.44 percent. This begs the question of whether the rest of the world will ultimately drag U.S. equities lower or whether the rest of the world will play catch-up to the U.S. The strategists at Bank of America Merrill Lynch wrote in a report late last week that there’s scope for non-U.S. assets to rebound, given they are underperforming the most since the financial crisis and given that the global economy seems to be in decent shape. But before investors adjust their portfolios, they should consider that history suggests there are more gains ahead for U.S. equities despite September generally being the cruelest month for returns. LPL Senior Market Strategist Ryan Detrick points out that before this year, the S&P 500 has been higher each month from April through August only five times since 1950. Each of those times, the final four months of the year were higher, with gains ranging from 8.2 percent in 2017 to 15.6 percent in 1958. “This summer rally has caught many investors flat-footed, but they may want to consider that more strength could be coming, if history is any guide,” Detrick wrote in a research note Friday.

DOLLAR FALLOUT

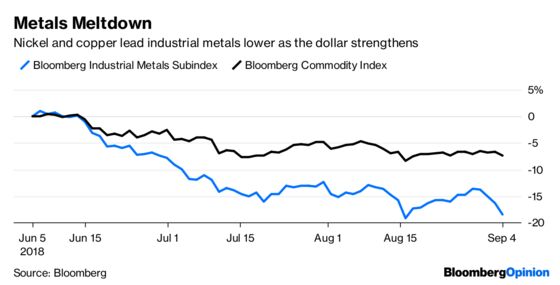

The rising dollar has been blamed for much of the ills in emerging markets of late. The thinking goes that EM borrowers who took out dollar-denominated debt will have a much harder time paying back those obligations as the greenback rises. But dollar strength is also wreaking havoc with commodities, especially base metals. The Bloomberg Industrial Metals Subindex fell again Tuesday, bringing its decline since early June to 19.2 percent. Those commodities are largely traded in dollars, so the currency’s strength tends to make them more expensive, denting demand. By comparison, the broader Bloomberg Commodity Index is down just 7.39 percent. Nickel hit a seven-month low as inventories rose, while copper dropped to its lowest level in 12 days. China is a big user of base metals, which it needs to feed its growing economy, the largest in the world after the U.S. Commodity traders, though, are on edge because they are worried that a budding trade war between the U.S. and China will curb demand. President Donald Trump is expected to impose tariffs on as much as $200 billion of additional Chinese products as soon as Thursday. The clock is ticking.

TEA LEAVES

There’s a good chance that Trump will be tweeting on Wednesday about how other countries have long taken advantage of the U.S. when it comes to trade. That’s because the Commerce Department is projected to say that the U.S. trade deficit expanded in July by the most since March 2015, widening by $3.9 billion to $50.2 billion. That would follow a $3.16 billion widening in June and mark the biggest back-to-back expansion in the deficit since late 2016. Bloomberg Economics describes the widening as payback for a strong second quarter, when exports surged, most likely in response to foreign consumers stockpiling goods in advance of retaliatory tariffs on U.S. products.

DON’T MISS

We May Be Facing a Textbook Emerging-Market Crisis: Satyajit Das

Turkey Missed Its Chance to Stop This Emergency: Marcus Ashworth

Argentina Needs Expanded Help From IMF: Mohamed A. El-Erian

Economists Gear Up to Challenge the Monopolies: Noah Smith

What Happens After China Surpasses the U.S. Economy: Daniel Moss

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.