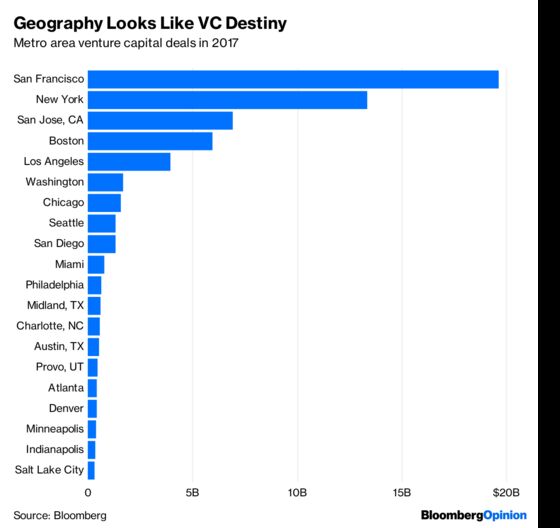

(Bloomberg Opinion) -- The U.S. high technology industry looks like it may be too concentrated. One sign of this is the lack of geographic diversity in the venture capital industry, which is highly concentrated in a few technology hubs, mostly on the coasts:

In 2017, three metro areas — San Francisco, New York and San Jose, California — took about two-thirds of the investment for the top 20 cities. Their share of the top 10 cities has actually increased since 2015, driven in part by super-sized late-stage financing rounds for companies like WeWork Inc., Uber Technologies Inc., and Lyft Inc.

There are a few signs that VC is starting to look beyond the traditional hubs in its quest for returns. In 2015, Bloomberg recorded VC deals in 119 metro areas; by 2017, that number was up to 141. New startup hubs like Columbus, Ohio, and Indianapolis are getting more attention. But more needs to be done to accelerate the spread of venture investment.

Technology industries are increasingly important in the U.S. Not only is tech disrupting older sectors — “software eating the world,” as the famous saying goes — but the U.S. is becoming more specialized in high-technology products as lower-end manufacturing has moved to countries such as China. The move into high tech brings great promise — economist Enrico Moretti estimates that tech boosts a region’s wealth much more than other industries, by drawing in more money and spreading it around an area. But it also carries a danger — the possibility that superstar cities like San Francisco and New York will become ever richer, while the vast majority of the country’s regions are left to languish.

Venture capital isn’t absolutely necessary for the development of a local tech industry — big tech companies that no longer have any need for early-stage financing can choose to move to areas that VCs shun — but in practice it’s very important. Startup companies want to locate close to their sources of financing. Research has documented the historical tendency for startups to perform better when they’re located in areas with lots of VC. Companies that move to Silicon Valley, for example, have historically outperformed those that stayed behind.

Meanwhile, big tech companies generally prefer to locate in places with lots of startups, which they can acquire, and whose engineers they can hire away. The likelihood of acquisition only increases the incentive for startups to move to tech clusters, creating a snowball effect that can greatly enrich a tech hub, but which is distinctly unhelpful for the large number of regions that lose out.

As worries about regional inequality intensify, there have been growing calls for venture capital to spread out, especially to the Rust Belt. The argument is that if VCs look beyond traditional tech centers for funding, industry will follow.

So how can VC dollars be lured out of traditional tech hubs? Back in 2007, Carole Carlson and Prabal Chakrabarti of the Federal Reserve Bank of Boston interviewed a number of VC leaders and recipients of VC funding, in an attempt to answer exactly this question.

Carlson and Chakrabarti’s interviews suggest that VCs were more likely to invest in secondary cities — those that aren’t traditional VC hubs — when those cities have a more established investor presence and when historical returns in those cities had been good. Obviously, both investor presence and historical returns are even stronger in traditional investment hubs, illustrating why moving is hard.

There are plausible psychological reasons for these VC biases — fear of missing out, herd behavior or the tendency to assume that future returns will mirror historical ones. But to some degree, they probably also reflect rational concerns. As startups get larger, they need to hire large numbers of competent managers. But in secondary cities, most managers will have experience in non-tech industries, and that experience may not translate well. Additionally, secondary cities may have staid, cautious cultures that produce employees less eager to disrupt traditional business models.

What can secondary cities do to overcome VC’s caution? Carlson and Chakrabarti’s interviews suggest five main policies. First, cities and their corresponding state governments should invest in upgrading their local universities, in order to produce a pool of talented engineers and managers. In addition, they should encourage local investors to become angels, creating the nucleus of a local investor community. They should improve access for VCs, with good airports and quality hotels. They should boost quality of life with appealing downtowns, while investing in the arts. And perhaps most importantly, they should focus on narrow clusters — such as biotechnology, robotics or agricultural software — instead of trying to become the next Silicon Valley. This latter approach, which has been used by cities like Pittsburgh, not only harnesses clustering effects, but probably helps with marketing as well.

As for VCs themselves, they should try to overcome their own biases against striking out on their own and trying out new locations. This could be good not just for the nation, but for their own returns as well. Research finds that the benefit of startups locating in Silicon Valley has faded since 2001. And while top VC firms tend to outperform the public markets, the rest don’t do so well. Staking out virgin territory in the Midwest or the South might be exactly the thing many smaller VCs need to strike gold.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.