The Dollar Is Losing Its Mojo at the Wrong Time

U.S. is on a borrowing binge to pay for trillion-dollar federal budget deficits and any weakness in dollar should be concerning.

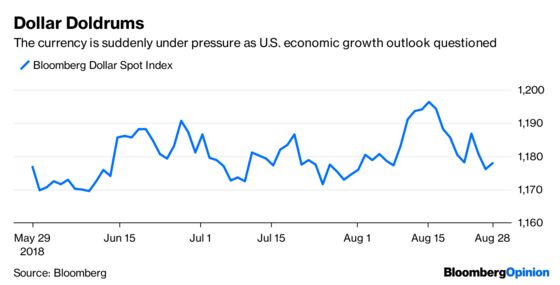

(Bloomberg Opinion) -- What’s wrong with the dollar? Barely two weeks ago the Bloomberg Dollar Spot Index reached its highest since June 2017. President Donald Trump tied the strength to confidence in the U.S., boasting in a tweet on Aug. 16 that “money is pouring into our cherished DOLLAR like rarely before.” But since then the greenback dropped as much as 2.2 percent, reaching its lowest of the month on Tuesday before recovering to end the day slightly higher.

At a time when the U.S. is embarking on a borrowing binge to pay for trillion-dollar federal budget deficits, any weakness in the currency should concern the government. After all, foreigners might have second thoughts about lending money to the U.S. if they expect the dollar to depreciate. That could cause borrowing costs to rise regardless of whether the Federal Reserve raises interest rates or not. NatWest Markets strategist James McCormick has identified six primary reasons for the dollar’s recent downturn, ranging from Trump’s recent criticisms of the Fed’s tighter monetary policy to moves by China to keep its currency from getting any weaker. But perhaps the most intriguing reason is the notion that U.S. economic growth has peaked and will only slow. Although McCormick noted in his report dated Aug. 25 that the U.S. economy is in good shape, a growing number of strategists are starting to point to data showing reports coming in softer than forecast.

Citigroup Inc.’s economic surprise indexes show that not only has U.S. data largely missed estimates this month, they are missing by the greatest degree since September 2018. As such, the currency strategists at Deutsche Bank AG and Goldman Sachs Group Inc. both say they see limited upside for the dollar for now.

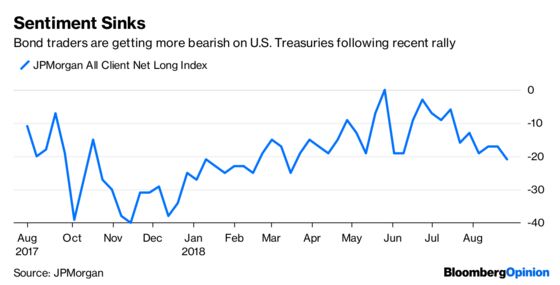

BOND SENTIMENT SOURS

Benchmark 10-year U.S. Treasury note yields closed last week at 2.81 percent, their lowest since May, amid a heated debate over whether a speech by Fed Chairman Jerome Powell — in which he said “there does not seem to be an elevated risk of overheating” — leaned dovish. But the bond market reversed swiftly this week, with yields rising to 2.88 percent in late trading Tuesday. Does that mean bond traders are having second thoughts about whether Powell may be leaning toward ending interest-rate hikes sooner rather than later? Maybe, but perhaps the better explanation is that the bears are taking advantage of the rally to set up short positions at what they think are more attractive levels. A widely followed JPMorgan Chase & Co. survey released Tuesday showed that bond traders are the most bearish since March. Its so-called All Client Net Long index slid to negative 21 from negative 17 in the week ended Aug 21. The economists at Goldman Sachs Group Inc. emboldened the bears by reiterating their call that that the Fed will boost rates two more times this year and four times in 2019. In a report Monday, the Goldman economists emphasized Powell’s nod to a recent Fed study that indicated it would be ill-advised for the central bank to ignore low unemployment and slow the pace of rate hikes, Bloomberg News’s Liz Capo McCormick reported.

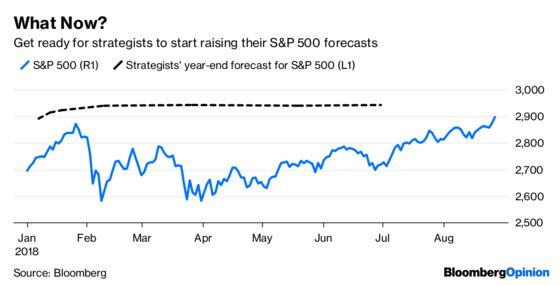

WHAT NOW FOR STOCKS?

One day after setting a record, the S&P 500 Index topped that by posting yet another high. The benchmark closed at 2,897.52, putting it less than 2 percent away from the 2,950 median year-end estimate of 25 strategists surveyed by Bloomberg News at midyear. But rather than recommending investors get defensive, get ready for strategists to get even more bullish and start boosting their year-end estimates as soon as they get back from their summer vacations — if they haven’t done so already. DataTrek Research co-founder Nicholas Colas nicely summed up the general sentiment toward stocks in a note to clients on Tuesday. “As long as you believe the U.S. economy is in decent shape (we do) and trade/tariff wars will not push the global economy into a recession (we don’t), U.S. stocks are reasonably valued because earnings are strong/rising and interest rates remain low,” Colas wrote, referring in that last point to the 10-year Treasury note yield's seeming inability to rise above 3 percent. At about 18 times estimated earnings, the S&P 500 is cheaper now than it was back in January, when the ratio reached almost 19 times, despite the rally in equities. That’s largely due to strong earnings growth. Colas figures the best-case scenario is for the S&P 500 to advance an additional 8.7 percent by the end of the year.

BRAZIL POLITICS MATTER

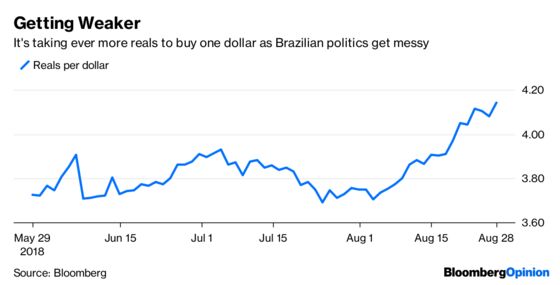

It’s getting ugly in Brazil, where global investors are revolting against the nation’s increasingly unstable political environment. Brazil’s real fell on Tuesday to its weakest level since January 2016. It has lost about 9 percent of its value this month, compared with a more modest 1.40 percent decline in the MSCI EM Currency Index. The nation’s equities are also down for the month and the cost to protect against losses in Brazil’s bonds with credit-default swaps has jumped to the highest since the end of 2016. To understand how crazy Brazil’s politics are, consider that support for former President Luiz Inacio Lula da Silva — currently in jail for a corruption conviction — rose in all three major polls that came out last week, horrifying traders who dread the return of his Workers’ Party to the presidential palace in Brasilia, according to Bloomberg News. If allowed to run, Lula would win a runoff round against all candidates with as much as 53 percent of the ballots, the polls showed. “Brazil remains a paradox,” Sean Newman, a money manager at Invesco Advisers in Atlanta, told Bloomberg News. “In an election where no one seems to care about candidates, all want less corruption but favor the man behind the biggest debacle in the country’s history.”

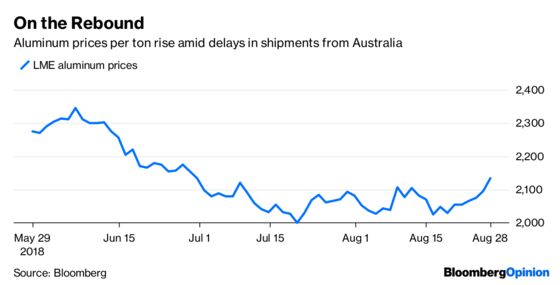

HOT COMMODITY

One of the more important industrial metals is bucking the broad weakness in commodities, with prices rising to their highest since June. The price of aluminum on the London Metals Exchange jumped 1.84 percent on Tuesday to $2,133.50 per ton, extending its gain since mid-month to 5.36 percent. Barring a serious surprise, aluminum prices will rise in August for the first time since May. Meanwhile, the broader Bloomberg Commodity Index is poised for its third consecutive monthly loss. The rebound is being credited to reports of delays in shipments of alumina — the commodity used to make aluminum — from Australia because of a strike at an Alcoa plant and maintenance at producer South32’s Worsley operations, according to Bloomberg News’s Mark Burton. Also, production in China is down amid a general tightness in the market as a result of sanctions against Russia that has curtailed activity at United Co. Rusal. “We view alumina as likely to remain fundamentally tight through the coming months,” Colin Hamilton, a managing director for commodities research at BMO Capital Markets, wrote in a research note.

TEA LEAVES

The U.S. Commerce Department on Wednesday will provide its second estimate of just how fast the economy expanded in the second quarter. Although a big change isn’t expected, with economists forecasting growth of 4 percent, compared with the 4.1 percent that was originally reported on July 27, the report shouldn’t be dismissed. That’s because investors and others will get their first look at economy-wide business profits. Earnings before taxes and excluding profits on inventories and capital accumulation — the measure most closely associated with health in the corporate sector — has flat-lined somewhat recently after rebounding strongly from June 2016 to September 2017, according to Bloomberg Economics.

DON’T MISS

Look Here for One Sign the Bull Market Is Over: Chris Hughes

Copper Fails Miserably as an Economic Forecaster: Stephen Mihm

Trump’s Nafta Deal Is Hardly Worth the Price: Tyler Cowen

Tobacco Smolders as Booze Makers Get Pot Lift: Tara Lachapelle

Venture Capital Could Use Some Geographic Diversity: Noah Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.