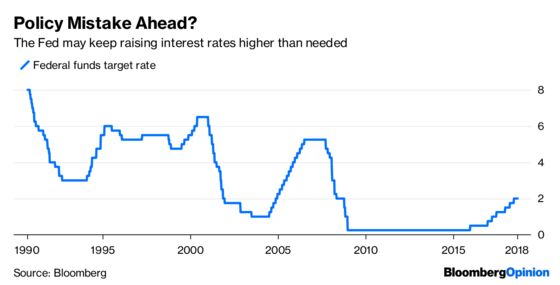

Fed Policy Is to Keep Hiking Until Something Breaks

The central bank is not inclined to take a leap of faith and pause to assess the impact of past rate increases.

(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell took to the podium at the annual Jackson Hole monetary conference, delivering a message of support for the central bank’s policy of ongoing gradual interest-rate increases. This policy stance is less about commitment to estimates of key policy variables such as the natural rate of interest and more about data dependence. Unfortunately, Powell left the unsettling feeling that monetary policy can be summarized as “We plan to keep hiking until something breaks.”

Central bankers center policy on the economic outcomes thought to occur in stable equilibriums. Currently, unemployment and policy interest rates are both below their natural values, while output growth exceeds potential growth.

The values of these variables, however, can’t be observed directly and instead are imprecisely estimated. Focusing too heavily on those estimates can lead to policy errors. Powell highlights the error of the 1970s when the Fed’s estimates of the natural rate of unemployment were too low. The labor market was tighter than the Fed believed and helped contribute to inflation. In contrast, Powell lauded former Fed Chairman Alan Greenspan for recognizing that the natural rate of unemployment had fallen in the late 1990s, allowing for the central bank to hold rates lower as suggested by the Fed’s estimates of the natural rate of unemployment at the time.

Powell uses these episodes to justify the Fed’s current middle-of-the-road policy stance. Facing low rates of inflation and low unemployment, the Fed could simply not boost rates, essentially taking a page out of Greenspan’s playbook. Or, to avoid the mistakes of the 1970s, the Fed could hike more aggressively in response to an unemployment rate that is below the estimated natural rate. Considering the uncertainty about the true levels of these natural or equilibrium values, Powell defends the policy of gradual hikes as appropriate. They don’t want to overreact to either slow inflation or low unemployment.

In short, Powell does not feel beholden to specific estimates of the natural rates of anything. This lack of commitment has important implications for monetary policy. We already knew the Fed was taking its estimates of the natural rate of unemployment with a grain of salt. The Fed would have tightened policy more aggressively if it truly believed unemployment rates below 4.5 percent threatened inflation stability in the near term. But we didn’t know how seriously the Fed would take its estimate of the natural rate of interest. Now we know — Powell probably isn’t taking it as anything other than a loose guideline.

If the natural rate of interest is only a loose guideline, there is not much reason to expect the Fed to automatically pause as they hit that estimate, as suggested recently by Dallas Federal Reserve President Robert Kaplan. Hitting that estimate — sometime after the next three to four 25-basis-point rate hikes — may make policy makers more cautious, but that estimate will be much less important than the actual data flow.

This raises the bar for a pause. Powell and his fellow policy makers need to see a definite change in the numbers that leads them to believe that economic activity has moderated and financial conditions have sufficiently tightened to justify the pause. In other words, they are not inclined to take a leap of faith and pause as they hit neutral to assess the impact of past tightening. They need to see a reason to stop tightening.

The best-case scenario is that the data moderates over the next six to nine months and provides a reason to pause. Essentially, the data tell the Fed its estimate of the neutral policy rate is more or less correct after an additional 75 or 100 basis points of policy tightening. That’s my baseline estimate.

The worst-case scenario is that something actually needs to break before the Fed stops tightening. This is a possibility because of the long and variable lags in the policy process. The Fed could keep on hiking well past when it should stop, or fail to reverse course quickly enough, because the data has yet to catch up with a slowdown already occurring under the surface. This is arguably how expansions end.

Powell would like the Fed to recreate Greenspan’s policy of the second half of the 1990s, which was a time when good judgment trumped commitment to estimates of unknown policy variables. Let’s hope he can pull it off.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Duy is a professor of practice and senior director of the Oregon Economic Forum at the University of Oregon and the author of Tim Duy's Fed Watch.

©2018 Bloomberg L.P.