Market Sell-Off Misery May Have a Silver Lining

The U.S central bank’s steady pace of rate increases is being blamed for contributing to the current market turmoil.

(Bloomberg Opinion) -- It's hard for investors to be optimistic on a day like Wednesday. Global equities fell to their lowest level in more than a month as emerging-market stocks stood on the cusp of a bear market, tumbling 19.6 percent from their January peak. Commodities plunged to their lowest since July 2017 as that widely watched leading indicator — copper — did enter bear-market territory. Credit suffered as yield spreads on corporate bonds widened.

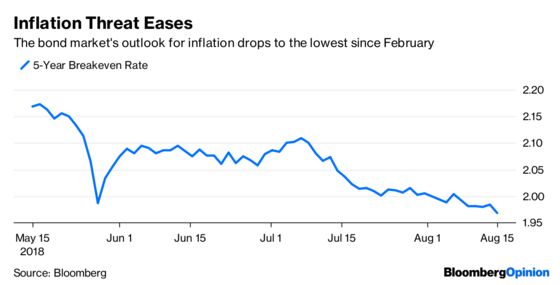

That's all bad, no doubt, but at least faster inflation isn't a concern. Without a whole lot of fanfare, breakeven rates on Treasuries — a measure of what traders expect the rate of inflation to be over the life of the securities — have rapidly declined. For five-year securities, the rate has come all the way down to 1.95 percent, the lowest in six months, from this year's peak of 2.19 percent in May. This is an important development because if the trend continues, it would potentially give the Federal Reserve cover to not raise interest rates next month; that, in turn, could be supportive for global markets. Although that view is definitely in the deep minority, the central bank's steady pace of rate increases — six since December 2016 — is being blamed for contributed to the current market turmoil. Of course, Fed officials may decide that pausing now and not continuing the march to a neutral rate would only add to the criticism that it's beholden to markets, fostering the belief that a central bank "put" is alive and well. To some investors and strategists, that's a small price to pay to keep the decline in markets from becoming disorderly.

"A great showdown is underway between investors and the Federal Reserve over the path of inflation," Ben Breitholtz, a data scientist at Arbor Research & Trading, wrote in a research note Wednesday. "Markets are solidifying their belief headline inflation cannot run above 2.5 (percent) year-over-year for the years to come, much to the dismay of Federal Reserve officials."

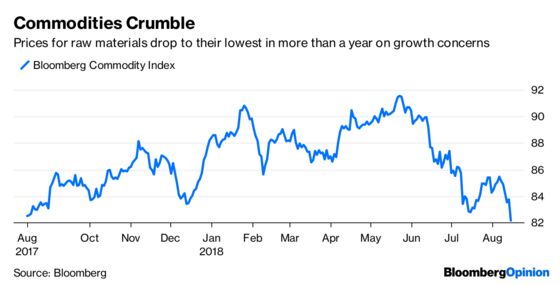

COMMODITIES ROUT

The biggest contributor to the drop in inflation is the price of raw materials. The Bloomberg Commodity Index covering everything from oil to metals and live cattle fell as much as 2.11 percent Wednesday to a one-year low, bringing its decline since this year's peak in May to 10 percent. What's worrisome about the drop is that it’s being led by metals amid growing concern that the turmoil in emerging markets and a budding trade war between the U.S. and its major peers will curb global economic growth. Most contracts in base metal markets fell more than 2 percent in London, with copper sinking below $6,000 as supply concerns eased. Meanwhile, bearish bets outnumbered bullish wagers on 10 of the 18 raw materials tracked by the U.S. Commodity Futures Trading Commission, according to Bloomberg News. “When you look at the broad sell-off across metals, the key drivers are clearly macro factors,” Nicholas Snowdon, a metals analyst at Deutsche Bank AG, told Bloomberg News. Yes, the commodities market had a bigger drop of 11 percent between February and June of last year, but that was more due to supply issues at a time when the global economy was enjoying a synchronized upswing.

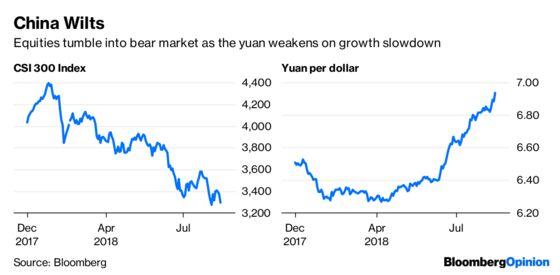

CHINA CONCERNS

The commodities market probably wouldn't be soft if it wasn't for China. The data coming out of the Asian nation, which is the world's largest consumer of raw materials, is sending some very disturbing signals despite the government's vow on Wednesday that it will be able to weather the escalating trade war with the U.S. and achieve its economic targets for this year. Even so, the benchmark CSI 300 Index of equities fell, bringing its decline since late January to 25 percent. The yuan weakened past 6.9 a dollar on Wednesday for the first time since May 2017, extending its decline since mid-April to 9.6 percent. Investors got a reminder of the economic troubles China faces on Tuesday as data showed factory output, retail sales and credit creation in July all trailed estimates, according to Bloomberg News. Chinese policy makers face a difficult balancing act in trying to tackle debt while supporting growth. Fixed-asset investment rose at the slowest pace in two decades during the first seven months of the year, data released on Tuesday showed, while infrastructure spending fell to a quarter of the pace seen a year earlier.

FROM BAD TO WORSE

The Bloomberg Euro Index fell for a second straight day Wednesday. Although not unusual in itself, what's jarring about the move is the magnitude of the decline. The decrease on Tuesday and Wednesday was as much as 1.15 percent, the most over a two-day period since October. In a sign of how troubled the euro zone is, few see the downtrend ending anytime soon, even if the turmoil in Turkey begins to ease. As euro-area growth slows and interest-rate differentials lead investors to unwind bullish euro positions from earlier in the year, Deutsche Bank AG and Nomura International Plc see a possibility the currency will drop to as low as $1.10 from about $1.1350 Wednesday, according to Bloomberg News's Charlotte Ryan and Lananh Nguyen. As recently as April, the euro was trading above $1.24. “I think $1.10 is the next stop, and we are underweight the euro,” Alessio de Longis, an OppenheimerFunds money manager, said in an interview on Bloomberg TV. “It’s this confluence of factors of weakening growth and rising credit risks that makes this a bit of a vulnerable situation.” Options markets show strong demand for longer-term downside exposure, with one-year risk reversals moving to as much as 139 basis points in favor of euro puts, the most bearish sentiment since April 2017.

BOTTOM FOUND?

The S&P 500 Index fell on Wednesday for the fifth time in the last six trading days. Besides showing that U.S. equities are not immune to turmoil in foreign markets, the move provided some good intelligence on where the bottom might be for the benchmark for American equities. The S&P 500 closed at 2,818.37, down 21.59 points, after earlier dipping to as low as 2,802.49. That's an important number because it's the upper end of the S&P 500's support range of 2,790 to 2,800, according to Bloomberg Intelligence. "The 2,800 level proved formidable resistance during the advance, and should likewise prove strong support on correction, suggesting the bulk of the sell-off for the S&P 500 may be complete, at least for the near term," BI equity strategists Gina Martin Adams and Aditya Kalgutkar, wrote in a research note Wednesday. Should the S&P 500 price line break beneath 2,800, the next support is 2,790, the peak of the June advance, which happens to coincide with the 50-day moving average, they added. Even so, for the index to truly regain its footing, the technology sector will need to find some support. In both corrections this summer, tech traded down to its 50-day moving average, and after bouncing around that level, began to rebound. The sector is now just a few ticks above that average.

TEA LEAVES

There's been a lot of concern lately over the health of the U.S. housing market. Mortgage rates are hovering around their highest since 2011 and the Fed this week said that household debt rose to a record $13.5 trillion in the second quarter. At the same time, faster inflation is eating into the meager gains in wages. It's no wonder that an index compiled by the National Association of Realtors shows housing affordability is the lowest since 2008. That's why a government report Thursday on housing starts for August — which includes apartment construction — will likely get more scrutiny than usual. The median estimate of economists surveyed by Bloomberg is for an increase of 7.4 percent after a 12.3 percent drop in June that was the biggest since 2016.

DON'T MISS

Tax Cuts Are Why Bond Yields Aren't Higher: A. Gary Shilling

Turkey's in a Mess. Capital Controls Won't Help: Marcus Ashworth

Libor's Shadow Gives Way to New Overnight Rate: Brian Chappatta

CLOs Are the New Hedge Funds. Plan Accordingly: Stephen Gandel

These ETFs Save Investors a Trip to the Casino: Nir Kaissar

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.