(Bloomberg Opinion) -- That sound you hear is currency traders groaning about having to cancel their August vacations.

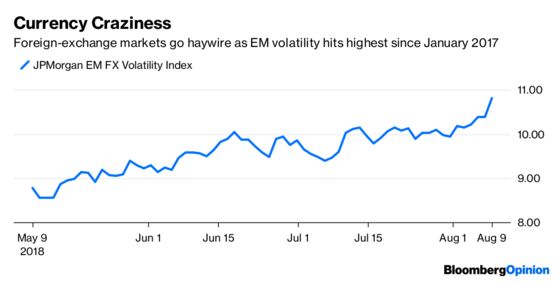

Over the last decade or so, the last full month of summer in the northern hemisphere has become notorious for big, unexpected moves in financial markets. This year, currencies are living up to that reputation.

The Bloomberg Pound Index was poised for its sixth straight decline in late New York trading Thursday, its longest slump since last August. New Zealand's dollar fell the most since October against a basket of developed-market peers. Turkey's lira can't find a bottom, dropping again Thursday to bring its decline for this month to 11.4 percent already. Russia's ruble isn’t far behind, weakening 6.21 percent. On the other side of things, the yen is doing the exact opposite of what Japanese officials want, gaining more than 2 percent since July against its peers and already making August the second-best month for the currency over the past year. And those are just some of the notable moves.

At a time when most are lamenting a drop in cross-asset volatility, a JPMorgan index measuring such gyrations in emerging-market currencies has jumped to its highest since January 2017. The upshot is that more traders are looking to hide out in the dollar, with net long positions in the greenback by hedge funds and other large speculators rising to the highest since early last year, Commodity Futures Trading Commission data show.

The strategists at Credit Suisse summed it up best in a report dated Aug. 8. They wrote that "as far as idiosyncratic themes go, they range from the now relatively mundane and familiar," such as Brexit tensions and the potential for a Bank of Japan policy shift, "to the highly unpredictable," including U.S. sanctions on Turkey and Russia, political upheaval in Brazil and corruption scandals in Argentina, "to the outright bizarre," like when Saudi Arabia this week threatened to dump all its Canadian assets in reaction to a tweet. Whatever happened to the summer doldrums?

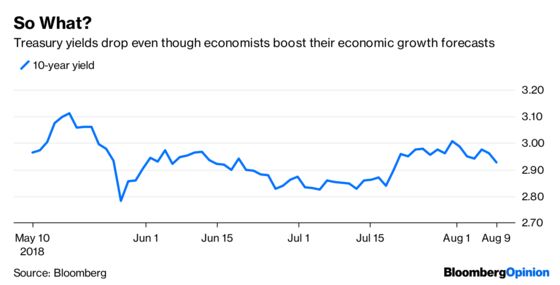

BONDS IGNORE THE DATA, FEDSPEAK

What does the bond market know that economists don't? That seemed to be the question Thursday as yields on 10-year Treasuries fell to 2.92 percent, the lowest since July 20. Bonds rallied even though a monthly Bloomberg survey showed that economists raised their U.S. third-quarter growth forecasts to 3 percent, from 2.8 percent as of July. Also, Chicago Federal Reserve President Charles Evans said the central bank may need to raise interest rates to “somewhat restrictive” levels to combat the effects of recent fiscal stimulus on the U.S. economy. “It would not surprise me at all if we make a judgment to move to a somewhat restrictive setting,” Evans said, defining that as roughly half a percentage point above his 2.75 percent estimate of neutral. Those were hawkish comments from one of the Fed's most reliable doves, says Bloomberg News's Matthew Boesler. Economists now see the target for the federal funds rate rising to 3 percent in the second quarter of 2020, from the current range of 1.75 percent to 2 percent. But there's a logical explanation for the bond market's seemingly sanguine reaction. No one is saying that inflation is in jeopardy of getting out of hand, and higher rates would only keep inflation expectations in check. That's good news for bond markets.

SMALL IS STRONG

While most investors are keeping a close eye on the S&P 500 Index to see if it can finally break above the records seen in January — it was only about 0.4 percent away in late trading Thursday — one part of U.S. equities market keeps setting new all-time highs. The S&P Small Cap 600 index inched up 0.08 percent on the day, bringing its advance for the year to 13.6 percent. That's double the gain of the S&P 500. With companies representing about 75 percent of the S&P 600's market capitalization having reported second-quarter results, earnings for the index are on pace to rise 36 percent from a year earlier, the fastest rate in over seven years, according to Bloomberg Intelligence. The big jump in profits has led to a 12.5 percent increase in earnings estimates for the year — and the swift rise in analysts' expectations has in turn suppressed earnings multiples, causing an 8 percent drop in the S&P 600's 12-month forward price-to-earnings ratio since late January, according to Bloomberg Intelligence. The index now trades at 18.5 times expected earnings, more than 3 percent below its five-year average. Who said stocks aren't a bargain?

RUSSIAN BONDS PLUNGE

Traders are of the opinion that new U.S. sanctions placed on Russia will have real consequences for the latter's economy. Not only has the ruble tumbled — dropping to its weakest level since 2016 — but perhaps more importantly, Russia's bond market has fallen out of bed, pushing up borrowing costs. Russian 10-year yields have risen about a third of a percentage point over two days in the biggest move since the last bout of penalties in April, according to Bloomberg News's Alex Nicholson. At 8.2 percent, the yield is the highest since March 2017. To be sure, analysts say President Vladimir Putin’s efforts to protect Russia after past rounds of sanctions have left the economy more insulated, according to Bloomberg News's Anna Andrianova. Data due as early as Friday will show gross domestic product added 1.9 percent last quarter from a year earlier, compared with 1.3 percent in the first three months, according to the median of 20 forecasts in a Bloomberg survey. Russia has countered sanctions by revamping fiscal and monetary policy, channeling extra income into a sovereign wealth fund and unloading most of its holdings of U.S. Treasuries, Andrianova reports. That's made Russia is less vulnerable to outflows of foreign capital than some of its embattled peers such as Turkey.

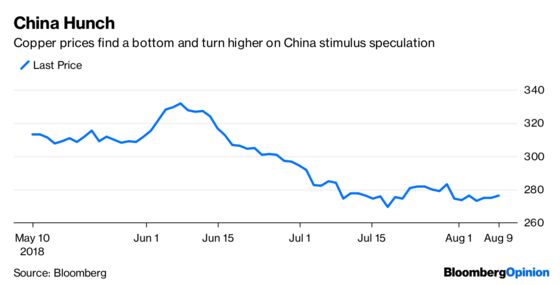

COPPER'S CHINA HOPES

The economic data out of China this month paints a picture of an economy that continues to slow. That’s not what Chinese officials desire at this time, given the budding tit-for-trade trade war with the U.S. So, are they about to roll out some more stimulus measures? The copper market sure thinks so. The metal rose on Thursday as support continues to build following a 19 percent plunge over a period of six weeks in June and July. It's now up 2.6 percent from last month's low on July 19. “The market is betting on China once again stepping in and coming to the rescue,” Ole Hansen, the head of commodity strategy at Saxo Bank A/S, told Bloomberg News. “With China having such a huge impact on industrial metals demand, any push to increase stimulus would have a dramatic effect on prices.” China confirmed it will impose a 25 percent tariff on scrap copper imports from the U.S., raising the possibility that China will have to import more refined metal, according to Bloomberg Naws's Mark Burton. Goldman Sachs Group Inc. said a looming strike at the Escondida mine in Chile could also lift prices.

TEA LEAVES

A slow week for U.S. economic data will end with a bang. On Friday, the Labor Department will release its closely watched report on consumer price inflation. The median estimate of economists surveyed by Bloomberg is for a 2.3 percent rise in the July Consumer Price Index, excluding food and energy, the same as in June, which was the biggest increase since January 2017. But don't start fretting that inflation is about to take off. The economists at Bloomberg Intelligence figure that inflation appears to be approaching a midyear plateau based on varying degrees of deceleration in the three- and six-month rates of change in the core measure. If true, it may mean that the odds of a fourth-quarter interest rate increase by the Fed may shrink, underpinning bonds, stocks and other financial assets.

DON'T MISS

Elon Musk Isn’t Wrong About the Public Markets: Nir Kaissar

High-Yield Bond ETFs Try to Fill Liquidity Void: Brian Chappatta

Britain's No-Deal Brexit Woes Are Sinking Sterling: Mark Gilbert

Bank of Japan Is Committed to Low Rates, for Now: Daniel Moss

Challenge to Biggest Idea in Behavioral Finance: Barry Ritholtz

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.