Many Americans Still Feel the Sting of Lost Wealth

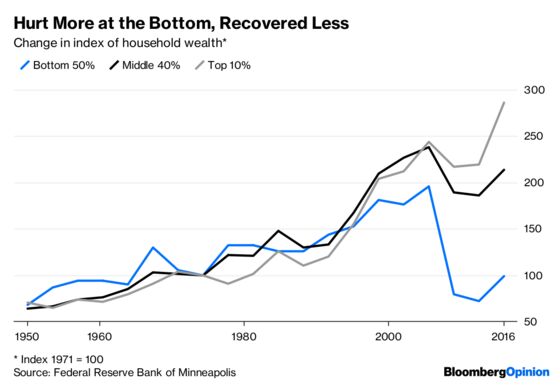

(Bloomberg Opinion) -- The financial crisis and the Great Recession were absolutely devastating for the wealth of middle- and lower-income Americans. A report from the Federal Reserve Bank of Minneapolis shows just how big of a hit they took:

The average household in the top 10 percent of today’s wealth distribution is almost three times as rich as the average household in the top 10 percent of 1971’s distribution. Meanwhile, the average household in the bottom half is slightly poorer.

This is a striking demonstration of rising inequality, but it also tells a story about the last few decades of American economic life. Beginning in the late 1990s, the upper half of the wealth distribution started to pull away from the lower half, but on the eve of the housing crash, all three categories had seen a steady gain in wealth since 1950. A person living in July 2006, looking back on the past half-century, could feel reasonably comfortable that most Americans were still living the dream of steadily rising wealth.

But the housing price decline that began in mid-2006, and the chain of disasters that followed, totally wiped out that trend. Eight years later, the picture looks like one of divergence rather than broadly shared gains.

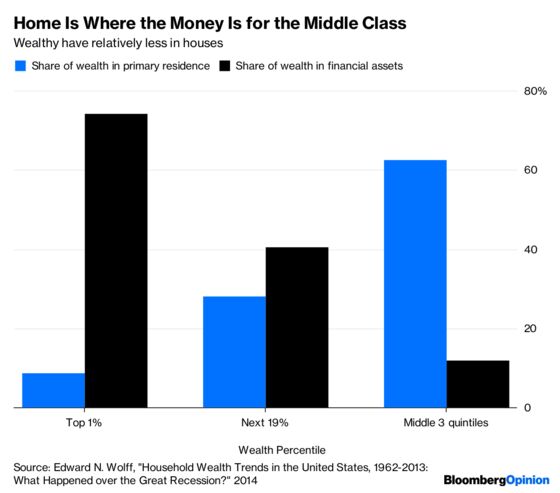

Why? One reason is that the middle- and lower-income Americans tend to hold much of their wealth in houses, while the upper class tends to own a lot of stocks. The Minneapolis Fed’s report is based on a recent paper by economists Moritz Kuhn, Moritz Schularick and Ulrike Steins, which measures historical U.S. wealth levels using the Survey of Consumer Finances. The authors carefully adjust their data for aging (older people tend to have accumulated more wealth) and shrinking household size, and find that the overall trends remain solidly in place.

Kuhn et al. find big differences between the various groups pictured above. Families in both the bottom 50 percent and the middle 40 percent tend to have most of their money in houses (usually their own). The main difference between the two groups is debt -- the bottom 50 percent relatively have a lot more of it, which cancels out their housing assets and leaves them with very little net worth. The top 10 percent, in contrast, have the bulk of their money in the stock market.

That breakdown agrees with what other economists have reported:

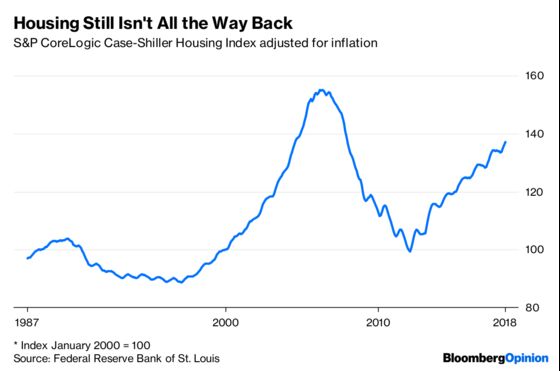

The housing crash, financial crisis and Great Recession was concentrated in the housing sector. In real terms, house prices fell about 50 percent from peak to trough, and still haven’t recovered:

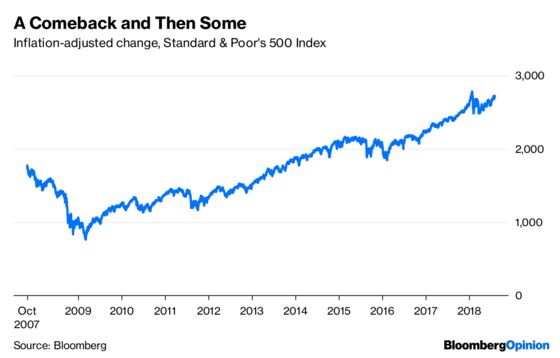

Meanwhile, the stock market fell by more, but rebounded much more quickly, and is now about 50 percent higher in inflation-adjusted terms from the pre-crisis peak:

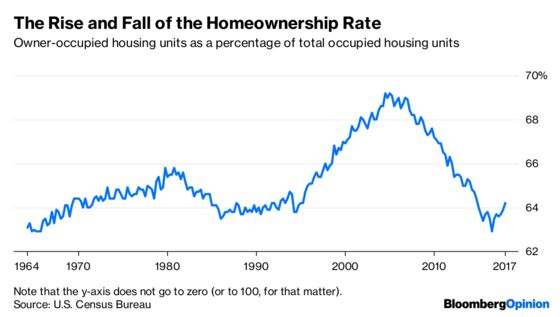

This is one big reason why the recovery has benefitted the wealth of those at the top so much more than those at the bottom. But it’s not the only reason. Savings differences also matter -- the rich tend to save more than the poor. Another factor is probably the falling homeownership rate:

During the housing bubble, more Americans owned their own homes; the trend reversed in 2006. That meant that even when house prices partially recovered, those who lost their houses in the crash weren’t able to share in the rebound. The government’s failure to bail out underwater homeowners -- recall that the Tea Party was inspired by an on-air rant against the idea of aiding struggling mortgage borrowers -- was a fateful error whose economic and social consequences are still being felt.

Wealth inequality eats at the core of a society. But as long as the wealth of the middle and lower classes is growing -- as it was up until 2006 -- the corrosive effect of inequality will be limited. For half of the country, the housing collapse destroyed a 60-year story of the American dream -- no wonder so many people are turning to populism and socialism.

To restore that dream, wealth will have to grow again for a broader swath of Americans. In a country with slow productivity growth and an aging population, that probably would require redistribution of wealth.

One option is a social-wealth fund. If the government uses tax revenue to buy shares in companies, and then distributes the dividends and capital gains to citizens, that will help solve the problem of stock ownership being concentrated at the top. This could be paired with policies to nudge workers into putting more into their retirement accounts, along with measures to reduce money management fees. Additionally, taxing capital gains and dividend taxes as ordinary income, and distributing the proceeds to lower-income households, could compress inequality.

A second strategy is to raise homeownership. As the 2000s housing bubble showed, this path to wealth can be fraught with peril. And pumping up house prices can easily shut later generations out of the market. But as an asset, housing also has its advantages -- it’s relatively easy for most people to understand, and mortgage payments nudge people to save more of their paychecks.

The best way to build housing wealth would be to create more real housing value. State governments could upzone low-density neighborhoods, and provide subsidies to help lower-income people purchase houses in those areas. Some local homeowners would resist greater density, but overall, denser, more productive cities should cause property values -- and wages -- to rise.

There are other options for restoring lost wealth, and these should be discussed. But if something isn’t done, large numbers of Americans are likely to look back on a half-century of wealth destruction and stagnation with an increasingly jaundiced eye.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Noah Smith is a Bloomberg Opinion columnist. He was an assistant professor of finance at Stony Brook University, and he blogs at Noahpinion.

©2018 Bloomberg L.P.