The Bond Market Is Developing a Cash Problem

The U.S. Treasury on Wednesday sold more 10-year notes than it ever had before to help finance a bulging budget deficit.

(Bloomberg Opinion) -- The U.S. Treasury Department on Wednesday sold more 10-year notes than it ever had before to help finance a bulging budget deficit. Strategists generally deemed the $26 billion auction “solid.” And although that’s certainly true when comparing the results with recent auctions, it’s hard to ignore an inconvenient truth facing the bond market.

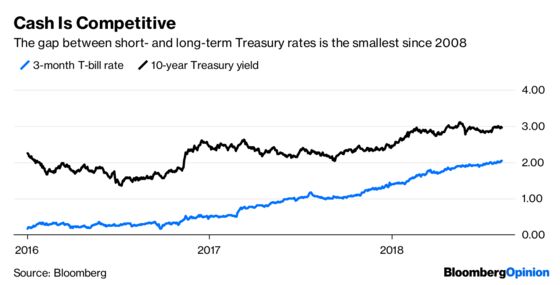

Investors submitted bids for 2.55 times the amount offered, which was in line with the average of 2.53 this year for 10-year notes. But average is a bit of a disappointment when considering that inflation expectations are dropping rapidly, which should make longer-term debt more appealing. Yields on Treasury Inflation Protected Securities show that breakeven rates on government debt (which is what traders expect the rate of inflation to be over the life of the securities) fell to 1.98 percent on Wednesday, the lowest since February. The rate reached 2.19 percent as recently as May. The reality is that Federal Reserve interest-rate increases are finally making cash a viable alternative. The question for bond investors is whether to lend money to the government for 10 years at a rate of about 3 percent and assume all the risks that come from that — $1 trillion budget deficits? Central banks switching from quantitative easing to quantitative tightening? — or buy three-month Treasury bills and get a rate that’s just a little less — currently 2.05 percent, up from less than 1 percent a year ago and 0.3 percent two years ago — and assume no risk.

“After years of (getting) zero, 2 percent feels like a lot,” Michael Shaoul, the chief executive officer of Marketfield Asset Management, said Wednesday on Bloomberg Television. At the start of last year, 10-year Treasuries paid about 2 percentage points more than three-month bills. In 2015, they paid almost 2.50 percentage points more than the cash equivalents.

CRUDE CRUMBLES

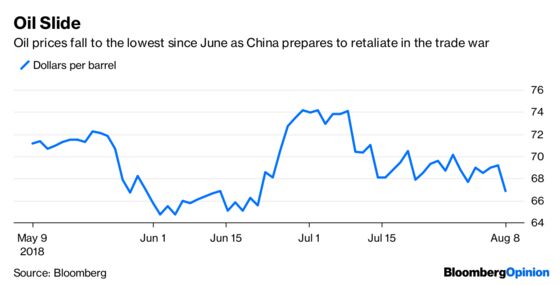

One big reason bond breakeven rates dropped on Wednesday is because crude oil prices, which are a big part of the Consumer Price Index, took a dive. Futures on West Texas Intermediate dropped as much as 4.12 percent on Wednesday in New York on reports that China will levy 25 percent tariffs on billions of dollars in U.S. gasoline, diesel and other goods in a matter of weeks, according to Bloomberg News’s Jessica Summers. Meanwhile, American crude inventories fell by just a fraction of what was forecast, the Energy Information Administration reported. The breakout in oil prices to the downside to $66.32 a barrel, the lowest since June, reverses a rally that pushed prices up to $75.27 in early July. The levies will take effect on Aug. 23, China’s commerce ministry said in a release. The list also includes lubricating oil, asphalt and aviation gasoline as China follows through on penalizing products initially listed as at-risk in June, reports Bloomberg News’s Ryan Collins. Oil from American fields was among goods the Chinese designated as subject to eventual tariffs on a June 15 list. But crude was spared from the 11-page list of products that will incur the latest tariffs. China was the biggest foreign buyer of U.S. crude as recently as June, purchasing a record 15 million barrels that month.

POUND FREEFALL

It’s getting (even more) ugly in the market for sterling. The Bloomberg Pound Index fell for a fifth consecutive day Wednesday, dropping as much as 0.62 percent to its lowest level since September. It’s now down 6.61 percent from its high this year in April. An increasing number of foreign-exchange traders are coming to the conclusion that the U.K. could end up leaving the European Union with no agreement for future economic ties, which would be a disaster for its economy. U.K. International Trade Secretary Liam Fox said over the weekend that the risk of a no-deal Brexit had increased to as much as 60 percent. “Markets are starting to focus on the pound-specific risks associated with a no-deal Brexit,” Viraj Patel, a currency strategist at ING Groep NV told Bloomberg News. The pound has weakened to 90.125 pence per euro from 87.234 in June, and Patel says he sees it depreciating to 91 or 92 pence in coming months. U.K. Prime Minister Theresa May is stepping up the government’s preparations in case Brexit negotiations break down and the country crashes out of the EU without a deal. May is planning a top-level meeting of her cabinet ministers early in September specifically to discuss how to ready the U.K. for a no-deal Brexit, reports Bloomberg News’s Tim Ross, citing people familiar with the matter.

RUBLE REDUCED TO RUBBLE

Maybe Donald Trump is right when he says no U.S. President has been tougher on Russia than him. At the least, he has currency traders worried. The ruble was the biggest loser in the global foreign-exchange market Wednesday, weakening 2.41 percent in late trading and heading for its lowest closing level since November 2016. The move came after Russia’s Kommersant newspaper published the full text of a U.S. bill seeking “crushing sanctions” for election meddling. The bill includes proposals to sanction new sovereign debt and block dollar transactions of the nation’s biggest lenders. Traders are particularly concerned by a clause that calls for prohibiting “all transactions in all property and interests in property” of some of the country’s largest lenders, according to Bloomberg News’s Natasha Doff and Artyom Danielyan. “The Kommersant publication was the straw that broke the camel’s back,” Denis Davydov, an analyst at Nordea Bank in Moscow, told Bloomberg News. But with Trump calling for closer ties with Russia, and the U.S. Treasury warning earlier this year against sanctioning the sovereign debt market, it’s uncertain the bill will make it into law. Traders aren’t taking any chances.

SWEDEN MAKES A MOVE

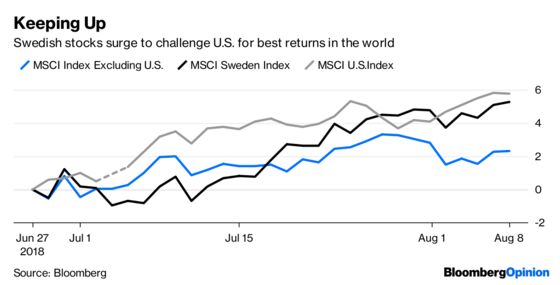

The story of the year in global equity markets has been the performance of U.S. stocks, which went from lagging behind in 2017 to setting the pace in 2018. The MSCI USA Index has gained 7.06 percent this year, with the bulk of the gains coming in the last three months, compared with a decline of 3.88 percent for the MSCI All Country World Index excluding the U.S. But Sweden is coming on strong, with the MSCI Sweden Index gaining 5.26 percent over the last six weeks, compared with 5.76 percent for the U.S. index. While much of Europe’s growth stagnates, a report last week showed Sweden’s economy expanded twice as fast in the second quarter as economists estimated. This was followed by data showing a jump in manufacturing activity. State Street Bank & Trust Co. is recommending international investors load up on the krona to take advantage of the brighter outlook in Sweden, according to Bloomberg News’s Anooja Debnath. The currency is now seen as one of the top three gainers in the G-10 basket against the greenback for the remainder of 2018, according to the median estimate of foreign-exchange strategists surveyed by Bloomberg. Although Swedish stocks aren’t cheap at 17.6 times trailing 12-month earnings, they are a relative bargain compared with the 21.2 price-to-earnings ratio for U.S. equities, data compiled by Bloomberg show.

TEA LEAVES

The escalation of trade tensions between the U.S and China have garnered most of the attention of market participants, but on Wednesday the focus will shift just a bit. That’s when the U.S. and Japan start two days of trade talks. Although Japan has largely sought to avoid confrontation with the Trump administration over trade, declining to retaliate over steel and aluminum tariffs, Japanese officials are signaling they are ready to take a harder line on the threat of U.S. tariffs on vehicles and car parts, according to Bloomberg News' Connor Cislo and Andrew Mayeda. It’s been difficult to bridge the divide between the two countries, given Japan’s commitment to a multilateral trade deal with Asia-Pacific countries, and the Trump administration’s preference for bilateral agreements, they reported, citing a person familiar with the situation who spoke on condition of anonymity because the discussions aren’t public.

DON’T MISS

S&P 500’s Run at Record Lacks Animal Spirits: Charles Lieberman

Tesla Going Private Would Destroy CDS Investors: Brian Chappatta

Many Americans Still Feel the Sting of Lost Wealth: Noah Smith

There’s a Hole at the Heart of China’s Silk Road: Mihir Sharma

Brexiteers Are Their Own Worst Enemy: Clive Crook

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.