End-of-Days Metals Rout Overstates Trade War Risks

(Bloomberg Opinion) -- Commodity investors are acting like it’s the last days of Rome.

News that the Trump administration was planning to increase the tariff rate on $200 billion of Chinese imports to 25 percent from 10 percent sent markets into a tailspin Wednesday, with a Bloomberg Intelligence index of mining companies falling 1.7 percent and every major industrial metal slumping in synchrony.

Rio Tinto Group investors were so alarmed at the backdrop that even the company’s promise in first-half results yesterday to hand $7.2 billion back to shareholders in dividends and buybacks couldn’t stop the stock sliding as much as 4.8 percent.

It’s time to settle down. While trade wars could indeed deal a blow to global economic growth and the materials demand that’s bound up with it, the effect on individual commodities is likely to be anything but uniform. Indeed, for the likes of Rio Tinto it could be outright bullish.

To understand why, consider Beijing’s efforts to boost credit. The People’s Bank of China has been encouraging banks to lend more by taking a softer stance on loan quotas so as to offset the effects of a cooling economy, people familiar with the matter told Bloomberg News Wednesday, adding to the ongoing retreat from a deleveraging program that’s caused the country’s economy to slow this year.

That shouldn’t be all that surprising. As we argued last year and earlier this year, opening up the spigots of industrial stimulus is the Chinese leadership’s go-to way of bailing the economy out of a soft patch. Right now, President Xi Jinping stands before a yawning gulf of slowing growth from economic rebalancing, buffeted by threats of trade war and speculation that his unprecedented control over the Chinese state is weakening. Faced with that, who could resist the easy attractions of a fresh bump of state-directed credit stimulus?

To date, most official statistics have suggested that rebalancing is underway. Production of cement — one reliable proxy for the construction growth that swallows up most stimulus dollars — has been running at its lowest rates in years:

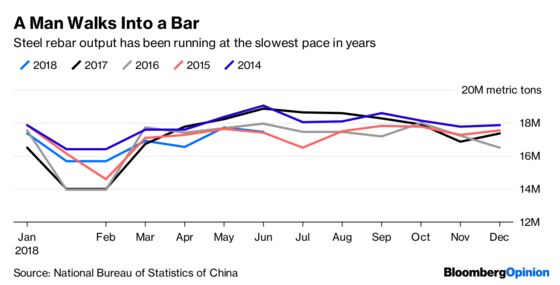

Steel rebar has been displaying the same pattern:

In theory, China’s credit loosening needn’t dramatically alter that picture. If the measures go to prop up cash-strapped small and medium enterprises, they could support less materials-intensive service sectors and keep the rebalancing show on the road. But just as water flows downhill, credit in China tends to drift not toward the little guy, but to precisely the connected state-owned firms that the deleveraging campaign is meant to starve of capital.

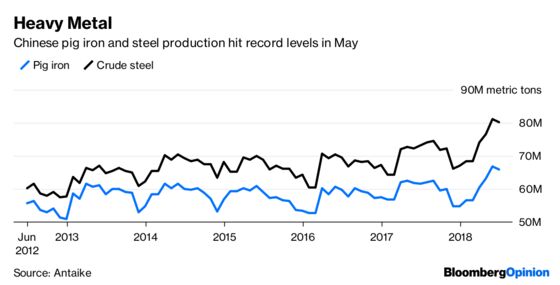

There’s already evidence that higher up the supply chain, industrial production is picking up. Output of crude steel and pig iron jumped to record levels in May and hardly edged back in June, according to data from Antaike, a consultancy — largely what you’d expect from a sector enjoying profits of around 1,000 yuan ($147) a metric ton. Steelmakers are so keen to boost output that they’re using scrap and high-iron ores to push their plants beyond conventional capacity limits, helping compensate for the closure of less-efficient factories in recent years, according to Goldman Sachs Group Inc. analyst Trina Chen.

The best way to consider what will happen to commodities over the remainder of 2018 is to think about end-use sectors.

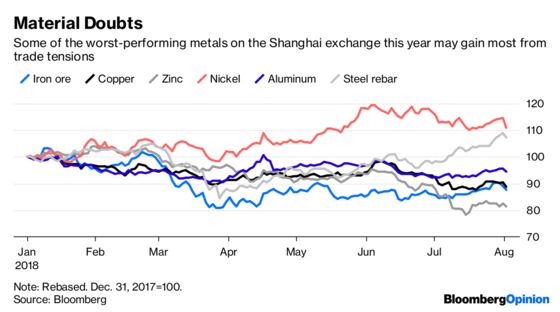

Smaller-volume base metals like zinc and nickel may indeed be facing tough times, as rising tariffs reduce demand for the manufactured goods in which they’re used. Materials like aluminum and copper may suffer less, since their use in consumer goods is balanced by a decent slice of demand from construction and engineering. Those like iron ore and steel which depend principally on heavy industry could be looking at bullish conditions, as Beijing increases spending to offset political and economic headwinds.

That’s bad news on a host of fronts. The global economy and climate badly need China to retreat from the materials-intensive path it’s pursued in recent decades. China’s current trajectory, paved with debt and increasingly unproductive industrial investments, inexorably reduces the odds that it can grow past the middle-income trap, and raises the risk of a financial crisis somewhere down the line.

The one group of people who shouldn’t be fretting, though, are producers of bulk commodities like Rio Tinto. China’s industrial addiction may be a problem for the world — but if you’re selling the stuff its economy is hooked on, you’re in the money.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.