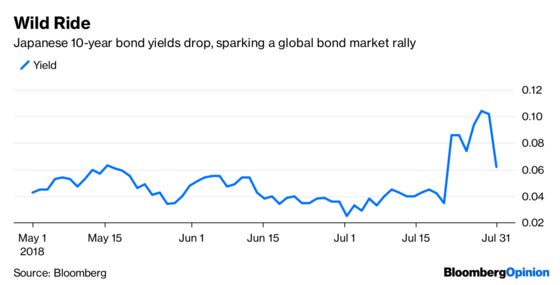

(Bloomberg Opinion) -- The two things bond traders fear most are hawkish central bankers and inflation, and neither seem to be much of a problem of late. Global bond markets rallied on Tuesday after the Bank of Japan said it expects to keep interest rates very low for an “extended period of time.” And in the U.S., the Federal Reserve’s preferred measure of inflation fell below its 2 percent target for June.

For all the talk at the start of the year of a nasty bear market in bonds pending on the horizon, conditions have largely been benign for fixed-income assets. The Bloomberg Barclays Global Aggregate Bond Index is down just 1.60 percent for the year through Monday and is basically unchanged since mid-May. In a statement Monday, the Bank of Japan lowered its inflation forecasts. And while data in the euro zone Tuesday showed faster inflation, economic growth slowed, easing concerns about future inflation pressures. In the U.S., the core personal consumption expenditure price index rose 1.9 percent in June from a year earlier. That kept so-called real yields, or what investors earn on 10-year Treasuries after inflation, at some of the highest levels since 2011, or about 1 percent. That may not sound like much, but real yields were negative as recently as 2016, according to data compiled by Bloomberg.

Betting on a reversal in the three-decade bull market in bonds has been a fool’s game for years. It will happen eventually, but time’s running out for 2018 to be the year that marks the high point in the bond market. As Van R. Hoisington and Lacy Hunt at Hoisington Investment Management, which runs the top-performing Wasatch-Hoisington U.S. Treasury Fund, wrote in their most recent quarterly review and outlook report, longer-term Treasury yields reflect “harsh realities which are constraining economic expansion,” including over-indebtedness, reliance on additional debt for growth, poor demographics, technological constraints and potential trade conflicts.

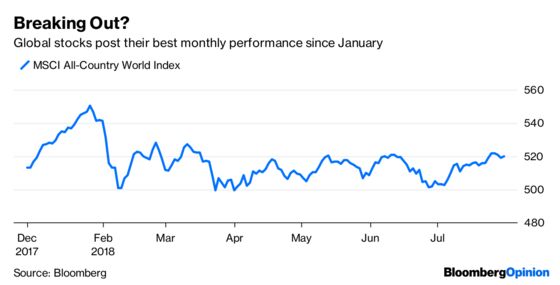

EQUITIES DELIVER JULY SURPRISE

The global equities market wrapped up July by posting its biggest monthly gain since January, with the MSCI All-Country World Index jumping 2.91 percent. The performance feels like a minor miracle, given the recent stumbles by such market-leading, highflying technology stocks as Facebook Inc., Netflix Inc. and Tencent Holdings Ltd. What’s encouraging is that all 11 major sectors that constitute the MSCI benchmark gauge gained in July, led by health care, industrial and finance. At about 15.7 times expected earnings, global equities seem like a relative bargain compared with the almost 17 times earnings they were trading at in January. It’s easy to say that equity investors are too complacent given the potential for a global trade war, but the amount of tariffs being thrown around are relatively small so far. Plus, there’s the sense that officials will come to some agreement before things get out of hand. U.S. stocks rallied Monday on reports that U.S. Treasury Secretary Steven Mnuchin and Chinese Vice Premier Liu He are having private conversations to restart talks aimed at averting a full-blown trade war between the world’s two largest economies. And last week, President Donald Trump and European Commission President Jean-Claude Juncker said they agreed to suspend new tariffs while continuing talks.

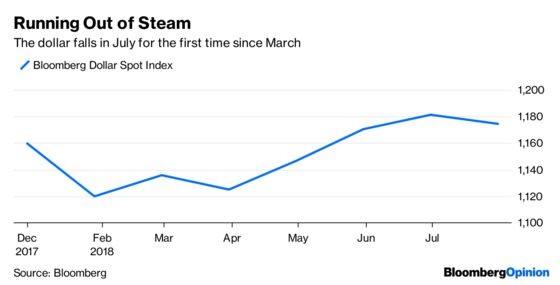

RIP DOLLAR RALLY

The Bloomberg Dollar Spot Index ended July on high note, rising for the first time in three days, but it wasn't enough to prevent the gauge from posting its first monthly decline since March. Despite a report last week showing the U.S. economy grew in the second quarter at its fastest pace since 2014, currency traders have little appetite to keep pushing the greenback higher as the government’s borrowing needs increase to finance a rapidly expanding federal budget deficit. Morgan Stanley, State Street Corp. and Wells Fargo & Co. are some of the firms that have said recently that the dollar has peaked after gaining about 5 percent against its chief peers since mid-April, according to Bloomberg News’s Lananh Nguyen. It doesn’t help bullish sentiment that President Donald Trump has signaled that he’d prefer a weaker dollar. “With U.S. growth set to slow going forward, and with the Fed rate hike pace also likely to slow from its current ‘automatic’ pace, key fundamental drivers of this year’s greenback strength are likely to fade,” Wells Fargo strategists wrote in a July 27 research note. Some of the biggest gainers against the dollar in July were the Mexican peso, Argentine peso, South African rand, Brazilian real and Hungarian forint, all of which gained about 3 percent to 7 percent.

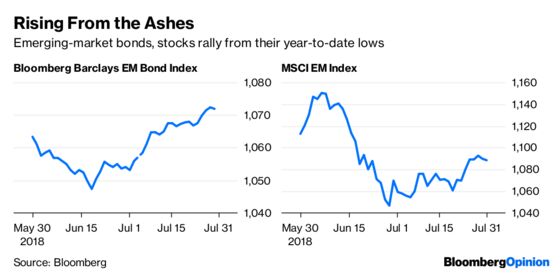

LAWS OF SUPPLY AND DEMAND WORK IN EM

The best performing part of the global bond market in July was emerging-market debt securities. The Bloomberg Barclays Emerging Markets Hard Currency Aggregate Index jumped 1.69 percent through Monday. It helped that the dollar’s rally petered out, but perhaps just as important is that emerging-market debt got a bit scarce in July. Borrowers raised $118 billion this month from 981 issues, the least since July 2013, according to data compiled by Bloomberg. The decline in supply came after yields for emerging-market debt climbed for six consecutive months, the longest streak since at least 1998, as an advancing dollar and rising U.S. interest rates diminished investor demand for risky assets, according to Bloomberg News Dana El Baltaji. The average yield on dollar-denominated debt in emerging markets fell 17 basis points in July to 5.59 percent on Monday, the Bloomberg Barclays index shows. Other parts of emerging markets also rebounded in July, with the MSCI EM Index of equities surging 1.73 percent in its first gain since January, and a similar gauge of EM currencies snapping three monthly declines to end July little changed. “We do like EM assets, particularly EM equities,” Isabelle Mateos y Lago, chief multi-asset strategist at BlackRock Investment Institute, the asset manager’s think tank, recently told Bloomberg News. “It’s a combination of the global growth backdrop, earnings expectations for emerging-market corporations and valuations.”

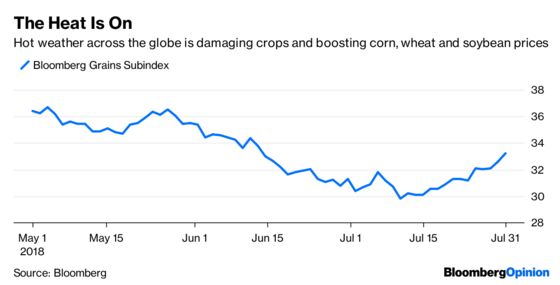

MOTHER NATURE TRUMPS TARIFFS

Perhaps no market is tougher to predict than commodities. Prices are often subject to unforeseen events, like the weather. So while everyone has been wringing their hands about a budding trade war between the U.S. and China, scorching dry weather has taken over as the main driver of grain prices. The Bloomberg Grains Index, made up of contracts tied to corn, soybeans and wheat, has surged 5.65 percent this month, its biggest gain since August. Of course, grains still have a long way to go before wiping out their 11.9 percent decline in June, but the trend is the right one for farmers who haven’t seen crops hurt by the weather. To be sure, the recent heat is not just a U.S. phenomenon but is also impacting crops in Europe and Asia, raising worries about future supply, according to Bloomberg News’s Lucca de Paoli. Elevated temperatures in the Northern Hemisphere can be traced to a so-called kink in the jet stream, which is a ribbon of wind that circles the Earth. The heat has been blamed for wildfires across Scandinavia, Greece and California, record high temperatures in Texas, Japan and Africa and flooding rains along the U.S. East Coast last week. The world is hotter in general, which means when temperatures spike, they do so off a higher baseline, according to Bloomberg News’s Brian K. Sullivan and Eric Roston.

TEA LEAVES

No one seems quite sure whether that looming trade war is affecting U.S. businesses or not. Yes, the Commerce Department said Friday that gross domestic product expanded at a 4.1 percent rate in the second quarter, the fastest pace since 2014, but various surveys show that businesses are much less confident about the outlook. Investors and economist should get some clarity Wednesday, when the Institute for Supply Management releases its monthly manufacturing survey for July. In the June report, Bloomberg Intelligence notes that the forward-looking new orders component remained above 60, and supplier deliveries — the time it takes to deliver a product — surged. But some of the increase may have been due to manufacturers stockpiling inventories in anticipation of additional rounds of tariffs. So the report may not provide a full answer to the question of whether tariffs are hurting U.S. businesses, but it could provide a critical piece of the puzzle.

DON'T MISS

Housing Headwinds Are Getting Stiffer: Danielle DiMartino Booth

Junk Bonds Are Treasures When There's No Supply: Brian Chappatta

French Bonds Should Wake Up and Smell the Sake: Marcus Ashworth

The Bank of Japan Has Found Some Cover for Tapering: Shuli Ren

Hedge Funds’ Big Short Could Be Fool’s Gold: David Fickling

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.