(Bloomberg Opinion) -- Why was economic growth so anemic in the early years of the current expansion? Why did it pick up in 2015? Why is it picking up again now?

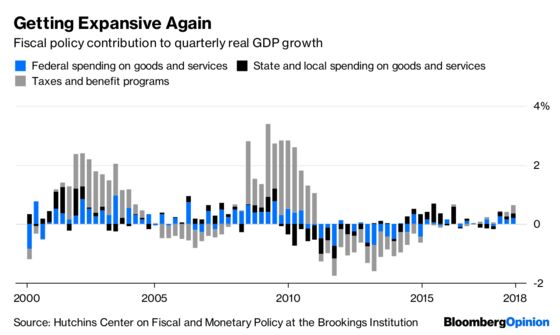

Well, there are surely lots of reasons. But if you are even modestly predisposed to believe that government fiscal policy is a major driver of short-to-medium-term moves in gross domestic product, this chart will certainly not disabuse you:

This “Hutchins Center Fiscal Impact Measure,” calculated by researchers at the Hutchins Center on Fiscal and Monetary Policy at the Brookings Institution using data from the Commerce Department’s Bureau of Economic Analysis, “includes both the direct effect of federal and state/local spending on GDP ... as well as an estimate of the indirect effects of fiscal policy on GDP growth through its effect on private consumption.” This last is what’s labeled in the above chart as “taxes and benefit programs.” The quotes are from a detailed Hutchins Center explainer. There’s also a 2009 paper by three Federal Reserve Board economists outlining the general approach. It seems legit, in other words.

The fiscal impact measure shows that falling taxes and rising benefit payouts accounted for the bulk of fiscal stimulus during and immediately after the Great Recession. Most of this was the automatic consequence of a steep economic decline, which cut into tax receipts and increased demand for unemployment insurance, food stamps and the like. As the economy began to grow again, this automatic stimulus reversed. The non-automatic stimulus from Congress also reversed and stayed mostly negative for several years as a new Republican majority in the House of Representatives pushed hard for spending cuts.

State and local governments retrenched too as they tried to clean up the fiscal mess left by the recession, although their policies stopped cutting into GDP growth much after 2012 and started boosting it significantly in late 2014. Starting in the fourth quarter of last year, the federal government began delivering what is now its most sustained fiscal boost since 2010, with both spending increases and tax cuts playing a stimulative role. It hasn’t been all that big a stimulus just yet, but it appears set to continue for several years, with the Congressional Budget Office projecting that the federal deficit will grow to from 3.5 percent of GDP in the fiscal year that ended last September to 3.9 percent this fiscal year, 4.6 percent next year and 5.4 percent in fiscal 2022.

Are these rising deficits really a good thing for the economy? Economist Simon Kuznets, the originator of what is now called GDP, actually counted government spending as a cost to the private sector. It was John Maynard Keynes who pushed to include it instead as a contribution to economic growth. As David Pilling puts it in his book “The Growth Delusion”:

Without this definitional shift, what we know today as Keynesian fiscal stimulus would be difficult to justify since it would detract rather than add to national income.

As it is, though, fiscal stimulus does boost GDP. And after seven years of little to no stimulus from Washington, we’re getting some now from those Republican Keynesians in Congress and the White House.

To contact the editor responsible for this story: Brooke Sample at bsample1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2018 Bloomberg L.P.