(Bloomberg Opinion) -- Japan has, more or less, constantly been in the midst of the most radical monetary policy experiment in modern history since 2012. Is it working? It probably depends who you ask.

A brief recap: Abenomics (a program named after Prime Minister Shinzo Abe that combined ultra-loose monetary policy, flexible fiscal policy and selective deregulation to boost the economy) sparked an extreme form of quantitative easing that saw the Bank of Japan print yen to buy almost all of the $9.5 trillion in Japanese government bonds outstanding, as well as a huge portion of the equity market via exchange-traded funds.

The good news for Japan is that the yen is weaker, which has helped exporters. And while it’s hard to separate causation from correlation, deflation is no longer a persistent threat and the Japanese economy is arguably getting somewhat hot with the unemployment rate dropping to its lowest since the first half of the 1990s. These developments have not really gained widespread attention. In the public consciousness, most still think that Japan exists in a purgatory of deflation and bad demographics, but gross domestic product is starting to rise again, most notably on a nominal basis.

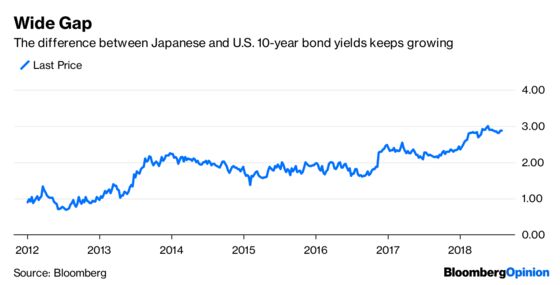

Investors should pay attention, because these changes come with special risks and challenges. In short, a hot Japan has the potential to blow up the world of macro investing. When an economy begins to accelerate, the typical response would be for longer-term bond yields to rise. But in Japan, they’re not permitted to do so. That’s because the BOJ’s QE program has morphed into something called yield curve control, where it buys as many bonds as needed to keep yields on 10-year notes from exceeding 0.1 percent.

This means that as bond yields rise globally, a pseudo-arbitrage exists between Japan’s bond market and the rest of the world. In other words, if an investor can successfully borrow and short Japanese government bonds, or JGBs, with yields around 0 percent currently and buy 10-year U.S. Treasury notes at 3 percent, somewhat riskless profits are possible.

But therein lies the problem. In free markets, prices — especially interest rates — are signals that help determine the correct allocation of capital. The bond market in Japan, home to the world’s third-largest economy, no longer performs that function because the BOJ has purchased so many bonds that there are many days when nothing is traded. So that trade probably couldn’t be put in place because an investor couldn’t find any bonds to short.

What would happen in a normal world is that speculators would aggressively short JGBs, driving up yields, strengthening the currency and holding off inflation. With yields pegged at zero, short selling JGBs simply results in more government bonds being bought by the BOJ — and the creation of a lot more yen, which will undoubtedly weaken.

That’s the theory, anyway, but it’s almost impossible to predict what can happen in some kind of economic zero-gravity environment, where the typical rules of supply and demand no longer exist. Although nobody really knows how this is going to play out, I can say with confidence that if the economy continues to strengthen and inflation rates rise further, the prospect of a hawkish BOJ is going to result in one of the biggest macro-investment challenges in memory.

If Japan spooks the bond market and yields skyrocket, the country faces a potential insolvency and possibly even default. At 224 percent of GDP, Japan's economy is more leveraged than Greece, where the debt-to-GDP is 180 percent, according to data compiled by Bloomberg. In the U.S., it’s 77.4 percent. Some people think Japan doesn’t even have to exit QE, and all officials have to do is cancel out the debt and start over (which seems very inflationary).

Japan has a large economy, and is underrepresented in the financial news relative to the size of that economy and the risks that it poses to the world. Foreign investors have lost a lot of money over the years attempting to short Japan’s markets, but for the first time in a long time it seems as though the trade might be closer to working. Nobody is prepared for a Japan that is a little more exciting.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Jared Dillian is the editor and publisher of The Daily Dirtnap, investment strategist at Mauldin Economics, and the author of "Street Freak" and "All the Evil of This World." He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.