What the GDP Report Won’t Tell You About the Economy

(Bloomberg Opinion) -- Something is amiss in Corporate America. Both national and regional surveys reveal a sinking sense that the economy’s tailwinds are shifting to headwinds. The downtrodden confidence is a curiosity given many economists’ forecasts calling for second-quarter growth to have accelerated to a 4.2 percent annualized rate, the fastest since 2014.

Soft though the survey data may be, the numbers don’t lie. If something doesn’t give — and fast — what follows is sure to be damaging to the real economy.

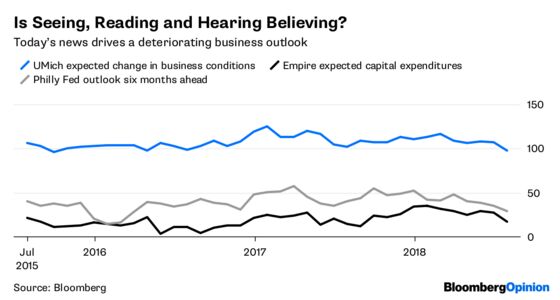

The University of Michigan consumer sentiment survey for July revealed that the business outlook had slumped to the lowest level in over two years. Odds are pretty good this number was dragged down by those with the highest incomes, many of whom are likely also business owners and corporate executives who’ve been on the front line of the rising costs to run their businesses.

But there may be more than meets the eye among those whose incomes rank in the top third of households. While the majority of these respondents expressed concern over the tariffs, what they’re reading, hearing and seeing may be dampening their outlooks even further. As things stand, it’s as if January never happened, a month in which confidence was so high, the “news heard” among high income earners hit a 20-year high. By the beginning of July, “news heard” had slid to minus 18, the lowest in two years. The six-month, 79-point swing is so severe it rivals August 2011, when the euro crisis shook world markets, Standard & Poor’s stripped the U.S. of its AAA credit rating, and households were rattled by the debt ceiling debacle.

Are things really all that bad? Alcoa Corp. Chief Executive Roy Harvey certainly seems to think so. In the aluminum giant’s post-earnings conference call last week, Harvey explained that rather than benefit, the company is suffering from U.S.-imposed tariffs despite the original intent of the effective tax imposition on imports. The required “primary aluminum,” a key input for further processing into products Alcoa makes, comes from its own Canadian smelters, where tariffs have been levied. The firm’s raw materials costs have thus increased, crimping profits and leaving executives with the poor choice of paying tariffs on its own imports or selling its Canadian production outside the U.S. at lower margins. In addition, much of the increased domestic demand for aluminum has been satisfied by antiquated and inefficient production capacity that had been taken offline, further depressing profits.

Alcoa is among the minority of companies that have said tariffs are responsible for tempering their earnings outlooks. (Some of the concerns over trade eased after President Donald Trump and European Commission President Jean-Claude Juncker said Wednesday that they agreed to suspend new tariffs while continuing talks.) Most blame the strengthening dollar. Nevertheless, the law of unintended consequences is apparent in the first two regional Federal Reserve surveys released for July.

The first out was the New York Fed’s Empire report, which covers the New York area. Planned capital expenditure and technology spending sank in July, falling to the lowest in 11 months. A similar survey from the Philadelphia Fed echoed those results, with the outlook for employment falling to the lowest in 17 months, and the outlook for “business activity” dropping to the lowest since March 2016. The portion of the survey covering new orders and backlogs tumbled to the lowest since February of that same year.

Bleakley Financial Group Chief Investment Officer Peter Boockvar posed some difficult questions in the wake of the survey’s conclusion that while current activity remains brisk, the future is less promising: “Is it the tariffs? A stronger dollar? Did we pull a lot of activity into the second quarter because of supply constraints where everyone was double ordering?”

Anecdotal evidence certainly suggests as much, with firms reporting that they’ve been stockpiling for months to head off possible price increases brought on by future tariffs. In last week’s two-day testimony to Congress, Fed Chairman Jerome Powell expressed concern that the tariffs would compel companies to ratchet back activity. As if on cue, the day after his testimony, the Fed’s Beige Book of economic activity had this to say: “Manufacturers in all Districts expressed concern about tariffs and in many Districts reported higher prices and supply disruptions that they attributed to the new trade policies.”

The Cleveland and New York District Feds, in particular, reported activity had already taken a hit. As is the case with Alcoa, the New York area engages in a good amount of trade with Canada, and manufacturers corroborated that costs had increased. Meanwhile, panic buying is reported to have pulled activity forward in the Cleveland region: “In some cases, manufacturers noted a rush to purchase metals in anticipation of additional price increases.”

Consider the starting point for many companies. Last year’s weak dollar and natural disasters had many struggling to satisfy overseas demands and the massive needs required to rebuild. Labor and raw material costs were already on the rise to correct for the imbalances. The tariffs were the insult to injury many manufacturers could simply not afford.

“The actual economic impact will really come down to time,” cautioned Boockvar. “The longer this goes on, the more actual business activity will be negatively affected.” To Boockvar’s point, the collapse in business sentiment suggests many companies don’t foresee the ability to withstand further blows to their ability to profitably conduct business. Businesses are saying as much.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Quill Intelligence.

©2018 Bloomberg L.P.