(Bloomberg Opinion) -- The bond market these days is about as fun as watching paint dry. The benchmark 10-year Treasury note yield has moved less than 7.7 basis points in July, putting it on course for its smallest monthly range since 1973, according to Bloomberg News. Even so, some very important developments are happening beneath the surface that shouldn’t be ignored.

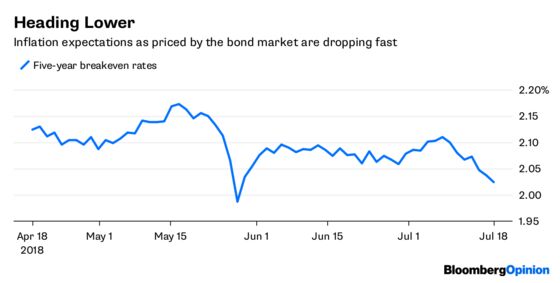

Federal Reserve Chairman Jerome Powell raised a few eyebrows on Wednesday when he told the House Financial Services Committee on his second day of semiannual testimony before Congress that policy makers are “slightly more worried about lower inflation.” That was a bit of a shocker given the Fed has already raised interest rates twice this year and has flagged at least one more before January. Perhaps Powell was just following the bond market’s lead. Despite overall yields being little changed, breakeven rates on Treasuries (which is what traders expect the rate of inflation to be over the life of the securities) have tumbled. For five-year securities, the rate has come all the way down to 2.02 percent on Wednesday from 2.17 percent in May. Much of that is likely due to weakness in the commodities market, especially the recent declines in oil and gasoline, but recent economic data have thrown doubt on the purchasing power of consumers. Specifically, the government said last week that real wages — or what consumers actually earn after taking inflation into account — failed to advance in June.

Signs that inflation expectations are anchored — or even declining — could give the Fed cover to slow the pace of rate increases to gauge the U.S. economy’s response to the escalating global trade war. And if Powell truly is concerned about slower inflation, it could help explain why he added the qualifier “for now” when he reiterated to the Senate the Fed’s commitment to the current policy of gradual rate increases.

THE STOCK BUYBACK MYTH

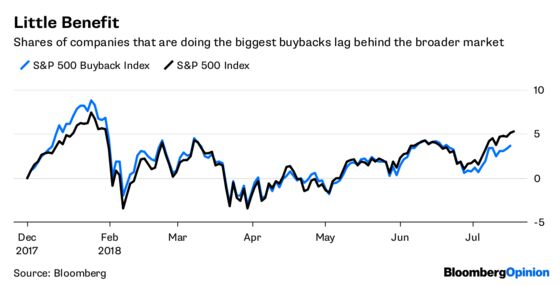

The S&P 500 Index rallied on Wednesday, helped by the biggest gain in four months in the shares of Warren Buffett’s Berkshire Hathaway Inc. after the company said it was removing a cap on stock repurchases. One theory for why stocks haven’t fallen out of bed this year despite the political turmoil in Washington is that companies are using money repatriated from overseas thanks to tax reform to buy back their shares. But buybacks are neither at an abnormally high level nor are they leading to outperformance of the shares of companies doing them. Although U.S. buybacks look set to approach a record $1 trillion this year based on what has been announced, in volume terms it’s not as impressive, according to JPMorgan Chase & Co. The firm’s strategists note that at 4 percent of the capitalization of the S&P 500, this year’s announced buyback pace is lower than the record of 6 percent in 2007 and below the 5 percent post-Lehman peak seen in 2012. “If one looks at net actual buybacks rather than gross announced buybacks, the YTD pace of the share count reduction across major U.S. equity indices is almost half of its 2015 high,” the strategists noted. Oh, and at 3.62 percent, the gain this year in the S&P 500 Buyback Index of the top 100 stocks with the highest repurchase ratios trails the 5.31 percent increase of the broader S&P 500.

A YEN MYSTERY

Many market participants are scratching their heads this year over the performance on the yen. A traditional haven in times of crises, the yen has been anything but this year despite rising global trade tensions. The yen has been little changed over the last three months against a basket off developed-market currencies even though the Swiss franc and U.S. dollar — two other haven currencies — have strengthened. One explanation could be an increase in Japan’s appetite for risk assets overseas. The Japanese have been net buyers of foreign stocks every week since the end of March, and purchases reached a record 985 billion yen ($8.7 billion) in the five days ended June 29, Bloomberg News reports, citing data from the Ministry of Finance. The yen is the second-worst performing Group of 10 currency since the beginning of April, just behind the U.K.’s pound. The yen is yet another reminder that the foreign-exchange market often zigs when many expect it to zag. The Citi Parker Global Currency Index, which tracks nine distinct foreign-exchange investment styles, is down 1 percent in 2018 after falling in each of the past three years and six of the last seven.

CRYPTOCURRENCY SMACKDOWN

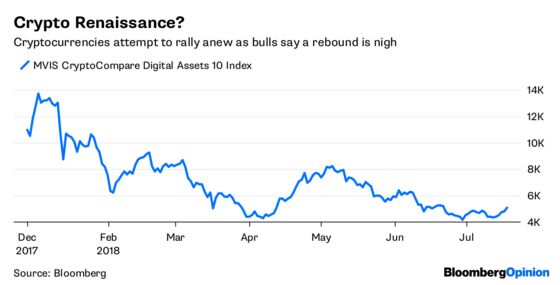

Fans of Bitcoin and other digital currencies, who have been pummeled this year, are getting excited by a budding rebound in the market. Led by Bitcoin, the MVIS CryptoCompare Digital Assets 10 Index, which tracks the performance of the 10 largest and most liquid digital assets, has risen for five consecutive days, gaining 23 percent. Even so, the index is still down 53 percent for the year and a number of prominent investors came out on Wednesday to throw cold water on the mini-rebound. Billionaire hedge fund manager Ken Griffin said at the CNBC Institutional Investor Delivering Alpha Conference that he questions the value of cryptocurrencies and laments how younger investors have been attracted to the digital coins rather than stocks of companies that drive economic growth. While Griffin’s securities trading business has considered making markets in crypto-assets, the Citadel founder said he has “a hard time” being a liquidity provider in a product he doesn’t believe in, according to Bloomberg News. Likewise, Oaktree Capital Group LLC co-chairman and co-founder Howard Marks said that in the long run, Bitcoin will be shown to have no substance. Last week, Fundstrat Global Advisors head of research Thomas Lee, one of Wall Street’s most outspoken Bitcoin bulls, said he was sticking with his year-end forecast of $25,000. Since he reiterated that call, Bitcoin has added almost $1,000, but at $7,370 it still has a long way to go to meet Lee’s forecast.

RELIEF IN SIGHT?

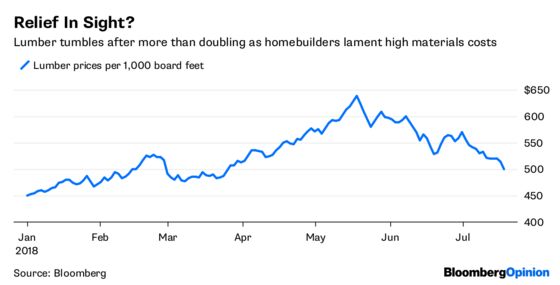

Shares of companies involved in the housing industry have suffered this year, with the Bloomberg Americas Homebuilders Index dropping about 155 percent, compared with a gain of 5.20 percent for the S&P 500. Government figures released Wednesday showed that U.S. housing starts fell in June to the slowest paces in nine months amid higher mortgage rates and elevated costs for labor and materials. But it looks as if some relief is on the way in the form of lower lumber prices. They soared about 95 percent between January 2017 and mid-May to a record amid U.S. tariffs on Canadian imports, transport bottlenecks and strong housing demand. But they have since dropped about 20 percent to $499.90 per 1,000 board feet on the Chicago Mercantile Exchange. “The market is searching for a bottom,” Kevin Mason, managing director of Vancouver-based ERA Forest Products Research, said in an email to Bloomberg News. “The poor housing numbers are the key driver.”

TEA LEAVES

Concern is starting to rise that escalating trade tensions between the U.S. and its main trading partners may be causing companies to become more cautious in their outlooks despite government reports showing continued strength in hiring. First, the University of Michigan’s monthly consumer confidence survey on Friday showed that the portion of its poll asking respondents about their outlook for business conditions in a year tumbled to its lowest since April 2016. Then, earlier this week the New York Federal Reserve’s monthly Empire Manufacturing index showed that the plans by companies in the New York area to increase capital expenditures in the next six months fell to its lowest since August. That’s why Thursday's regional economic index for July from the Philadelphia Federal Reserve will take on added importance. The June report was soft, with the index dropping to its lowest since November 2016.

DON'T MISS

Powell Wants to Create Some Mystery Around Fed Meetings: Tim Duy

Trade War May Spark a Chinese Debt Crisis: Anne Stevenson-Yang

Puerto Rico Battles the Shortsighted Hedge Funds: Joe Nocera

If Any Oil Gets Stranded, It Will Be OPEC's: Liam Denning

Target-Date Funds Aren’t the Retirement Bull’s-Eye: Nir Kaissar

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.