Markets Hear What They Want to Hear From Powell

It’s almost impossible to game out a trade war since it’s largely dependent on actions of unpredictable politicians

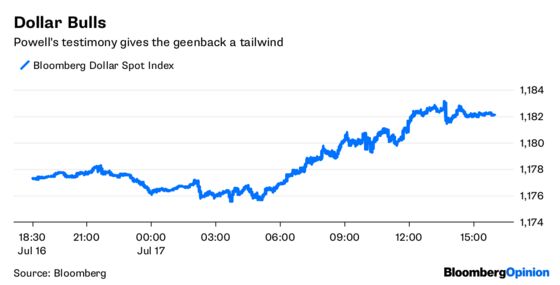

(Bloomberg Opinion) -- All you really need to know about the current state of markets was on display Tuesday. U.S. stocks rallied as Federal Reserve Chairman Jerome Powell suggested that the central bank is willing to slow the pace of interest-rate increases if needed. The dollar rallied as currency traders focused on Powell's comment that the Fed will continue to gradually raise rates. So, which is it? Don't look to the bond market for the deciding vote: Treasuries were basically flat on the day.

Investors are being buffeted by any number of crosscurrents that are making it harder than usual to make informed decisions. Yes, U.S. economic growth is accelerating and corporate profits are booming, but inflationary pressures, geopolitical risks and — most importantly — escalating trade tensions threaten the outlook. Bank of America Merrill Lynch’s July global fund manager survey released on Tuesday showed that a majority of investors worldwide believe a trade war is the greatest risk facing markets. The trouble for investors is that it's almost impossible to game out a trade war because it's largely dependent on the actions of unpredictable politicians. Viewed through that lens, it's no wonder markets are acting a bit schizophrenic these days.

The Federal Open Market Committee, the Fed panel that sets interest rates, “believes that — for now — the best way forward is to keep gradually raising the federal funds rate,” Powell said in prepared testimony before the Senate Banking Committee. As such, equities investors were heartened by the words “for now,’’ which suggested the Fed might pull back at the first sign of economic turbulence. Currency traders pushed the Bloomberg Dollar Spot Index up as much as 0.5 percent because the prospect of higher rates should continue to draw foreign investors into dollar-denominated assets.

THE DOLLAR IS BIG CONCERN FOR STOCKS

If Tuesday's surge in the dollar represents a new leg higher in the greenback after a short pause, perhaps investors in equities shouldn't be so upbeat. It's still early yet, but tariffs only rank as the eighth most important issue cited in conference calls so far this earnings season, according to Bianco Research, which cited data compiled by FactSet. More concerning is a stronger dollar, which makes U.S. good more expansive to foreign buyers. "Despite the constant hyperventilation on cable news channels regarding tariffs, companies are pointing to the dollar as the main headwind to earnings," Bianco Research President Jim Bianco wrote in a research note Tuesday. The Bloomberg Dollar Spot Index has surged 5.74 percent since mid-April, which helps explain why the S&P 500 Focused Foreign Revenue Exposure Index, which consists of the 125 members of the benchmark index with the largest weighting of foreign revenue, has gained just 3.85 percent since late March, while the S&P Focused U.S. Revenue Exposure Index has gained 9.69 percent. After foreign exchange, the next four factors cited by the highest number of companies as a negative impact are related to costs: raw materials, transport, labor and oil/gas.

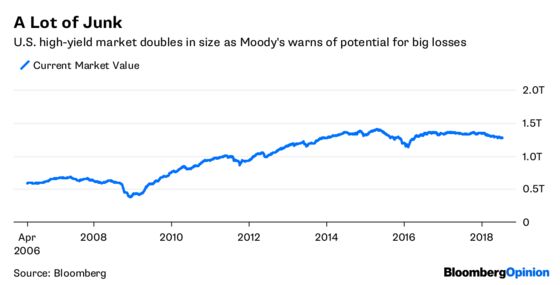

MOODY'S DELIVERS BOND WARNING

The market for U.S. high-yield, high-risk, or junk, bonds is one of the few areas of the global fixed-income market that has delivered a positive return to investors this year. Although it's not much, the 0.69 percent gain in the Bloomberg Barclays U.S. Corporate High Yield Bond Index is still better than the 1.39 percent drop in the Bloomberg Barclays Global Aggregate Bond Index. But a new report from Moody's Investors Service suggests there are troubled times ahead for credit investors. The ratings firm said in a report dated July 16 that "during a severe credit downturn, around one quarter of currently rated corporate issuers in the U.S. could default within three years" and "weaker covenants" could imply higher losses — lower recovery values — in a default. Maybe that wouldn't have been so alarming in the past, but since the financial crisis the corporate bond market has become a lot less creditworthy. Moody's latest corporate rating distributions indicate that the proportion of high-yield issuers is about 66 percent, up from 60 percent in 2008. The amount of junk bonds outstanding is even more striking. The Bloomberg Barclays U.S. Corporate High Yield index covers debt with a market value of $1.27 trillion, up from about $600 billion before the financial crisis.

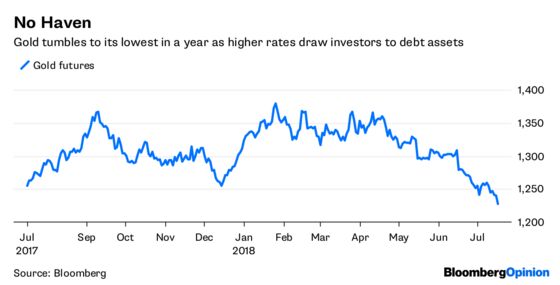

BULLION BUST

The gold market is setting up for an epic decline. The price of the precious metal dropped on Tuesday to its lowest since last July, bringing its drop since early April to 10 percent. What has strategists worried is that gold broke below $1,240 an ounce, which was seen as an area of support, to as low as $1,225.90 on Tuesday, according to data compiled Bloomberg. Holdings in exchange-traded funds backed by the metal have fallen for eight straight weeks, the longest slump since January 2014, according to Bloomberg News' Susan Barton. Also, futures traders have the least bullish net long position in more than two years, according Commodity Futures Trading Commission data. Some strategists blame a stronger dollar and higher short-term bond rates for gold's weakness. Since gold is traded in dollars, a stronger greenback makes it more costly to buy the precious metal. Perhaps, but the dollar has been stuck in a range the last month after rising in April and May. A better explanation may be that cash instruments are finally paying a competitive interest rate, while gold pays nothing. Treasury three-month bill rates topped 2 percent on Wednesday for the first time since 2008. The rate has quadrupled over the past 18 months.

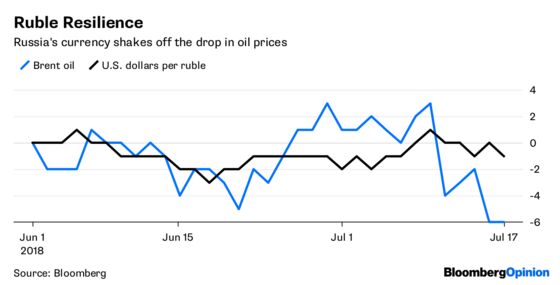

RUBLE RESILIENCE

President Donald Trump took Germany to task last week when he said a planned 1,230 kilometer (764-mile) undersea pipeline that will carry natural gas from fields in Russia to the European Union network at Germany’s Baltic coast makes Germany a captive to Russia. Since oil and gas exports are so integral to Russia's economy, it would be logical to expect the ruble to take a hit on the comments, especially with oil prices globally taking a dive. Except, it hasn't. Russia's currency has held up even though crude prices have dropped about 10 percent this month. That's because Russia is luring foreign investors away from Turkey, Brazil and Poland with a reassuringly hawkish central bank and some of the highest real yields in emerging markets, according to Bloomberg News's Ksenia Galouchko. Dividend and tax payments are also buoying the currency. “The correlation between oil and the ruble is nothing like it used to be, you can forget about it,” said Yury Tulinov, an analyst at Societe Generale SA’s local unit Rosbank. Although the 30-day correlation between the ruble and oil is up to 0.4 from being negative in May, it remains weak when compared with the almost perfect correlation of 0.9 seen in 2016. A correlation of 1 means markets move in lockstep; a reading of minus 1 the opposite.

TEA LEAVES

The Fed on Wednesday will release its Beige Book economic report, which is based on anecdotal information collected by its 12 regional banks. Bloomberg Intelligence notes that market participants will have to wait until the September iteration of the Beige Book for an assessment of the latest round of trade tensions as contacts submitted their responses before the July 10 announcement by the U.S. government will move forward with tariffs. That doesn't mean the report won't still have a lot of interesting and potentially market-moving material. The last Beige Book report, published in late May, noted that labor-market conditions remained tight across the country and that labor shortages of qualified workers persisted — particularly for truck drivers and IT professionals. The report cited a North Carolina trucking company that said some customers were willing to pay rates that quadrupled. In the Chicago district, “numerous contacts” said freight costs had “increased dramatically.”

DON'T MISS

Quants Are Getting a Bad Rap for Poor Performance: Aaron Brown

Jerome Powell Hints at Some Trouble With Curve: Brian Chappatta

Trump's Disdain for Europe Risks U.S. Economy: Michael R. Strain

These Investors Aren’t Spooked by Trade Wars: Matthew Winkler

Sovereign Wealth Fund Warning Light Is Flashing: Mark Gilbert

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.