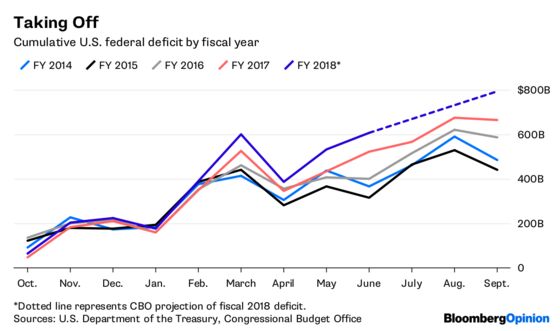

(Bloomberg Opinion) -- The federal deficit has grown a lot over the past six months. This should come as no big surprise, given the tax cuts approved by Congress and signed by President Donald Trump in December and the spending deal reached in February, but it’s still striking to see the actual numbers from the Treasury Department, which last week released data on federal revenue and outlays in June. The U.S. government’s fiscal years begin in October, so we now have data for three quarters of fiscal 2018.

The Congressional Budget Office’s latest projection, which I’ve included in the chart, is that the full fiscal-year deficit will add up to $793 billion, or 3.9 percent of gross domestic product. That’s a little bit lower than the $805 billion it forecast in April, but the change is only a technical one, reflecting updated estimates of health insurance revenue and subsidies under the Affordable Care Act and spending under the appropriations bill signed into law in March. The CBO is still projecting that the deficit will keep rising to $973 billion (4.6 percent of projected GDP) in fiscal 2019 and just over $1 trillion (also 4.6 percent of GDP) in fiscal 2020.

The CBO, in a long-term budget outlook published last month, also forecast that the deficit would reach 5.1 percent of GDP in 2028, 7.1 percent in 2038 and 9.5 percent in 2048, thanks mainly to burgeoning spending on Social Security, Medicare, Medicaid and other health-care programs, and interest on the national debt. The 9.5 percent deficit forecast for 2048 would still be lower than the 10.8 percent of GDP that the deficit hit during the Great Recession in fiscal 2009, but these CBO forecasts are meant to average out over expansions and recessions, and 9.5 percent is a whole lot higher than the average deficit since 2000 of 4.4 percent of GDP. This deficit trajectory is also probably unsustainable, likely to bring on inflation, fiscal crisis or political crisis — or all three — well before 2048 if not addressed.

But discussions of long-run budget prospects are so fraught with uncertainty and susceptible to distortion that I do wonder sometimes how useful they are. Meanwhile, we have actual numbers on revenue and spending for the first three quarters of the current fiscal year. So let’s look at those, and how they compare with the recent past.

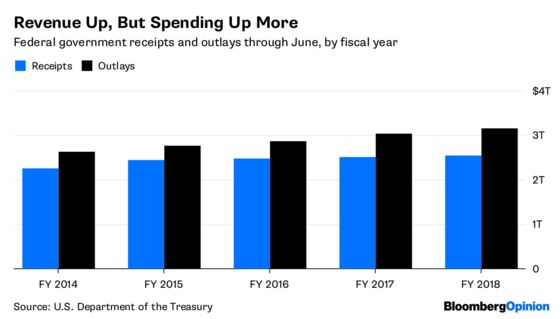

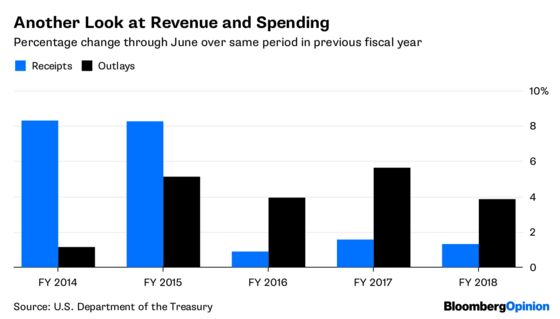

That’s because revenue growth of 3.8 percent over three years is quite weak, given the circumstances. One factor is the Tax Cuts and Jobs Act of 2017, which took effect Jan. 1 of this year. Federal receipts are still up so far this fiscal year despite the tax cuts, but only by $33 billion, or 1.3 percent. Tax revenue virtually always goes up when the economy is growing, and all indications are that receipts would be rising faster if it weren’t for the new tax law. Receipts from corporate income taxes — the main focus of the tax act — are actually down $62 billion, or 28 percent, over the same period in the previous fiscal year, while this fiscal year’s increase in overall tax revenue substantially trails that of recent years during which the economy was growing at a similar speed. (For reference, real GDP grew 3.2 percent in fiscal 2014, 2.4 percent in fiscal 2015, 1.5 percent in fiscal 2016 and 2.3 percent in fiscal 2017, and Bloomberg Economics forecasts that it will grow 2.8 percent in fiscal 2018. )

A few months of data obviously aren’t the last word on the revenue impact of the tax bill; those who claim to foresee big positive feedback effects from the tax cuts don’t see them arriving immediately. But for now the legislation is clearly tamping down tax revenue. Which is, after all, what tax cuts are supposed to do.

As for the $115 billion, or 3.8 percent, spending increase so far this fiscal year, about half of it comes from the usual suspects of Social Security, Medicare and Medicaid, reports the CBO. The retirement of the baby boomers will be driving up Social Security and Medicare outlays for a while yet, while Medicare and Medicaid are both affected by health-care cost increases that after trailing overall inflation since 2010 are now outpacing it again. Another third of the spending increase comes from interest payments on the national debt, which are rising because the debt is getting bigger and interest rates higher. The rest is due to increased defense spending. Non-defense discretionary spending is actually down infinitesimally so far this fiscal year, although it would be up by a nontrivial amount if it weren’t for some accounting decisions at the Department of Education.

Put it all together, and the deficit is $84 billion bigger so far this fiscal year than in the first nine months of fiscal 2018, and the CBO expects it to be $128 billion bigger for the full fiscal year. That would amount to about 0.6 percent of projected GDP. Economic growth, meanwhile, is as already noted expected to accelerate by 0.5 percentage points of GDP in fiscal 2018.

I don’t want to be so simplistic as to suggest a one-to-one (or, more precisely, 1.2-to-one) correlation, but it does seem like this deficit increase is an underappreciated factor in the U.S. economy’s strength this year. It may be unsustainable. It may bring big problems down the road. It surely would have been even better to do this back in 2011 or 2012, when the economy was weaker and unemployment much higher. There also surely could have been ways to structure such a stimulus that would be more advantageous to workers and less generous to corporate shareholders. But for the moment, President Trump and Congress do seem to be following the Keynesian playbook to tolerably good effect.

To contact the editor responsible for this story: Brooke Sample at bsample1@bloomberg.net

Justin Fox is a Bloomberg Opinion columnist covering business. He was the editorial director of Harvard Business Review and wrote for Time, Fortune and American Banker. He is the author of “The Myth of the Rational Market.”

©2018 Bloomberg L.P.