(Bloomberg Opinion) -- Plunge, tumble and rout are overused by the financial media to describe a market in decline, but such superlatives would not be out of place to describe what’s happening to commodities. The Bloomberg Commodity Index of 25 raw materials ranging from oil to copper to cattle dropped as much as 2.80 percent on Wednesday, the most since 2014, before closing at its lowest level since December. That brought the gauge’s decline to 8.88 percent from this year’s peak in late May.

If one thinks of raw materials as a sort of early warning system — copper is frequently called the metal with an economics Ph.D. because it often tracks the health of the world economy — then commodities are sending an incredibly distressing signal. Their performance is far worse than the relatively modest 1.05 percent drop in the MSCI All Country World Index of equities over the same period, which probably speaks more to the widespread belief among stock investors that leading central banks will stop talking about monetary tightening and continue flooding the world with cash at the first sign that the budding trade war between not only the U.S and China but also between the U.S. and its allies is causing real trouble. “There is growing concern among market participants that the trade war will affect the real economy and put the brakes on global economic growth,” Commerzbank analysts, including Carsten Fritsch, said in their daily report.

Metals were among the hardest hit on Wednesday after the Trump administration said Tuesday that it would impose a new round of 10 percent tariffs on $200 billion of Chinese goods as part of a dispute over what it says is Chinese theft of U.S. intellectual property. Copper prices plunged as much as 4 percent in London, while zinc, nickel, lead and tin also slid on the London Metal Exchange, according to Bloomberg News. Agricultural products including corn, wheat, soybeans, coffee, sugar and cotton all declined Wednesday. In the energy sector, oil fell as much as 5.52 percent, the most since February 2016.

EM GURU HAS CONCERNS

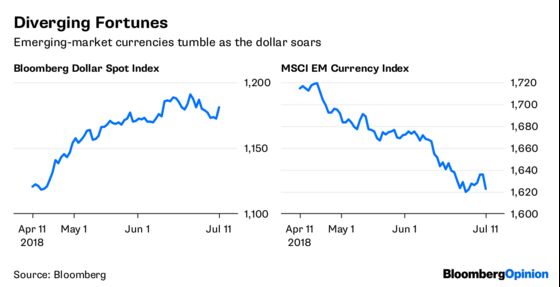

The drop in the commodities market in recent weeks is a big reason for the weakness in emerging markets. After all, many of their economies are dependent on the production and exports of raw materials. Chile’s peso weakened on Wednesday even though a day earlier the government raised its 2018 economic growth forecast to 3.8 percent. Chile is the world’s largest exporter of copper. Overall, the MSCI Emerging Markets Index of equities fell as much as 1.47 percent, while the MSCI EM Currency Index declined 0.82 percent in its biggest drop since May. “There’s no question we’ll see a financial crisis sooner or later because we must remember we’re coming off a period of cheap money,” Mark Mobius, a veteran investor in developing nations, told Bloomberg News in an interview in Singapore. Mobius, who left Franklin Templeton Investments earlier this year to set up Mobius Capital Partners LLP, predicted that the MSCI Emerging Markets Index will most likely fall an additional 10 percent by the end of the year. That would tip the gauge, which has fallen about 16 percent from a peak in late January, into a bear market. While interest rate increases by emerging-market central banks are a “short-term fix” to shoring up their currencies, they could be counterproductive for countries with high amounts of debt, Mobius said.

INFLATION FEARS SUBSIDE

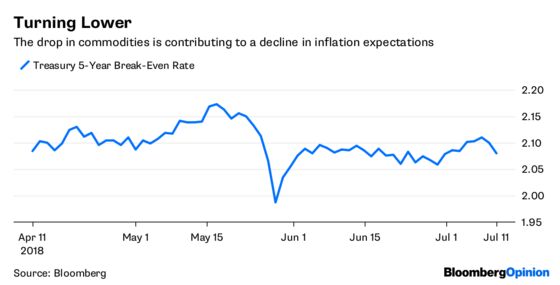

The upside to the plunge in commodities markets is that inflation expectations are being held in check, which is supporting the all-important market for U.S. Treasuries. The thinking is, if the cost of raw materials is on the decline, manufacturers feel less pressure to raise prices. Breakeven rates on five-year U.S. Treasuries, or what traders expect the rate of inflation to be over the life of the securities, dropped 2 basis points Wednesday in the biggest decline since May. At 2.08 percent, the breakeven rate has dropped from this year’s high of 2.19 percent in mid-May. Signs that inflation expectations are anchored could give the Federal Reserve cover to slow the pace of rate increases to gauge the U.S. economy’s response to the escalating global trade war. Although minutes from the Fed’s June 12-13 meeting released last week showed that officials were committed to moving toward a slightly restrictive monetary policy, there were also concerned trade wars could hurt business sentiment and investment, noting that industry contacts said it was already having an impact. Barclays strategist Michael Pond says inflation risks are skewed lower, in part because wage growth remains subdued and trade tensions may wind up depressing prices should the economy take a hit. “We’re not looking for a pickup in inflation as a result of the trade war — in fact, it could go the other way,” Pond, head of global inflation markets strategy, told Bloomberg News’s Emily Barrett and Jacob Bourne.

WHERE’S THE VOLATILITY?

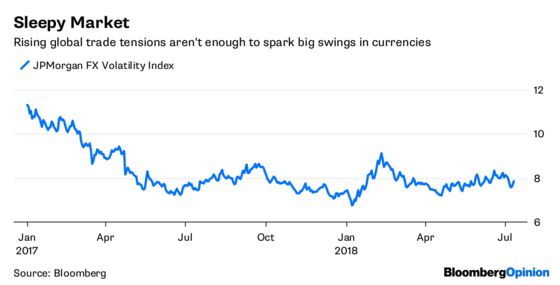

Perhaps the oddest development in all the posturing over what a trade war means for the global economy is that the $5 trillion a day currency market remains sanguine. At a reading of 7.85 on Wednesday, the JPMorgan Global FX Volatility Index is down from its high this year of 9.12 in February and last year’s high of 11.31 at the start of January. If anything, the relative calm in the foreign-exchange market should be a reassuring sign. It’s not that low volatility means there won’t be losses but more likely that traders expect the losses to be orderly and manageable. For all of President Donald Trump’s unpredictability, traders feel they have largely figured him out. That’s to say Trump will typically use bluster as a negotiating tactic, starting off with the most outrageous demands to get the other side negotiating before hashing out an agreement in a manner that lets Trump declare some sort of victory. “President Trump has a track record of starting a negotiation from an extreme position and then moving toward compromise,” John Lynch, the chief investment strategist at LPL Financial, wrote in a research report in late June. “Keep in mind that the amount of time between announced tariffs and implementation — typically 60–90 days — provides time for negotiations and that announced tariffs may not be implemented."

WHEN BULLS AND BEARS AGREE

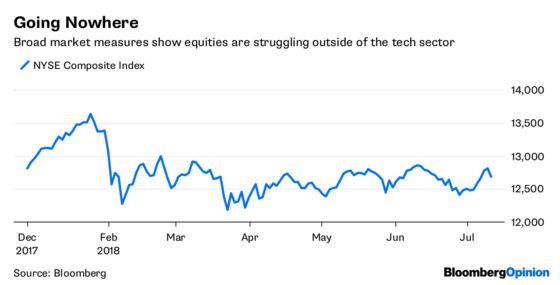

The S&P 500 Index fell from its highest on a closing basis since the start of February, dropping more than half a percent and dragging global equity markets lower. The bulls would argue that the decline is nothing to worry about because the economy is humming, jobs are plentiful and profits are booming. The bears argue that’s precisely why investors should be worried: things are so good that the risk is that the Fed keeps raising rates when valuations are rather rich. Regardless of which side you fall on, when the bulls are bullish and the bears are bearish for the same reason, it narrows the path to success for the stock market, the strategists at Leuthold Group have noted in recent research reports. This tension can be seen in the broadest measures of the stock market. While the S&P 500 is up 3.76 percent this year, that’s largely to a handful of highflying technology shares. The NYSE FANG+ Index, which is an equal-dollar weighted index of 10 tech stocks including Facebook Inc., Apple Inc., Amazon.com Inc., Netflix Inc. and Google parent Alphabet Inc., is up 32.5 percent this year. However, the broad NYSE Composite Index, which is a float-adjusted market-capitalization weighted index that includes all common stocks listed on the New York Stock Exchange, has dropped 0.99 percent. When it comes to stocks, it’s all a matter of perspective.

TEA LEAVES

In what is perhaps the biggest economic data point of the week anywhere in the world, the U.S. Labor Department on Thursday will release its monthly reading on the consumer price index. The index jumped 0.2 percent in May from the prior month and 2.8 percent from a year earlier. That was the biggest increase in the inflation rate in more than six years. The report for June is forecast to show a gain of 0.2 percent for the month and 2.9 percent from a year earlier. There’s much at stake for bond investors. Even though a rally has cut yields on benchmark 10-year Treasury notes to about 2.85 percent from 3.13 percent in May, the sense is that yields can’t go much lower. The latest Commodity Futures Trading Commission report shows that speculators have record bets against 10-year notes, implying they expect yields to rise. In other words, if the CPI report comes in even a bit below forecasts, it could trigger a big rally in bonds as traders rush to reverse their bearish bets.

DON'T MISS

The Reason Merger Arbitrage Funds Aren't Doing Well: Aaron Brown

Fed Could Avert an Inverted Curve. But It Won't: Brian Chappatta

20 Billion Pounds of Linker Orders? Don't Panic: Marcus Ashworth

Dalio’s Risk Parity Strategy Comes to the Masses: Nir Kaissar

Bitcoin Looks More Like Gold Than a Currency: Noah Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.