The Reason Merger Arbitrage Funds Aren’t Doing Well

(Bloomberg Opinion) -- Mergers and acquisitions are booming, with 2018 projected to be the first year that global deal volume breaks $5 trillion. But merger arbitrage funds, which attempt profit on perceived market inefficiencies before or after an M&A deal is announced, are not doing well. The last three months for which data are available represent the first time MAFs have lost money three months in a row, and represent the second-, third- and sixth-worst months since data begins in 1999.

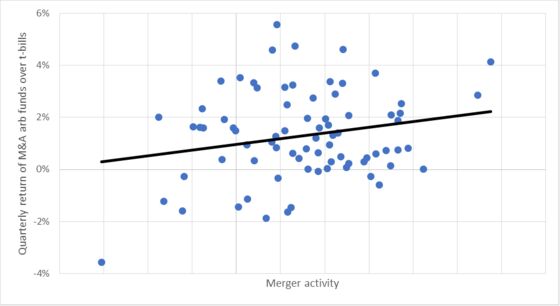

This defies the historical pattern shown in the graph below from 1997–2017, which shows higher levels of merger activity are typically associated with better returns for MAFs.

Arbitrage literally means a riskless profit, but in financial marketing it is applied to low-risk strategies. For example, a simple M&A deal might entail A seeking to buy B and offering one share of A for two shares of B. If A is selling at $40 per share and B at $15 per share, shares of B might jump to $19 on the news. An MAF would buy two shares of B for $38, short one share of A at $40, and collect a $2 profit. When the merger occurs, the two shares of B are converted to one share of A, which is used to cover the short.

There are risks, primarily that the deal won’t be completed. But MAFs have returned 5.3 percentage points per year above three-month Treasury bills over the last 20 years, with a volatility of only 3.4 percent. That’s equity-like returns with bond-like risk.

The simple story on merger arbitrage is that after a deal announcement lots of investors want to sell B stock. They could wait until the final exchange occurs and sell A stock, but they will be exposed to A’s fortunes in the interim. If they had wanted that exposure, they would have bought A in the first place. MAFs can short A’s stock and diversify the risk of the deal falling apart with lots of other deals. MAFs are also equipped to evaluate the probability and price impacts of different outcomes: completed merger, failed merger, renegotiations, new bidder.

In this story, more deal volume means more demand for merger arbitrage. Since the capital and talent devoted to this strategy doesn’t change quickly, more demand means higher price. MAFs hold out for the highest premium and safest deals. Moreover, they can increase diversification by being involved in more deals. Low deal volume means lots of capital chasing a few deals, pushing down prices and making MAFs less diversified.

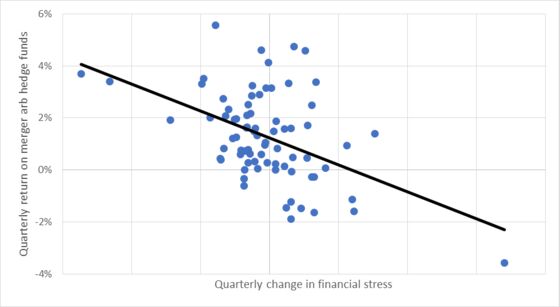

But the simple story is wrong. The chart below shows quarterly merger arbitrage returns versus changes in the Federal Reserve’s financial stress index, which is an indicator of fear, illiquidity, overleverage, credit problems and other components of a financial crisis. You can see this is a much stronger relation than the effect of deal volume on fund returns (the correlation is 0.47 versus 0.21).

In addition, the statistical association of deal volume with MAF returns is entirely driven by changes in financial stress. Increases in financial stress depress both deal volumes and MAF returns. There is no independent effect of deal volumes on MAF returns. Merger arbitrage is not a service provided to investors who don’t want to own the target company. It’s selling insurance against financial crises. A big increase in financial stress causes big losses for MAFs; a big decrease causes big gains. What’s unusual about 2018 is not that MAFs are losing money while deal volumes are increasing, it’s that deal volumes are increasing while financial stress indicators are increasing. Given the increase in financial stress, the MAF losses are expected.

This should be an investor’s first assumption about any strategy marketed as “arbitrage.” Most arbitrage strategies have attractive ratios of average returns to volatility, but not because the arbitrage manager is smart and the market is stupid, or because the arbitrage fund is providing some kind of market service. The excellent risk/return ratios are compensation of taking losses at the times no one wants to take losses, and gains at the times gains are least valued. That might or might not be a good bet for a portion of your portfolio, but be aware that you are making it.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.