(Bloomberg Opinion) -- It’s hard to believe, but the world is awash in even more debt. The Institute of International Finance in Washington said Tuesday that the global economy ended the first quarter with $247.2 trillion of debt, adding $8 trillion in the first three months of the year and $30 trillion since the end of 2016. All that debt, which amounts to 318 percent of worldwide gross domestic product, wouldn’t be much of a problem if it was being added amid a booming economy. But that’s hardly the case.

In fact, most economists are worried about an imminent slowdown in global growth, especially with the escalating trade war between the U.S. and its allies and China, rising borrowing costs and tumbling emerging-market assets. The median estimate of economists surveyed by Bloomberg is for global growth to rise 3.8 percent this year before decelerating to 3.7 percent next year and falling off a cliff to 3.2 percent in 2020. To make matters worse, major central banks look intent on pulling back the punch bowl that is otherwise known as quantitative easing regardless of the fallout. The collective balance-sheet assets of the Federal Reserve, European Central Bank, Bank of Japan and Bank of England, which grew steadily to 37.2 percent of their countries’ total GDP at the end of 2017 from less than 20 percent in 2011, are unchanged as a percentage of GDP this year, data compiled by Bloomberg show.

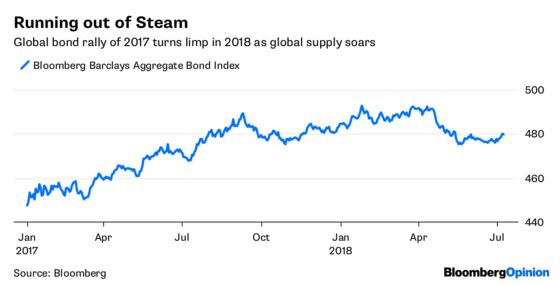

There are already signs that investors have had their fill of fixed-income assets. Demand at the U.S. Treasury Department’s auction of $33 billion in three-year notes Tuesday was the lowest for that maturity since 2009 based on the amount of bids received, continuing a trend of weak auctions. The benchmark Bloomberg Barclays Global Aggregate Bond Index has generated a loss of 1.05 percent this year after gaining 7.39 percent in 2017. The average yield on bonds in the index has climbed above 2 percent for the first time since 2014, rising from a low of 1.07 percent in 2016. While yields are still low on a historical basis, the trend is going in the wrong direction.

STOCKS STREAK HIGHER

Global equities posted their fourth straight daily gain on Tuesday, extending their rally to 2.56 percent in the longest winning streak for the MSCI All-Country World Index since the first half of May. The benchmark hasn’t risen for five straight days since February, and the odds are long that it will happen on Wednesday. That’s because of a potentially tense meeting on tap between U.S. President Donald Trump and others leaders of the North Atlantic Treaty Organization in Brussels. Any sign of discord among the members of the militarily important group — Trump has demanded that NATO countries shoulder a larger share of the alliance’s budget — could rattle investors. “Dear America, appreciate your allies, after all you do not have that many,” European Council President Donald Tusk said Tuesday after signing a joint declaration deepening the ties between the European Union and the North Atlantic Treaty Organization. Tusk’s comments followed a string of tweets by Trump accusing the EU of relying on American taxpayers for its security while charging “big Tariffs (& Barriers)” to U.S. imports, Bloomberg News reported.

YEN SIGNALS

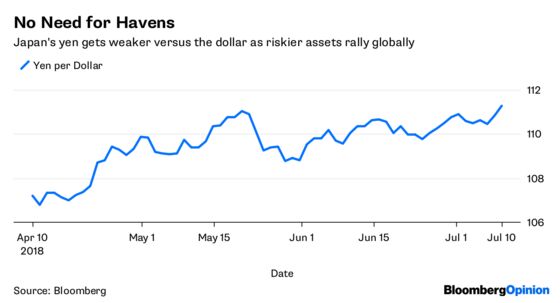

The last few trading days have been what investors call a “risk on” environment, in which riskier assets such as equities, emerging markets and junk bonds do well and haven assets such as Treasuries struggle. Whether you agree or not with the notion that it’s a good time take a flier on riskier assets, one corner of the foreign-exchange market suggests the much-talked about headwinds may be a bit overblown. That would be the yen, which dropped on Tuesday to its weakest level against the greenback since May, or 111.35 per dollar, and fell to its lowest since the first half of June against a basket of developed-market currencies. The yen is a traditional haven for traders in stressful times despite a hefty debt load for Japan that equates to about 225 percent of its economy. That’s largely because of a sizable current-account surplus that doesn’t make Japan reliant on foreign capital. Viewed through that lens, the yen’s recent weakness may be a sign that the risk-on environment is warranted. “For the time being, the market’s interest is shifting away from trade issues and focusing on hopes of robust corporate earnings and rising share prices,” Takuya Kanda, general manager at Gaitame.Com Research Institute, told Bloomberg News.

CHINA FLOWS

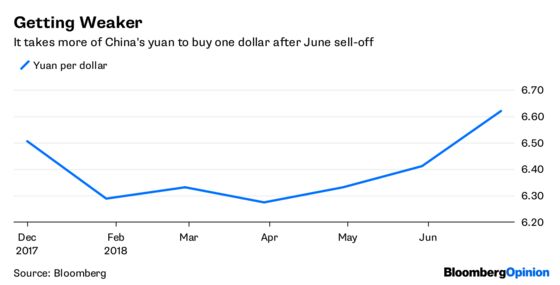

There’s no shortage of those who believe that China let its currency weaken last month by the most since it adopted a less rigid foreign-exchange regime in 2005 as a way to soften the blow on exporters from tariffs placed on Chinese goods by the U.S. There are also plenty of people who thought China was playing a dangerous game, risking a flight of capital from the country if it allowed the yuan to depreciate. It turns out that those concerns were unfounded, with overseas investors pouring the most into China’s domestic bonds in almost two years, increasing their holdings by more than 7 percent, according to Bloomberg News. The contrast underscores foreign demand for exposure to the country’s $12 trillion bond market, the world’s third-largest. China has steadily opened to international investors in part to provide a balance against domestic pressures to ferret money out. “The falling yuan is a concern, but as long as it’s not in a severe downtrend, it’s not the biggest consideration when we’re investing in local-currency bonds in China,” Manu George, director of fixed income at Schroder Investment Management Ltd. in Singapore, told Bloomberg News.

SUGAR SOURS

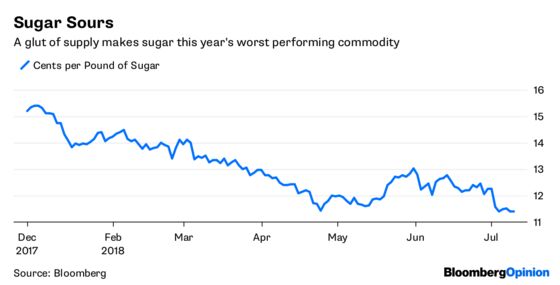

Those with a sweet tooth might like to know that the price of sugar is tumbling, with stockpiles poised to set a record. Sugar futures in New York have slumped 25 percent in 2018, the most of any member of the Bloomberg Commodity Index, which tracks returns for 22 components. Global production will top demand by 19.6 million metric tons in the 12 months that end Sept. 30, the biggest overhang ever, Brisbane, Australia-based Green Pool Commodity Specialists said in a report last month. At the same time, demand for sugar has eased as consumers become more health conscious, according to Bloomberg News’s Marvin G. Perez. While global consumption is still rising, the pace of growth has slowed to an average 1.4 percent in recent seasons, down from 1.7 percent over the past decade, according to Green Pool. Investors expect more price declines. In the week ended July 3, money managers more than tripled their net-short position, or the difference between bets on a price increase and wagers on a decline, to 54,736 futures and options, according to U.S. Commodity Futures Trading Commission data released Monday.

TEA LEAVES

The big central bank event of the week takes place on Wednesday when the Bank of Canada is widely expected to raise its target interest rates by 25 basis points to 1.50 percent. The increase will be the fourth in the past 12 months. But since the last boost in January, global trade tensions have escalated, including the U.S. slapping tariffs on Canadian steel and aluminum imports. As such, it will be interesting to see how Bank of Canada Governor Stephen Poloz weighs trade risks against an improving labor market and gains in oil prices that should bolster economic growth. And if the recent past is any indication, the Bank of Canada’s tendency will be to default to caution and wait for data to force its hand — a framework most analysts expect will produce a rate hike every half year or so, according to Bloomberg News’s Theophilos Argitis.

DON'T MISS

Corporate Bonds Are Getting Junkier: Danielle Dimartino Booth

CLOs Have Hit a Peak When Mom and Pop Show Up: Brian Chappatta

Erdogan's New Dynasty Makes Turkey Uninvestable: Marcus Ashworth

Saudi Arabia Can Ease Trump's Gas Price Fears: Liam Denning

China’s Unicorns Are Stampeding Into an IPO Quagmire: Shuli Ren

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.