Dollar Bulls Grapple With Buyer's Remorse

Americans positive about the trade war but the dollar’s strength has dropped to its lowest level in three weeks.

(Bloomberg Opinion) -- With President Donald Trump preparing to slap tariffs on Chinese goods as soon as Friday, much of the talk in financial markets is how the outperformance of American equities relative to the rest of the world is a sign investors expect the U.S. to come out ahead in any trade war. That sounds logical, until you consider the dollar.

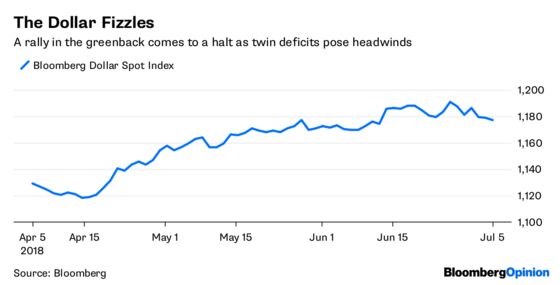

After a spurt of strength starting in mid-April, the rally in the Bloomberg Dollar Spot Index has fizzled. The gauge of the greenback’s strength has dropped to its lowest level in three weeks and is little changed from where it was at the end of May. Some might say that the dollar was due for a pause after rallying as much as 6.51 percent since mid-April, but perhaps the reason is also that the currency still faces a stiff headwind in the form of twin budget and current-account deficits. An economic slowdown that a trade war might bring won’t help. In a recent mid-year review and outlook report, JPMorgan Chase & Co. strategists led by John Norman, the firm’s head of cross-asset fundamental strategy, noted that a budget deficit of 4.8 percent of gross domestic product forecast through 2020 would rival the 5.8 percent under the Obama administration “without the justification of a global financial crisis.” Normand notes that large budget deficits aggravate a shortfall in the U.S current account, which is the broadest measure of trade because it includes investment. The current-account deficit is 2.5 percent of GDP and headed to 4 percent, Normand figures, which will “undermine the dollar structurally unless interest rates rise enough cyclically to attract sufficient capital flows from the rest of the world.”

Normand isn't alone in his concern about the dollar’s outlook. Credit Agricole foreign-exchange strategists led by Valentin Marinov wrote in a note to clients last week that “we continue to anticipate more” dollar “underperformance on the back of a further flattening” of the “yield curve and concerns about the deteriorating U.S. twin deficits.”

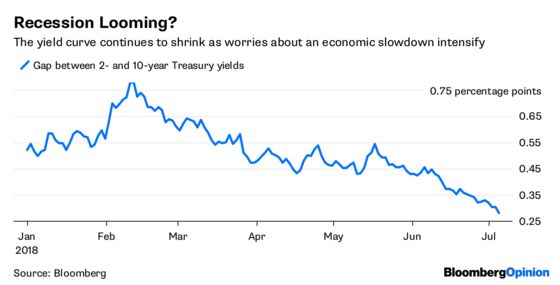

THE EVER-SHRINKING YIELD CURVE

Speaking of the U.S. yield curve, the gap between short- and long-term bond yields continues to shrink, which more economists and strategists say is a sure sign that fixed-income traders expect a big slowdown in the economy before too long. The difference between two- and 10-year Treasury note yields contracted to less 30 basis points on Thursday for the first time since 2007, narrowing to 28 basis points. The curve has shrunk from 80 basis points in February, and it would take just one more 25-basis-point rate hike by the Federal Reserve to invert the curve, which typically precedes a recession. The Fed, which is expected to raise rates again at its monetary policy meeting in late September, is closely watching the yield curve. Minutes of the Fed’s June 12-13 meeting released Thursday showed that “a number of participants thought it would be important to continue to monitor the slope of the yield curve, given the historical regularity that an inverted yield curve has indicated an increased risk of recession in the United States.” Some policy makers noted several factors, other than the gradual rise in rates, that may contribute to curve flattening, including 1) A reduction in investor estimates of longer-run neutral real interest rate; 2) Lower long-term inflation expectations; and 3) a lower level of term premiums in recent years relative to historical experience reflecting, in part, central bank asset purchases.

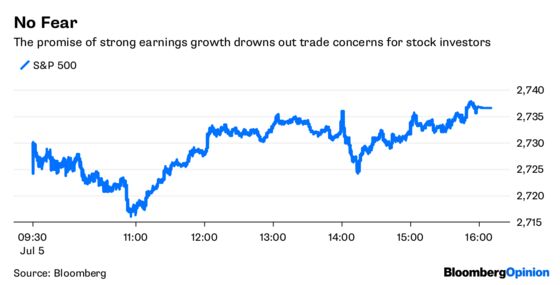

EARNINGS TRUMP TRADE

Despite the messages being sent by the currency and bond markets, it appears equity investors are mainly focused on the earnings season that is about to start. The S&P 500 Index jumped 0.86 percent Thursday, the most in four weeks, as companies prepared to post second-quarter earnings growth of 20 percent on average from a year earlier, according to data compiled by Bloomberg. That’s only slightly less than the January-March period, which experienced the fastest growth in seven years, according to Bloomberg News’s Elena Popina. Even so, the S&P 500 has pulled back in recent weeks on concern that companies may express a cautious outlook because of the damage from a potential trade war. “Companies’ forward guidance is going to be more important than it’s been in the past,” Dennis Debusschere, head of portfolio strategy at Evercore ISI, told Bloomberg News. “We have trade, we have a stronger dollar and a general feeling of nervousness around global growth. With earnings, people don’t necessarily expect anything extraordinary. With trade, they have no idea.” A recent survey of strategists by Bloomberg News shows that the median year-end projection for the S&P 500 of 2,944 hasn't budged since March. That compares with a level of 2,733 in late trading Thursday.

THE MEXICO RISKS THAT WEREN'T

Heading into last weekend’s presidential elections in Mexico, the worrywarts were working overtime. The consensus was that a victory by Trump critic and leftist candidate Andres Manuel Lopez Obrador would lead the nation's financial markets into a downward spiral. Of course, it’s still early but the reaction by investors has been rather ebullient. Mexico’s peso has rallied to its strongest against the dollar since the May 11. The benchmark S&P/BMV IPC index of equities rose 2.63 percent Thursday in its biggest gain since November 2016. Strategists credited the reversal in sentiment to market-friendly comments made by Lopez Obrador aides in recent days, including a promise to respect the independence of Mexico’s central bank. At least the nation’s citizens are feeling optimistic. A government report showed that an index of consumer confidence rose in June by more than forecast to the highest since mid-2016.

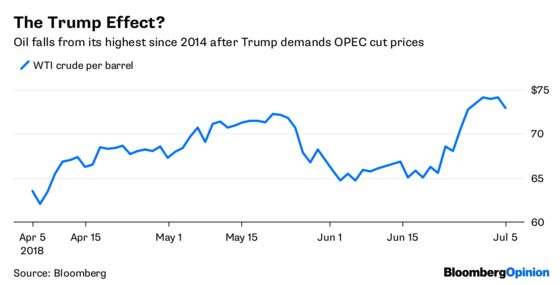

TRUMP HAS OPEC'S EAR. MAYBE.

Oil prices dropped the most in almost three weeks after Trump took to Twitter Thursday to demand that OPEC “REDUCE PRICING NOW!” Later, news broke that Saudi Arabia had cut pricing for most of its oil grades as the world’s biggest crude exporter increases production to assure buyers there is sufficient supply. There was no evidence that Saudi Arabia was responding to Trump’s demand, but it should be noted that oil didn’t really start dropping until a government report showed that U.S. crude inventories climbed by 1.25 million barrels last week as imports rose and exports fell. Analysts surveyed by Bloomberg had been expecting a median 5 million-barrel decrease because supplies typically decline this time of year amid strong demand from refiners, according to Bloomberg News’s Jessica Summers. West Texas Intermediate crude for August fell as much as $1.25 to $72.89 a barrel. Earlier on Thursday, Iran’s OPEC governor, Hossein Kazempour Ardebili, urged Trump to stop tweeting about oil, saying his missives were backfiring and driving prices higher. Perhaps, but for one day at least Trump can claim victory.

TEA LEAVES

The monthly U.S. jobs report, which is typically released the first Friday of every month, is always one of the most highly anticipated economic reports. But this Friday's release will garner more interest than usual. That’s because all eyes will be on Trump’s Twitter feed after last month, when he tweeted about an hour before the report was to be released that he was “looking forward to seeing the employment numbers at 8:30 this morning.” The report came in on the strong side. So, will Trump tweet again and tip markets off to what’s coming? And if he doesn’t tweet, will that mean the report will be weak? Regardless, the big question is how the bond market will likely react. An informal survey of clients by the top-ranked rates strategist at BMO Capital Markets found that 58 percent would jump in and buy bonds if the market dipped after the report, a higher amount than the 45 percent that usually say they would buy in such a scenario based on past surveys. Some 10 percent said they would buy if there was a rally, and 54 percent said they would “do nothing” in a rally, compared with 33 percent who would “do nothing” in a sell-off.

DON'T MISS

Vanguard's Not Only Threat to Active Managers: Eric Balchunas

The ECB Throws Water on the Investor Sunlounger: Marcus Ashworth

Beware China Equity Bulls Promising Rich Returns: Shuli Ren

Copper Pitches a Curveball at Bullish Hopes: David Fickling

Want Faster Economic Growth? Embrace Diversity: Noah Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.