The Fed Needs to Pass Its Own Stress Test

.jpg?auto=format%2Ccompress&w=200)

(The Bloomberg View) -- The largest U.S. banks have just cleared the first hurdle of this year’s Federal Reserve stress tests, demonstrating that they have enough loss-absorbing capital to survive a hypothetical crisis. Now, investors are waiting to hear how much of that capital the banks will be allowed to pay out in the form of dividends and stock buybacks.

They should be careful what they wish for. If banks disburse much more than they have been, they will start chipping away at the bedrock of the financial system.

For the second year in a row, U.S. banks passed the tests with flying colors. The Fed presented them with a worst-case scenario that included 10 percent unemployment and a 65 percent stock-market decline, and they all made it through without breaching regulatory minimum capital levels.

In next week’s second round, the Fed will assess the banks’ capital plans and decide how much it will allow them to spend on dividends and stock buybacks. Amid the Trump administration’s regulatory rollback — which includes proposals to make the tests less stressful — analysts expect total payouts to increase 25 percent over last year, by about $30 billion.

Such largess would be unwise, for at least two reasons.

First, banks are more fragile than the stress tests suggest. On average, the largest U.S. institutions have about $7 in equity for each $100 in mortgages, corporate loans and other assets (according to international accounting standards) — not enough to cover what they were projected to lose on loans and securities in the midst of the last crisis. It’s also less than half what economists at the Minneapolis Fed estimate they would need to lower bailout risk to an acceptable level. The tests miss this because they don’t take into account important aspects of real crises, such as the way trouble suffered by counterparties can amplify banks’ losses.

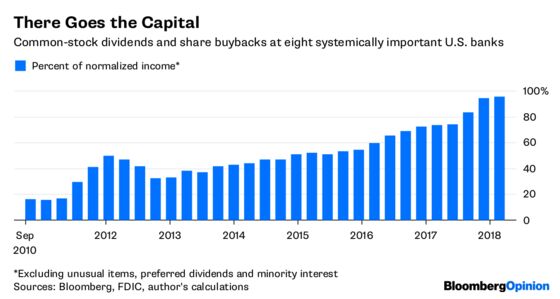

Second, banks are already returning almost all their earnings to shareholders. In the 12 months through March, the eight most systemically important U.S. banks spent 95 percent of their normalized income, or more than $100 billion, on dividends and stock buybacks (see chart below). Instead of paying out more at this point in the business cycle, it would be more prudent to build up equity capital to prepare for the inevitable downturn.

The Fed has been known to have trouble striking the right balance between keeping investors happy and protecting the financial system. In 2008, just before the government was forced to step in and rescue troubled banks, it allowed them to pay out tens of billions of dollars in dividends. It must act more responsibly this time around.

©2018 Bloomberg L.P.