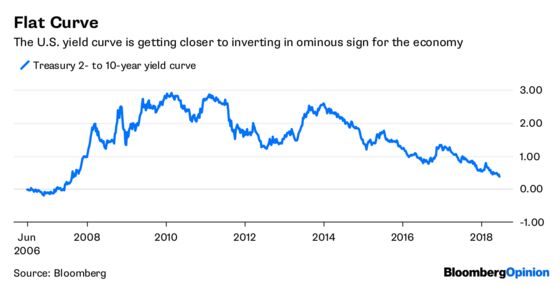

(Bloomberg Opinion) -- Pray for the global economy. For much of the past year or so, investors and economists have anxiously watched the relentless shrinkage of the gap between short- and long-term U.S. bond yields to the narrowest levels since 2007. After all, an inversion — when long-term yields fall below short term ones — preceded each of the last seven recessions. But while everyone has been so focused on the U.S, they seemed to have missed the global yield-curve inversion.

Within the past two months, the yield on an ICE Bank of America index of government bonds due in seven to 10 years has fallen below the yield on an index of bonds due in one to three years for the first time since the first half of 2007. The strategists at JPMorgan Chase & Co. said they were seeing the same thing in indexes they manage. Although the U.S. economy is in solid shape, there have been signs of weakness in the euro zone, China and emerging markets over the past month. A Citigroup Inc. index shows that worldwide economic data is missing estimates by the most since 2013. And within the past few weeks, both the International Monetary Fund and the Organization for Economic Cooperation and Development said that although tax cuts and fiscal spending were boosting the U.S. economy now, those moves are increasing risks to the global economy by causing debt to rise and potentially stoking inflation and the dollar.

The clouds over the world economy are “getting darker by the day,” IMF Managing Director Christine Lagarde said last week. To be sure, no significant individual market has an inverted yield curve, and the gap between two- and 10-year U.S. yields is 37 basis points. The JPMorgan strategists said indexes show an inversion because of how they are composed. U.S. bonds have a much higher weighting in the one- to three-year bucket, or about 50 percent, than in the seven- to 10-year bucket, where it has a weight of only 25 percent. That is important because short-term yields are higher in the U.S. than in much of the rest of the world, and there are a lot more short-dated U.S. government bonds relative to longer-dated ones. Still, who wants to bet against the track record of the yield curve?

WHAT'S TO WORRY ABOUT?

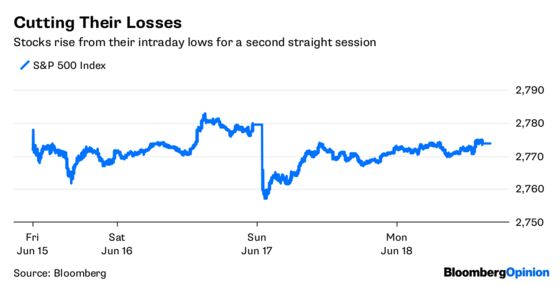

U.S. stocks fell on Monday, with the S&P 500 Index posting its first back-to-back decline this month. Even so, most investors were shocked by the relatively small declines – which total 0.31 percent – given the budding trade war between the U.S. and China and the concerns over the yield curve. To the bulls, that just proves how resilient the market is as tax reform spurs companies to go all out on stock buybacks. According to DataTrek Research, stock prices imply a 27 percent annual increase in dividends or buybacks, which the firm says is achievable given earnings expectations call for 20 percent growth. And what about the flattening yield curve? A yield curve that flattens but falls short of inverting has historically offered a strong backdrop for stocks, according to Bloomberg Intelligence strategists Gina Martin Adams and Ira Jersey. “As stocks tend to react quite well in bear-flattening regimes, investors should enjoy a period of relative tranquility for now,” they wrote in a report on Monday. “The S&P 500 has recorded average annual returns of almost 15 (percent) in similar periods since 1990. Even inversions usually aren't terrible, with average gains of 9.3 (percent).” The closely watched “fear gauge” is not sounding the alarm. The CBOE Volatility Index, or VIX, was at 12.56 Monday, down from the high for the year of 37.32 on Feb. 5 and in line with the average of 13.28 over the past 12 months.

WHERE'S THE BOTTOM?

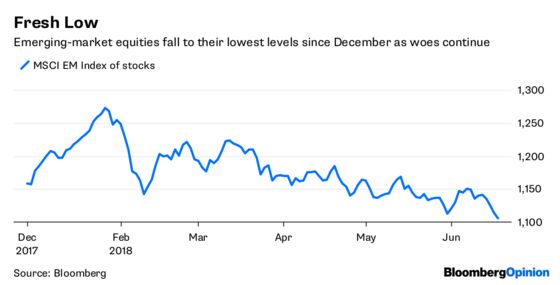

Another day, another beating for emerging markets. The MSCI EM Index of stocks closed at a fresh low for the year Monday while an MSCI index of emerging-market currencies extended its decline to 4.55 percent from its high for the year on April 3. The carnage seems to be indiscriminate, with a 2.11 percent drop in Poland's stocks leading EM equities lower on the day and a 1.50 percent decline in South Africa's rand pacing currencies. With OPEC clashing over output, Turkish elections looming and the likelihood of fallout from Argentina’s foreign-exchange crisis continuing, the prospect of a protracted trade war between the world’s two biggest economies merely served to cast a longer pall over emerging markets, according to Bloomberg News. Trade wars “have the potential to disrupt an otherwise positive economic outlook, if they were to trigger broad-based retaliatory actions,” Silvia Dall’Angelo, a London-based senior economist at Hermes Investment Management, told Bloomberg News. “The uncertainty concerning trade policies has the potential to negatively affect confidence, in turn holding back investment decisions.” Investors demand an extra 3.56 percentage points in yield to own emerging-market sovereign debt, the most since December 2016, JPMorgan indexes show.

WHAT DID SOUTH KOREA GET?

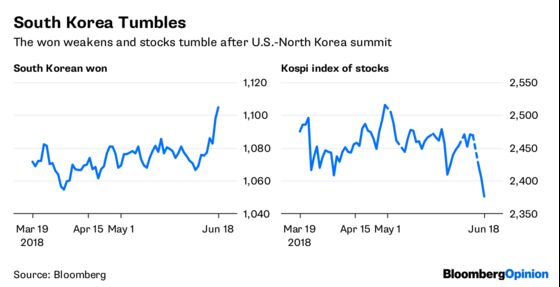

To hear U.S. President Donald Trump tell it, the U.S. “got so much” out of his summit with Kim Jong Un in Singapore last week. Maybe, but what did South Korea get? Traders have pushed the South Korean won down in four of the past five trading days to its weakest level since November. The benchmark Kospi index of stocks has declined for three consecutive days, falling 3.75 percent. Of course, South Korea has much to lose from a potential trade war between the U.S. and China, but its healthy current-account surplus should help alleviate any fallout. Perhaps what investors are truly worried about is the decision by Trump to halt military exercises with South Korea in the region. Such a move could immediately put South Korea at greater risk. After all, strategists point out that the agreement reached last week between Trump and Kim failed to lay out a timeline for the denuclearization of North Korea or provide details of how the U.S. would verify its compliance. "Geopolitical risk owing to historical tensions versus North Korea have ebbed, but remain elevated," Moody's Investors Service said in a note Monday affirming South Korea's Aa2 rating. "Considerable uncertainties related to the peace process persist. These concern the resolution of major issues, such as the extent and pace of denuclearization or disarmament of North Korea and the role of the U.S. in providing regional security guarantees in part through the maintenance of a considerable military presence in South Korea."

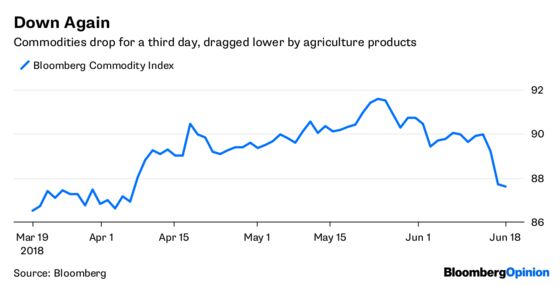

NOT SO HOT COMMODITIES

As if the hit from tariffs weren't enough, agriculture products are getting slammed because of unfavorable weather. The Bloomberg Agriculture Spot Index fell for a third consecutive day on Monday to its lowest since early February. Some of the big losers were corn, wheat, cotton and lumber. Corn futures for December delivery in Chicago dropped as much as 1.9 percent to $3.75 per half a bushel, the lowest price since the contract began trading in December 2014. The warm, wet weather in the U.S. Midwest over the last few days is seen as good for crops, Ted Seifried, chief market strategist for Zaner Group LLC, told Bloomberg News. Cotton for December delivery dropped 2.3 percent after as many as eight counties in southwestern areas of West Texas received as much as 3 inches (7.6 centimeters) of beneficial rain during the weekend, boosting crops, according to Bloomberg News. It's not all bad news for commodities. Oil and gasoline prices jumped on reports that OPEC was discussing a smaller-than-expected output increase when producers meet in Vienna this week.

TEA LEAVES

This is a big week for U.S. housing data, which is sure to receive more scrutiny than usual given the many crosscurrents currently buffeting the market. On the one hand, the market is benefiting from the lowest unemployment rate since 2000, and inventories of homes for sale are low, helping to push up prices. On the other, mortgage rates have crept up to levels not seen since 2011 and a budding global trade spat is causing key building materials to soar. On Monday, a National Association of Home Builders/Wells Fargo report showed that sentiment among U.S. homebuilders fell in June to match the lowest level this year. Higher lumber prices as a result of tariffs have added almost $9,000 to the price of a new single-family home since January 2017, the Washington-based NAHB said. On Tuesday, the government may say that housing starts rose 1.9 percent in May after falling 3.7 percent in April, according to the median estimate of economist surveyed by Bloomberg. While that sounds good, keep in mind that results fell below expectations in each of the past three months. Permits are forecast to fall for a second month, dropping 1 percent. Then on Wednesday, the National Association of Realtors is forecast to say that existing home sales rose 1.1 percent in May after a decline of 2.5 percent in April.

DON'T MISS

History's Not on Market's Side in a Trade War: Komal Sri-Kumar

Bonds Reflect Diverging Growth Prospects: Mohamed A. El-Erian

Bayer's Jumbo Bond Puts the Fed in Its Place: Marcus Ashworth

Bitcoin Breaking the Internet Is a Cry for Help: Lionel Laurent

It's Trump Sanctions, Not OPEC, That Are Lifting Oil: Julian Lee

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.