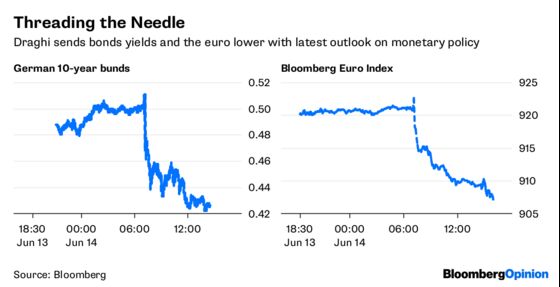

(Bloomberg Opinion) -- European Central Bank President Mario Draghi pulled off a seemingly impossible task Thursday: He announced policy makers will phase out bond purchases by the end of this year without causing either the euro to soar or bonds and stocks to tumble. In fact, the opposite occurred, providing yet more evidence that efforts by the world's biggest central banks to unwind their quantitative easing measures might not be as disrupting to markets as first feared.

The key for Draghi was that he also said the ECB will keep interest rates unchanged at record lows at least through mid-2019, a longer timeframe than investors anticipated. The Bloomberg Euro Index, which measures the currency against its major peers, promptly tumbled as much as 1.40 percent, the most since 2015. Germany, France, Spain and even Italy all saw their bonds rally, pushing yields lower. The Stoxx Europe 600 Index of equities surged the most in more than two months. “The reaction shows that the market had so far assumed that the end of QE would mean the start of a normalization process, which it is not,” Thu Lan Nguyen, a strategist at Commerzbank AG, said in emailed comments to Bloomberg News.

It would tough for the ECB to normalize policy at the same time it's cutting its forecasts following a spate of soft economic data out of the region recently. ECB staff now see the economy expanding just 2.1 percent this year, down from a prior forecast of 2.4 percent, before slowing to 1.9 percent in 2019 and 1.7 percent in 2020, according to new estimates released Thursday.

TOP DOLLAR

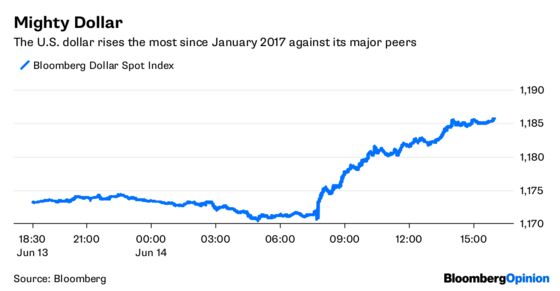

The byproduct of a weaker euro is, of course, a stronger dollar, which brings its own implications. The Bloomberg Dollar Spot Index jumped as much as 0.98 percent, the most since January 2017, to a new high for the year. The greenback is also getting a boost from a more hawkish Federal Reserve, which on Wednesday signaled that it now expects to raise interest rates four times this year. Higher rates tend to attract capital from international investors, which helps to explain a rally in Treasuries Thursday that pushed 10-year Treasury yields further below the psychologically important 3 percent level. Two-year Treasuries now yield 3.20 percentage points more than similar-maturity German bunds, up from about 2 percentage points this time last year and the most since at least 1990. And while Europe's economy shows signs of slowing, the U.S. economy is picking up. The Commerce Department said Thursday that U.S. retail sales rose in May by the most in six months. Measures of gross domestic product suggest the economy is expanding at a greater than 4 percent annualized rate this quarter. “The U.S. is accelerating, and just about everyone else is decelerating,” Nariman Behravesh, chief economist at IHS Markit, told Bloomberg News. “There’s no question in my mind that the U.S. is leading the pack.”

U.S. STOCKS OUTPERFORM

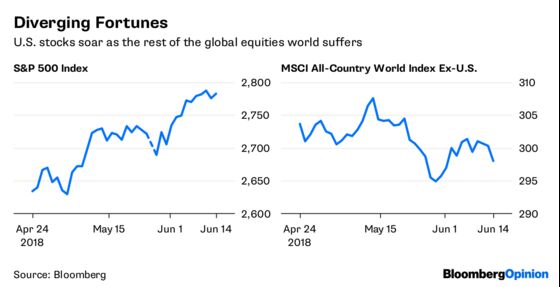

Perhaps the most visible sign of the economic divergence between the U.S. and the rest of the world is in the stock market. Yes, the S&P 500 Index had a great year in 2017, rising 19.4 percent, but that performance trailed the rest of the world as the MSCI All-Country World Index excluding the U.S. gained 24.06 percent. More recently, though, the tables have turned, with the S&P 500 gaining about 7.75 percent since early April compared with a decline of 0.60 percent for the rest of the world. While it's true that U.S. corporations are benefiting from tax-law changes, the International Monetary Fund warned on Thursday that tax cuts and public-spending hikes are increasing risks to the global economy by boosting debt, potentially stoking inflation and pushing the dollar higher. The loosening of the purse strings in Washington raises the risk of an “inflation surprise” for markets, the IMF said, according to Bloomberg News' Andrew Mayeda. And pricing pressures could in turn force the Fed to hike interest rates faster than expected. The IMF, which last week announced a record $50 billion loan program for Argentina, also said it’s seeing signs that U.S. fiscal policy may be causing capital flight from emerging markets.

MORE EMERGING-MARKET PAIN

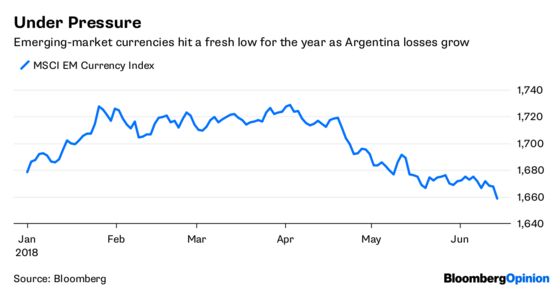

Emerging-market equities and currencies took another hit on Thursday. The MSCI EM Index of stocks fell as much as 1.25 percent, while another MSCI gauge tracking their currencies tumbled to its lowest level since December. Emerging-market bonds have also been under pressure: The Bloomberg Barclays index that tracks the dollar-denominated bonds of emerging-market borrowers has fallen 4.02 percent this year through Wednesday, the most among 19 major fixed-income markets tracked by Bloomberg. The Institute of International Finance in Washington estimates that more than $365 billion of EM government bonds and syndicated loans will come due in 2019, up from $185 billion this year and $160 billion in 2017. That means the more the dollar appreciates and U.S. rates rise, the more expensive it will be for emerging-market borrowers to refinance this debt. Argentina has been particularly troubled. Its peso tumbled to a new low on Thursday amid reports a group of central bank directors will depart from the institution, and as a truck drivers’ strike threatened to disrupt the country’s economy. The peso dropped as much as 5 percent on Thursday, bringing its decline for the year to more than 30 percent, the worst performance in emerging markets. Even more disturbing are signs that China's economy may be slowing, as recent data has fallen short of forecasts and its central bank chose not to follow the Fed in raising rates this week.

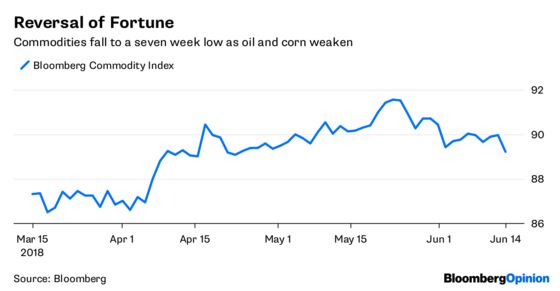

COMMODITIES DIP

Growing concerns over China, the world's second-largest economy and one of the biggest consumers of raw materials, and emerging-markets in general help explain recent weakness in the commodities market. The Bloomberg Commodity Index fell as much as 0.99 percent Thursday to its lowest level since in seven weeks. It's safe to say that the declines have caught many commodity investors off guard. A monthly survey by Bank of America Merrill Lynch released this week found that investor allocations to commodities is the highest in eight years. Some of the big losers in recent weeks in the commodities market include oil, gasoline, aluminum, corn and wheat. Oil has been under press amid signs that OPEC and its allies may agree to increase production when they meet in Vienna next week. It’s “inevitable” the cartel and its allies will decide to boost output gradually when they meet, Saudi Oil Minister Khalid Al-Falih said Thursday. Corn futures for December delivery fell as much as 3 percent to $3.85 a bushel on the Chicago Board of Trade on Thursday, the contract’s lowest level since Jan. 24. U.S. crop conditions have been “perfect” after planting, while trade tensions spurred negative sentiment, Ryan Fletcher, director of institutional sales at INTL FCStone in Chicago, told Bloomberg News.

TEA LEAVES

It's been a big week for central bankers, and it's not over. First, Fed Chairman Jerome Powell delivered a surprise by saying that he will start having a press conference after each Federal Open Market Committee meeting starting in January. Then, the ECB's Draghi

Mario Draghi said the euro-area economy is strong enough that it can phase out bond purchases by the end of the year. So, will Bank of Japan Governor Haruhiko Kuroda make it three-for-three by signaling something new when he and his colleagues wrap up their monetary policy meeting in a few hours? The chances are slim. Bloomberg Intelligence economist Yuki Masujima expects little fireworks, with the BOJ likely leaving its accommodative policy settings unchanged, including holding its key rate at negative 0.1 percent, in an effort to spur inflation, which remains far below the central bank's 2 percent target. "The economy has sent a mix of mildly positive and negative signals since the last board meeting in late April, but nothing that alters the picture of steady, if slow, progress on reflation," Masujima wrote in a research note.

DON'T MISS

Draghi's Masterclass in Something for Everyone: Marcus Ashworth

Bill Gross 'Trade of the Year' Misses Key Fact: Brian Chappatta

Powell Orchestrates a Masterful Move: Danielle DiMartino Booth

Goldman Sachs Backs an ETF That Returns the Love: Stephen Gandel

Debating Why Americans Are So Down in This Economy: Sen, Smith

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.