Trade Risks Are Evident in Markets If You Look Hard Enough

(Bloomberg Opinion) -- Following the disastrous Group of Seven summit this weekend, where President Donald Trump upended a carefully crafted effort at unity among the world's top economic powers, it's safe to say that most investors were probably expecting equities to stumble Monday. Instead, the MSCI All-Country World Index of global stocks closed at its highest level since March 14.

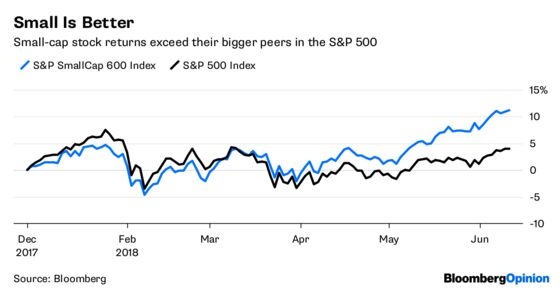

A sign of complacency? Perhaps, but digging a little deeper beyond the market headlines reveals a good amount of jitters over the potential for a budding trade tiff to devolve in a legitimate trade war. That can be seen in the performance of the Standard & Poor's SmallCap 600 Index, whose constituents are mainly domestic companies with hardly any international operations that would be exposed to tariffs and a higher dollar. The gauge closed at a fresh high on Monday, extending its gain this year to 11.2 percent. By contrast, the S&P 500 Index, which is chock full of companies with international exposure, is up only 4.05 percent this year. That marks a reversal from 2017, when the S&P 500 gained 19.4 percent while the S&P SmallCap rose just 11.7 percent. Here's another way that investors are putting a greater premium on companies that might be insulated from a trade war: At 20.3 times expected earnings, small-cap stocks are more expensive than bigger peers in the S&P, which has an average price-to-future-earnings ratio of 17.5 times. The gap of 2.84 times has expanded from 2.16 at the end of March.

"The idea that small caps might provide a ‘trade war hedge’ or ‘dollar hedge’ is preposterous, but it’s one that many investors may have accepted as an excuse to rotate into small cap risk,” Peter Cecchini, the global chief market strategist at Cantor Fitzgerald, wrote in a research report at the end of May and repeated on Monday. "We continue to feel strongly that equity markets broadly will soon respond to building global risks, just as Treasuries and volatility markets have."

THE EURO IS SAFE — FOR NOW

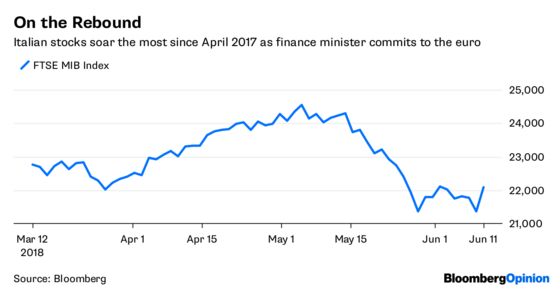

The Great Italian Debt Crisis of 2018 is over. Maybe. If you blinked, you may have missed it. The Bloomberg Euro Index was poised to close Monday at its highest level in almost three weeks after Finance Minister Giovanni Tria made assurances that the country would stay committed to the shared currency. Tria told the Corriere della Sera newspaper over the weekend that there was “no discussion” to leave the common currency and that the government would also block any market conditions that would “push toward an exit.” The Bloomberg Euro Index fell to its lowest since July at the end of last month on just such a possibility, while Italian stocks and bonds tumbled. But Tria's comments show that — once again — betting on a member of the euro leaving the currency bloc is a fool's errand. European Central Bank President Mario Draghi didn't even have to reassure markets that he would do "whatever it takes" to make sure the euro didn't break up, as he did in 2012 when Greece was on the precipice. Italy's benchmark FTSE MIB Index of stocks surged 3.42 percent Monday in its biggest gain since April 2017. Italian 10-year bond yields fell 29 basis points to 2.84 percent. While that is still far above the 1.71 percent level from where they traded in late April, recall that they had reached 3.44 percent at the end of May amid concern about the country’s future in the euro area after the Five Star Movement and the League — two euro-skeptic parties — formed a coalition.

VOLATILITY RULES EM FX

One of the biggest laments of investors has been the lack of volatility in financial markets globally. Maybe they should look at emerging-market currencies, where the JPMorgan Emerging-Market Volatility Index has just jumped to its highest since March 2017. By contrast, the CBOE Options Volatility Index, or VIX, which measures equities, is at about its lowest since January, and the Merrill Lynch MOVE Index covering bonds is well below its highs for the year. It certainly has been interesting times for emerging markets. Last week featured two surprise interest-rate hikes, a market meltdown in Brazil, Argentina’s $50 billion International Monetary Fund loan rescue, rising fears of a trade war and the realization that the end is nigh for stimulus in Europe, according to Bloomberg News. The currencies of Turkey, Brazil, Mexico, Russia and South Africa are experiencing the world’s biggest increases in their implied volatility gauges this quarter amid the worst period for developing-nation currencies since China’s shock devaluation in the third quarter of 2015, according to Bloomberg News's Srinivasan Sivabalan. The worst-hit is Turkey’s lira, whose measure of one-month implied volatility jump 159 percent and is near its highest level since January 2009.

OPEC FISSURES

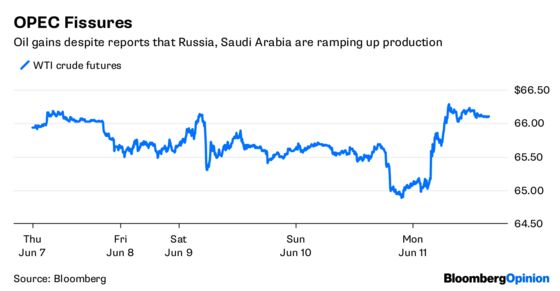

The coming meeting between OEPC and its allies in Vienna on June 22-23 is shaping up to be a can't-miss event. Crude pushed higher Monday, reaching $66.35 a barrel, as oil traders shrugged off a report that Russia lifted crude output 140,000 barrels a day above its cap in the first week of June to the highest in 14 months. Although the report suggests a potential schism in Russia's alliance with OPEC to curb production, it's notable that Saudi Arabia raised production last month to the highest since October, Bloomberg News reported, citing a person familiar with the kingdom’s disclosures to the cartel. President Vladimir Putin of Russia said last month that the “arrangements were never intended to remain in force forever.” “Russia’s key argument would be that the deal has reached its goal -- the market is balanced -- and now it’s time to think of a supply increase,” Andrey Polischuk, an energy analyst at Raiffeisen Centrobank in Moscow, told Bloomberg News. Hedge funds cut their net-long position in West Texas Intermediate — the difference between bets on a price increase and wagers on a drop — by 3.3 percent to 313,450 futures and options during the week ended June 5, the least since October 2017, data from the U.S. Commodity Futures Trading Commission show. WTI has closed below its 50-day moving average every day since the start of the month, a bearish signal, according to Bloomberg News's Jessica Summers.

SOUTH KOREAN RISKS

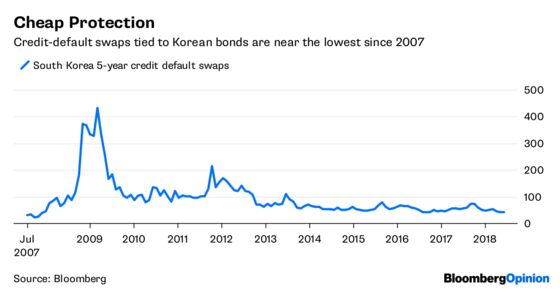

Many pundits will certainly opine on whether the historic summit between Trump and North Korean leader Kim Jong Un is a success and which side came out on top. For a more impartial view, keep an eye on markets, specifically the market for credit-default swaps tied to South Korea government bonds. A rise in the cost of the derivatives could signal that investors think the U.S. failed to make much headway in getting Kim to give up his nuclear weapons; a decline the opposite. Regardless of the outcome, investors might want to consider betting on a rise in the swaps, according to BNP Paribas Asset Management. Prices of the swaps are hovering near the lowest in more than a decade, suggesting investors see little risk in owning the underlying government debt. “It’s very attractive to buy protection,” said Jean-Charles Sambor, the deputy head of emerging-market fixed income at BNP Paribas Asset, who oversees the equivalent of $671 billion globally, told Bloomberg News. “The risks are asymmetric. That’s a good way to hedge your portfolio.” Five-year credit-default swaps on Korean notes have fallen nine basis points this year to 43.5 basis points amid easing tensions in the Korean peninsula, according to Bloomberg News's Lilian Karunungan. It’s the cheapest among the contracts offered by seven major emerging markets in Asia based on data compiled by CMA.

TEA LEAVES

It's a big week for global geopolitical and economic news. Besides the Trump-Kim summit, the Federal Reserve, European Central Bank and Bank of Japan will hold policy meetings with big implications. But there's no shortage of investors who feel that biggest news of the week will be Tuesday's U.S. inflation report. The report could either fuel or damp concerns that i nflation is accelerating and help determine whether the Fed raises rates three or four times this year. The median estimate of economists surveyed by Bloomberg is that the U.S. will say its consumer price index rose 0.2 percent in May, excluding food and energy costs, compared with a gain of 1 percent in April. That translates into a 2.2 percent increase from a year earlier, the most since February 2017. Recall that April's CPI report fell below forecasts, spurring a rally in stocks and bonds while causing the dollar to drop. Even so, "a significant share of policy makers opined at the May (Federal Open Market Committee) meeting that the underlying inflation trend may not have actually changed; rather, it might merely have been lifted temporarily by transitory factors, such as financial services costs," Bloomberg Intelligence economists Carl Riccadonna and Niraj Shah wrote in a preview report published Friday.

DON'T MISS

Gaming the Fallout from a Trade War on the Fed's Plans: Tim Duy

What to Expect From Fed and ECB This Week: Mohamed A. El-Erian

Italy Bonds Rejoice in Statement of the Obvious: Marcus Ashworth

Cash Is King Because It Finally Pays Something: Brian Chappatta

The Permian Blowout Is Apparently Never-Ending: Liam Denning

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.