Flat Yield Curve May Result in a More Aggressive Fed

Whether an inverted yield curve will cause the Fed to rethink its tightening plans is the big debate

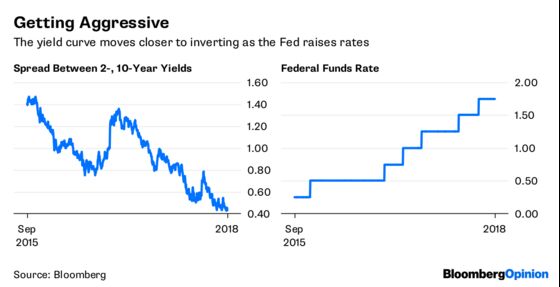

(Bloomberg Opinion) -- By all accounts, the Federal Reserve is intent on pushing ahead with its plan to gradually raise interest rates despite some strong signals in the bond market that policy makers risk going too far. Specifically, I'm talking about the yield curve, which is the flattest since 2007 and is rapidly heading toward an inversion.

The question of whether an inverted yield curve, which is traditionally a very prescient recession indicator, will cause the Fed to rethink its tightening plans is shaping up to be the next big debate among policy makers, with potentially major consequences for financial markets. The answer may lie in recent comments by key Fed officials who suggest an inversion may not mean what it has in the past.

The implications for investors are two-fold. First, the Fed may be very aggressive when boosting rates over the next year. Not aggressive in the pace of rate hikes, but aggressive in the willingness to keep increasing them despite an inverted yield curve. Investors should not discount the Fed’s intentions to continue hiking rates, especially if the economic data remains strong. Second, the Fed is playing with a spark that might kindle the next recession sooner rather than later. Maybe the yield curve is not the signal it once was, but history is not on the Fed’s side with this bet.

During monetary tightening cycles the yield curve flattens as rates on short-term bonds rise more quickly than rates on long-term bonds. The curve tends to flatten nearly completely as the economy reaches the mature stage of the business cycle and the Fed pushes policy rates toward their neutral level. At about 45 basis points, the difference between two- and 10-year Treasury note yields is down from about 125 basis points when the Fed began its current rate hiking cycle in December 2015. A flat yield curve can coexist with an extended period of economic growth, such as during the late 1990’s.

An inverted yield curve, where short-term rates rise above long-term rates, preceded each of the past seven recessions. As such, it would be foolish to ignore an inversion. To be sure, some central bankers are concerned, namely St. Louis Federal Reserve President James Bullard and Dallas Federal Reserve President Robert Kaplan. These concerns found their way into the minutes of the May Federal Open Market Committee meeting:

…several participants thought that it would be important to continue to monitor the slope of the yield curve, emphasizing the historical regularity that an inverted yield curve has indicated an increased risk of recession.

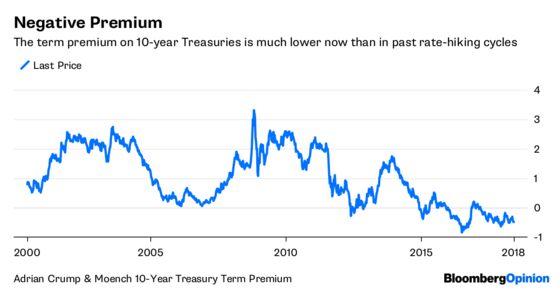

This suggests policy makers would hesitate to continue raising rates if the curve inverts. But in a recent speech, Fed Governor Lael Brainard argued that the yield curve may be a misleading indicator due to lower yields on longer-dated assets compared with past tightening cycles. The lower yields are attributable to a lower neutral interest rates and a low term premium, or the additional return required by investors to compensate for the additional risk of holding longer-dated bonds.

Low term premiums arise from a number of potential sources, including the Fed's large-scale asset purchases that were designed to suppress yields. As the Fed reduces its more than $4 trillion of balance-sheet assets, Brainard anticipates the term premium will rise. Another explanation for low term premiums is lower and more stable inflation expectations than in past cycles, a factor likely to continue to hold given the Fed’s commitment to an inflation target.

The low long-term rates attributable to a low term premium imply the yield curve will invert at lower levels of policy rates than in the past. This opens up the possibility the yield curve will invert at a policy rate that is not high enough to induce a recession. Brainard acknowledges that if the term premium remains low, the path of rates described in the Fed’s Summary of Economic Projections would likely invert the yield curve though “there would probably be less adverse signal from any given yield curve spread.”

The implication for policy according to Brainard:

It is important to emphasize that the flattening yield curve suggested by the SEP median is associated with a policy path calibrated to sustain full employment and inflation around target. So while I will keep a close watch on the yield curve as an important signal on how tight financial conditions are becoming, I consider it as just one among several important indicators. Yield curve movements will need to be interpreted within the broader context of financial conditions and the outlook and will be one of many considerations informing my assessment of appropriate policy.

What this tells me is that Brainard is primed to dismiss the negative signals from the yield curve. This is important because an inversion is a long leading indicator, often occurring a year or more before a recession. In other words, the curve is likely to invert well before the economy reaches the peak of the business cycle, a time when virtually all of the data will be looking solid. Specifically, unemployment will be low and central bankers will be fretting about overheating.

Sound familiar? It should. It is exactly the environment the Fed currently faces. If key leadership at the Fed is primed to dismiss the yield curve as an indicator, the data will likely compel the policy makers to keeping raising rates even after the yield curve has inverted.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.