Trump Better Start Liking a Strong Dollar, and Fast

(Bloomberg Opinion) -- President Donald Trump told CNBC in January that "ultimately I would like to see a strong dollar." Nobody really believed that, since Trump said a year earlier that the greenback was too strong and "it's killing us." The truth is, a weaker dollar would go a long way toward narrowing the chronic trade deficit – something Trump obsesses over — by making U.S. goods less expensive overseas.

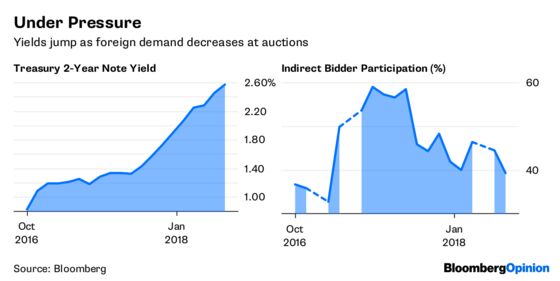

But someone needs to explain to Trump that at this point in time, the upside to a stronger dollar outweighs the downside. Consider that foreign investors own about half the U.S. debt outstanding. In effect, those investors are lending to the U.S. so the government can finance the budget deficit. That's not insignificant. The recent lost revenue from tax reform means the Treasury Department will need to more than double debt sales this year to $1 trillion to make up for the shortfall. Foreign investors would be more likely to buy U.S. debt if they were confident that the White House really was in favor of a strong dollar, making their holdings more valuable over time. If they aren't, then they could back away from U.S. securities, potentially causing borrowing costs for the government, companies and consumers to rise. Some of those doubts were probably on display Tuesday at the Treasury's monthly auction of two-year notes. The amount sold – $33 billion– was the most for that maturity since 2013, while a class of bidders that includes foreign investors purchased just 39.3 percent of the offering, their smallest share since 2016. The rate on the notes was the highest since July 2008.

What makes the results all the more disappointing is the fact that U.S. yields are higher than can be found in just about any other major government bond market. That should be a major draw for international investors. For example, two-year notes yield 3.17 percentage points more than similar-maturity German bunds, the most since at least before 1990. The average over that time is about a quarter of a percent, showing just how much of a premium the U.S. is paying to borrow. The auctions continue Wednesday, with the Treasury selling $36 billion of five-year notes.

DOLLAR HEADWINDS

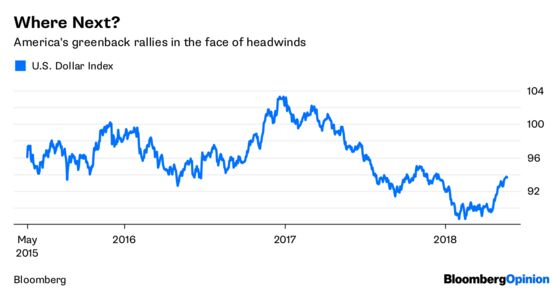

True, the dollar has rallied since mid-April, with the U.S. Dollar Index gaining 4.7 percent and rising to its highest level of the year, but few strategists are confident that this is the start of a lasting turnaround. Although the index has risen to 93.611, the median year-end estimate of strategists surveyed by Bloomberg is 90, which is lower than the 90.8 they had forecast at the start of 2018. Rather than any show of confidence in the U.S., some strategists say much of the dollar's gains stem from investors lightening up on highly profitable, near-record bearish bets, as well as companies repatriating overseas profits as a result of the recent tax reform. But that doesn't change the significant headwinds faced by the dollar in the form of the twin current-account and budget deficits. "There is no reason to expect" those deficits "to narrow anytime soon – in fact, (they are) going in the opposite direction," LPL Financial Chief Investment Strategist John Lynch wrote in a research note Tuesday. "While ongoing negotiations with China and on the North American Free Trade Agreement may eventually lead to some narrowing of the trade deficit, it will take years, not months." So although the dollar may continue its uptrend "in the near term," Lynch wrote that investors should "anticipate the return of the long-term secular downtrend as the greenback succumbs to the forces of the twin deficits."

COMMODITIES BREAK OUT

Or, maybe the reason for the softness in the bond market has more to do with the commodities, which are breaking out to the upside and fostering concerns that inflation is poised to accelerate. The Bloomberg Commodity Index jumped on Tuesday to its highest since 2015 and is poised for its best back-to-back months since March and April of 2016. The gains have been broad-based, spread between energy, metals and agricultural markets. Of 18 major commodities tracked by Bloomberg, only two – gold and soybeans – show a decline this month. While the rally is good news for commodities producers and investors, concerns are emerging that the rising prices of raw materials may be eating into corporate profit margins, damping the appeal of equities. We know what's been happening with oil and gasoline prices, but breakfast chain Cracker Barrel Old Country Store Inc. said Tuesday that it now expects commodity inflation of 3.25 percent for the fiscal year, compared to a previous estimate of as much as 3 percent. The price of lumber, a key material in the construction of houses, has jumped about 75 percent over the past 12 months. Bloomberg Intelligence equity strategists said they have reviewed transcripts of 350 first-quarter earnings calls by members of the S&P 500 and found that 38 percent mentioned that rising commodities prices are starting to put putting pressure on profit margins. "Margin expectations have been reduced on more than half of the industries in the index since the start of earnings season," BI strategists Peter Chung and Gina Martin Adams wrote in a research note Tuesday.

COMPLACENCY CREEPS BACK

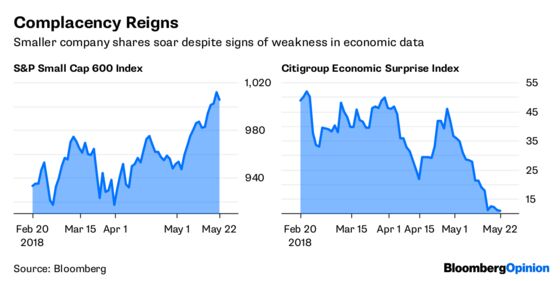

Remember how everyone described the big surge in the S&P 500 Index late last year and the first part of January as a "melt up"? That turned out to be an apt description, as stocks then cratered into a "correction" and have yet to recover. Well, there's another part of the stock market that looks to be in "melt up" mode, and some are wondering whether it, too, will come crashing down. The S&P SmallCap 600 Index has set eight new records this month. Its 8.14 percent gain in 2018 dwarfs the 2.27 percent increase in the S&P 500. That's a remarkable turnaround from last year, when the SmallCap Index – chock full of non-marquee names like Ollie's Bargain Outlet Holdings Inc. – lagged far behind the S&P 500, which is ruled by heavyweights including Apple Inc., Amazon.com Inc. and Google parent Alphabet Inc. Some see misplaced complacency in small caps, with implied volatility dropping to the lowest of the year, according to DataTrek Research. Small caps are largely a play on the domestic economy, which makes the current rally remarkable because the margin between the U.S. data that has been beating estimates and the data falling below estimates is the smallest since October, as measured by Citigroup Inc. If that trend continues, the momentum driving small caps could quickly disappear, just like it did for the S&P 500 at the end of January. "Stock prices always give the impression of certainty even though reality lives in a hazy cloud around them," Nicholas Colas, co-founder of DataTrek, wrote in a research note Tuesday. "Right now, that cloud seems small and unthreatening, just as it did in 2017. There are plenty of reasons, from Fed policy to oil prices, midterm elections to lingering trade negotiations, to think it will grow once again."

TOO CHEAP TO IGNORE

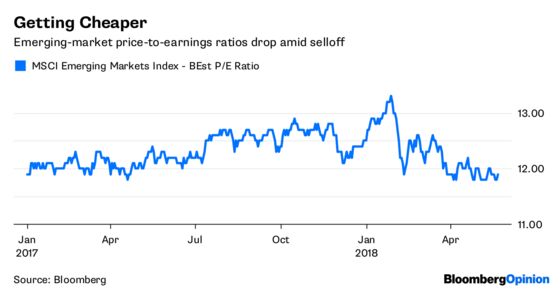

The rout in emerging markets took a breather on Tuesday, with an MSCI index of currencies of developing economies soaring the most in four months after dropping to its lowest level of the year on Monday. The rally was led by currencies from Latin America, specifically the Chilean peso, Brazilian real and Colombian peso. A growing number of influential investors say the sell-off that began in early April was too broad, capturing too many currencies of healthy economies with strong prospects at the expense of a troubled few such as Turkey and Argentina. BlackRock Inc., Goldman Sachs Asset Management International and Payden & Rygel Investment Counsel say they’re betting on a rebound now that valuations have left some assets a lot cheaper than January, according to Bloomberg News' Aline Oyamada. The price-to-earnings ratio of the MSCI Emerging Markets index stands at 11.8, down from a high of 13.3. "This has become a pretty good buying opportunity," Kristin Ceva, a money manager who helps oversee about $9 billion at Payden & Rygel Investment Counsel in Los Angeles, told Bloomberg News. Local currency government bonds yield about 4.5 percentage points more than developed-market bonds, up from about 3.25 percentage points at the start of the year. "What we see is attractive real yields in the emerging markets, coupled with a good underlying fundamental growth,” Richard Lawrence, senior vice president for portfolio management at Brandywine Global Investment Management in Philadelphia, told Bloomberg News.

TEA LEAVES

When will the highest mortgage rates since 2011 begin to crimp the U.S. housing market? Investors and economists may start to get the answer to that question as soon as Wednesday. That's when the government releases data for new home sales in April. Although the median estimate of economists surveyed by Bloomberg is for sales to drop 2.2 percent from a month earlier to an annual rate of 679,000 homes, that's not far from the record of 711,000 homes record back in November and would mark an increase from the 590,000 homes sold in April 2017. Consumer confidence has traditionally been a bigger factor in housing sales than mortgage rates, and it's important to know that sentiment has been at an all-time high. That said, there are signs that consumers may be grappling with rising debt loads. Recent data from the New York Fed showed that the number of consumers inquiring about taking on more credit within six months fell 5.65 percent, the most since the height of the financial crisis at the start of 2009. The data also show that the share of auto loans more than 90 days late rose for a seventh straight quarter, to 4.3 percent in the first three months of 2018. That’s the highest since 2012.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.