For Stock Traders, the Number 16 Is Especially Sweet

(Bloomberg Opinion) -- The S&P 500 Index rallied Monday, but trying to assign logic to the move feels a bit like a fool's errand. When pressed for a reason, investors cited a de-escalation of trade tensions between the U.S. and China over the weekend, but that doesn't feel satisfying. After all, the Trump administration only said the two nations agreed to “substantially” reduce the U.S. merchandise trade deficit with China. Beijing, meanwhile, promised to “significantly” increase purchases of U.S. goods and services.

The problem is, nobody can quantify "substantially" or "significantly," because neither side attached numbers to their statements. Nevertheless, there is a number that investors can work from: 16.

Ever since the big drop in late January and early February, the S&P 500 has been stuck in a trading range of between 16 and 18 times forward 12-month earnings estimates, according to Morgan Stanley Chief U.S. Equity Strategist Michael Wilson. The market has tested the bottom of that range four times since the selloff without falling further, Wilson noted in a research note Sunday. The good news is that the range has been rising given the increase in earnings estimates, implying a floor for the S&P 500 of 2,625 and a ceiling of about 2,950 based on current earnings estimates. On Monday, the index closed at 2,733.01.

Given this pattern, it makes sense to buy stocks whenever the forward price-to-earnings ratio drops toward 16 – unless one of two things happens, according to Morgan Stanley. One would be if 10-year Treasury yields move above 3.25 percent (they were at about 3.06 percent Monday); the other would be if there's a shock to the economy or earnings that causes investors to reassess equity risk premiums.

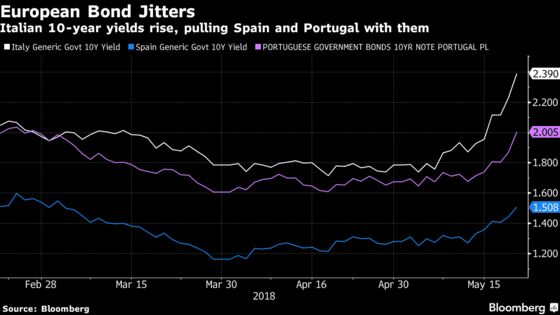

ITALY’S SICKNESS MAY BE CONTAGIOUS

The turmoil in Italian markets looks like it may be starting to spread to some of the euro zone's weaker members. Yields on 10-year Italian government bonds jumped 16 basis points to 2.39 percent on Monday, bringing the increase this month to 60 basis points, or 0.6 percentage point. Yields on Spanish and Portuguese bonds also soared. Investors may be worried that a proposal by the Five Star and League political parties to assess the feasibility of paying state debts with short-dated notes of small denominations known as mini-BOTs could catch on elsewhere. "Investors can handle idiosyncratic risk from Italy, but the threat of new systemic risks may weigh on the euro" and bolster currencies such as the Swiss franc, Danish krone and those of the Nordic region, the currency strategists at Brown Brothers Harriman wrote in a research note Monday. "The fear is that these Treasury bills will become a stealth parallel currency." The demand for derivatives that protect against a slide in the euro has risen to levels last seen during February’s stock rout, according to Vassilis Karamanis, a currency and rates strategist who writes for Bloomberg. "The use of the paper for payments of government liabilities could fuel concerns about Italy’s fiscal sustainability and even the country's membership in the euro zone,” said Valentin Marinov, Credit Agricole's head of G-10 currency research.

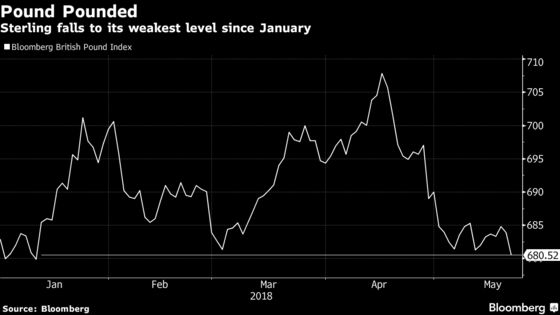

WHAT'S AILING THE POUND?

On April 16, the Bloomberg Pound Index closed at its highest since the U.K. voted to leave the European Union amid optimism that the economy was picking up and the Bank of England was poised to raise interest rates twice this year. But since then, sterling has faded fast, with the Bloomberg Pound Index losing almost 4 percent and falling Monday to its lowest since mid-January. It would be easy to attribute the pound's weakness to the dollar's renewed strength, but that would be ignoring the fact that the U.K.'s economy has turned softer of late. The Bank of England decided against boosting rates at its policy meeting May 10, and a widely expected increase in August could be in jeopardy if the economy doesn't rebound from a disappointing first quarter. The pound is also getting hammered by a new round of political uncertainty. Reports over the weekend said some lawmakers in the ruling Conservative Party are preparing for a snap general election later this year due to Brexit splits. The strategists at Credit Suisse wrote in a research note Monday that they are confident the pound will rebound and that it's "still a buy on dips given the positive political cycle (from low expectations) ahead of Brexit and muted rate-hike pricing."

PRAY FOR TURKEY

You know things are bad in markets when analysts say the only fix may be divine intervention. Istanbul-based broker Alnus Yatirim wrapped up his morning research note to clients Monday by writing “God help Turkey” as the nation's currency, stocks and bonds show no signs of bottoming amid double-digit rates of inflation. The mess Turkey is in is best illustrated in the performance of the lira, which weakened to a new low of about 4.60 to the dollar on Monday from about 3.40 in September. That represents about a 25 percent decline in the value of the currency. The Borsa Istanbul 100 Index has dropped 13 percent this year, compared with the decline of just 1.54 percent for the broader MSCI Emerging Markets Index. While Turkey's troubles are of its own making, they are symbolic of the broad weakness in emerging markets of late. From Mexico to Poland, and South Africa to Indonesia, it's hard to find an emerging market that hasn't taken a hit in recent weeks as interest rates in the U.S. rise, sparking a rebound in the dollar from a prolonged period of weakness. "When you look at external debt to GDP pre-crisis 2007, it was 28 percent. Now it’s 39 percent" for EM countries, Bob Michele, JPMorgan Asset Management’s global chief investment officer and head of global fixed income, said Monday on Bloomberg TV. "These economies have levered up and it’s not clear they can absorb higher funding rates going forward."

FUNDS MISS OUT ON OIL'S GAINS

Anyone with an automobile knows that the price of gasoline has shot higher in recent weeks. The Automobile Association of America says the national unleaded average gasoline price rose to $2.927 per gallon on Sunday, a 6.1 percent over the last month. A lot of that is due to the surge in oil, with Brent crude reaching $80 a barrel for the first time since 2014. There's no shortage of analysts who worry that rising oil and gasoline prices will curb consumer spending and economic growth. If so, then they should be even more worried about where the market thinks oil is headed. The five-year Brent forward price, which has been largely anchored in a tight $55-to-$60 a barrel range for the past year and a half, has jumped over the last month, outpacing the gains in spot prices and closing at $63.50 on Friday, according to Bloomberg News. "It seems that the investor community is finally calling into question the ‘lower for longer’ thesis" for oil, Yasser Elguindi, a market strategist at Energy Aspects, told Bloomberg News. There are also plenty of investors who are dismayed by the jump in oil prices because they haven't been able to take full advantage of the rally. Commodity Futures Trading Commission data show that hedge funds and other large speculators cut their net-long positions – the difference between bets on a price increase and wagers on a drop – for a fifth consecutive week, the longest stretch of declines since November 2016, according to Bloomberg News' Jessica Summers.

TEA LEAVES

The U.S. Treasury is dumping $276 billion of bills and notes on investors this week to pay for a ballooning federal budget deficit. The auctions will be closely watched for signs that investors believe the recent slump in Treasuries is overdone or whether there is more to come. The auctions started off fine, with the government having little trouble selling $90 billion of three- and six-month bills Monday. Things will heat up Tuesday, when it auctions $33 billion of two-year notes, the most for that maturity since 2013. Short-term debt has been particularly hard hit: With the Federal Reserve raising interest rates, yields on two-year notes climbed to a recent 2.57 percent from about 1.25 percent in early September. The strategists at bond powerhouse Pacific Investment Management Co. note that short-term debt securities have a lot of appealing attributes now that their yields have moved back above stock-dividend yields. "The front end of the fixed income markets looks attractive for the first time in almost a decade," the strategist wrote in a research report dated Monday.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.