(Bloomberg View) -- Bond lies.

In opaque and illiquid bond markets, if you think that you are getting ripped off by your trader or salesperson, the traditional thing to do is to go complain to her boss. "I do a lot of business with this bank," you say, "and if I find out that your salesperson is lying to me about the markup she is taking, I will put you in the penalty box." And then the boss takes the salesperson aside and says, look, obviously we want to make money, but you are squeezing this client a little too hard, maybe dial it back a bit. And the system works because the customers are sophisticated and can figure out when they are getting ripped off, and because the bosses know that they are sophisticated and so keep a lid on the ripoffs.

Or this is the rough theory, I don't know, but here is an anecdote about Benjamin Solomon, the former head trader of Deutsche Bank Securities Inc.'s commercial mortgage-backed securities desk:

The following month, on February 29, 2012, Solomon again covered for the misstatements of Trader C and Salesperson Y. Before offering a bond to a customer, Trader C had sold a different piece of the same bond to another customer at a price of 63. In offering bonds to the subsequent customer, Trader C and Salesperson Y wanted to avoid telling that customer the price at which they recently sold the same bond. After coordinating with Trader C, Salesperson Y told the customer that the sale was “a little higher” than 63 but would not provide the exact price. The customer then contacted Solomon, who called Salesperson Y about the issue. Although Solomon told Salesperson Y that the customer, who traded with DBSI frequently, deserved better treatment, Solomon agreed to tell the customer that the bond had last traded at 63.25. The customer bought the bonds at that price. DBSI made approximately $18,750 on the trade attributable to the misstatement

The system almost worked! A little? Like, the customer kind of sensed that his Deutsche Bank team was lying to him, and he called the boss to complain, and the boss kind of did tell the team to knock it off? But after one last score? (For $18,750?) In a repeat game you can view this as a sort of rough justice: Deutsche Bank was lying to the customer a little bit too much, and the customer complained, and Deutsche Bank grudgingly agreed that, going forward, it would lie a little bit less. A market that works on this basis can ... work. But you can see why regulators might come in and ask for something a bit better.

Of course that anecdote is from a Securities and Exchange Commission enforcement order against Deutsche Bank and Solomon, who "consented to the SEC’s order without admitting or denying the findings." Deutsche Bank will pay back "more than $3.7 million" to customers who got ripped off, as well as a $750,000 penalty; Solomon will pay $165,000 and be suspended from the industry for a year. If you want dumb trader chats, here are some more of them:

In another transaction, on September 27, 2011, Trader B bought a bond for DBSI’s account at a 735 spread. Later that day, Salesperson X offered the bonds to a customer but falsely stated that he was intermediating the trade with another customer who held the bond. After some negotiation with the customer, Salesperson X consulted with Trader B, who instructed him to tell the customer that “the account is being sticky at [715] ” i.e., that the fictitious other customer refuses to move from its 715 offer. Trader B then acknowledged to Salesperson X, “This is just a lie, right?” Salesperson X replied, “Well, I don’t care.” Trader B then said, “But I think we should say that.” Salesperson X agreed and then conveyed that misstatement to the customer, who then bought the bond at 714 and, incorrectly believing that DBSI obtained the bond at 715, paid an additional basis point on top as compensation to DBSI.

And:

In one instance, on January 17, 2012, Solomon bought a bond for DBSI’s account at 58. Shortly thereafter, Trader C offered the bond to a customer at 58.75. The customer responded, “58.25 ur working for too much. be nice.” Trader C replied “I bought them at 58.5.” Having been misled by Trader C, the customer accepted the offer. Solomon, aware of the spread between the purchase and sale prices, called Salesperson Y to warn him “not that you would, but, uh, [the buyer] thinks we’re just working for a quarter point on those bonds, ok?” Salesperson Y responded “I would never ... We need to make money. You deserve to make money, and I deserve to get paid.”

This is of course a sequel to the case of Jesse Litvak, the former Jefferies LLC trader who was sentenced to two years in prison for doing the same sort of stuff that Traders B and C and Salespeople X and Y got up to at Deutsche Bank. Those people didn't even get named in the SEC order, never mind thrown in prison. (Deutsche Bank said that it "took appropriate disciplinary action, including termination in some instances," so perhaps they were fired.)

One problem with regulation by enforcement is that it leads to pretty disparate punishments for the same action: For years bond traders lied to customers about the prices they had paid, and the enforcement mechanism was basically the customers calling up the traders' bosses to complain. And then prosecutors and regulators decided that it wouldn't be allowed any more, and it felt a bit silly to write a new rule saying "don't lie to customers about the prices you paid for bonds," and so instead they found an example in Litvak and put him in prison. That sent an effective message, and now one hopes that bond traders aren't doing much of this any more. But plenty of them did it back in the old days, and the regulators need to do something about it, but on the other hand they don't need to put all of those people in prison. That would be wasteful; imprisoning Litvak is plenty to send the message. So everyone else just gets relatively light punishments. As a regulatory method it more or less works, but it is rough on the one guy chosen to send the message.

Are banks opaque?

Here is a pleasing Bank for International Settlements working paper by Fabrizio Spargoli and Christian Upper looking into bank opacity. "Conventional wisdom maintains there are severe information asymmetries between a bank’s management and outside investors," they begin, and then they check to see if that is true by looking into whether bank executives are any better at trading their own stock than anyone else. The answer is meh, not really:

On average, bank insider sales do not earn an abnormal return and do not predict stock returns. By contrast, bank insider purchases do, even though less than other firms. Our within-banking sector and over-time analyses also fail to provide evidence of greater opacity of banks vis-à-vis other firms.

One possible explanation of this result is that banks provide investors with all of the information they need to fully understand their businesses. (Banks are not opaque.) Another possible explanation is that banks' disclosure is bad, but no worse than anyone else's. (Banks are opaque but so is everyone.) A third possible explanation is that disclosed trading by officers and directors, especially at highly regulated banks, is never done with an information advantage, because the only time you feel safe trading is when you don't know any more than the market does, and you use a 10b5-1 plan to avoid making informed trades. (Banks are opaque but not in a way that can be measured by insider trading.)

A fourth explanation, one which I kind of like, is that banks are impossible for outside investors to understand, but they are equally impossible for well-informed executives and directors to understand. The insiders have more data, and perhaps even more understanding of how the business works, but no more understanding of what will happen tomorrow than anyone else has. In this view, banks are radically opaque: Not only can you not see into them from the outside, but even when you get inside and look around, you still can't see anything. Jayanth Varma writes:

Banks are so opaque that even insiders cannot see through the opacity when bad things happen. Sometimes, as in the case of the London Whale, a market participant outside the bank has greater visibility to what is going on.

Elsewhere in bank mysteries:

- "German officials acknowledge in private that they would be tempted to skirt European rules if one of the country’s top banks needed a bailout." I ... what? This is not how to do it. If one of your country's top banks needs a bailout, sure, whatever, ignore the rules, bail it out, I am fine with that. Of course there is a moral-hazard cost if you do the bailout, but it might be outweighed by the benefits of saving your banking system and economy. But before that, when no one needs a bailout, don't go around saying -- even "in private" -- that you'd totally do a bailout if it ever became necessary. That's all moral hazard with no benefit!

- "Does More 'Skin in the Game' Mitigate Bank Risk-Taking?," asks the New York Fed's Liberty Street Economics blog.

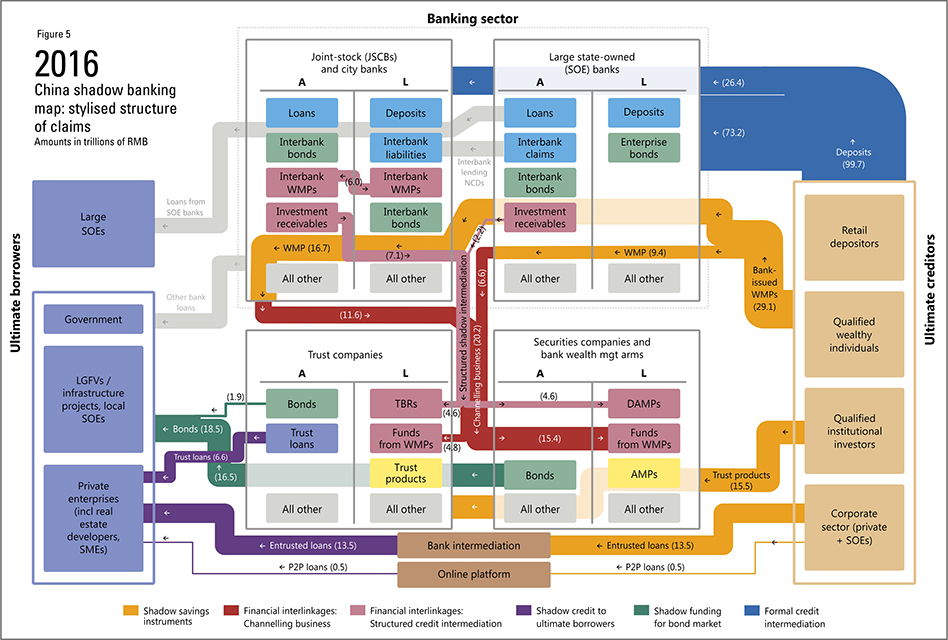

- Here's a BIS working paper on "Mapping shadow banking in China: structure and dynamics," and the actual map is pretty cool.

{kind=link}

Point72.

Lauren Bonner runs the talent analytics team at Point72 Asset Management, Steve Cohen's family office and once and future hedge fund, and yesterday she filed a lawsuit accusing Point72 of hostility to and discrimination against women. The complaint includes a couple of allegations of gross openly sexist behavior, but that is not the main point. Instead, the way these things usually work is that the bulk of the complaint is spent arguing that women are not paid or promoted fairly at Point72.

Point72 "emphatically denies these allegations," and they can be hard to prove in court. There is rather striking statistical evidence -- "of the 125 Portfolio Managers that Point 72 employs, it is believed that all but one are men," says the complaint, and "of the thirty to thirty-two Managing Directors, only one is a woman" -- but the job functions and performance of hedge-fund employees, particularly non-investing employees like Bonner, are not necessarily easy to compare. Who is to say that she is more qualified than the men who get paid more than her?

Well! Here is how her complaint describes a male recruiting employee who was hired at a higher salary and title than Bonner:

P72 hired Shields from The Blackstone Group, where he worked on the multimanager fund Senfina Advisors LLC (“Senfina”).

Shields was responsible for hiring many of the individuals that were responsible for Senfina incurring double-digit losses in 2016.

Despite coming from a fund down 24 percent, P72 hired Shields as a Director and agreed to pay him $1.3 million, with the expectation that Shields would hire portfolio managers that could deliver large gains.

Another male comparison was hired "from Och-Ziff Capital Management Group LLC ('Och-Ziff'), a firm that was rocked by scandal surrounding a five-year bribery probe and which suffered massive withdrawals in 2016." It seems almost rude to remind people that their previous hedge-fund jobs involved large losses or withdrawals, and yet ... it does seem like sort of a fair way to value their experiences? All else being equal, recruiting managers who lose money is a less impressive experience than recruiting managers who make money.

Also, given the much-discussed statistics about the gender wage gap, it is a little awkward that the fund's name is a decimal fraction in the 70s. As guitarist and record producer Scott Lane pointed out:

Were you worried about 50 Cent?

An annoyingly pervasive story over the past year or so of low volatility has been that someone has been buying a lot of out-of-the-money call options on the CBOE Volatility Index that would pay off if the VIX spiked. This someone would usually buy the calls that traded at a price of around 50 cents, leading to the buyer being nicknamed "50 Cent," and many rap lyrics were awkwardly repurposed to discuss these VIX option trades. The story was always the same though: Vol was low, the options didn't pay off, and Mr. Cent seems to have been down about $200 million since 2017.

Well now he gon' ... party ... like ... it's ... his ... I will stop, I am sorry, but here:

But as volatility rose last week, and stock markets fell, the strategy paid off. According to Pravit Chintawongvanich, head of derivatives strategy at Macro Risk Advisors, 50 cent held a net profit of $200m on the trade as of February 9.

“That means they’ve made about $400 million mark-to-market this month,” said Mr Chintawongvanich.

Great, that's great, congratulations, let's move right along. Elsewhere in volatility:

- "Volatility Sellers Return to Market With a Vengeance";

- A Planet Money Indicator episode on the VIX; and

- "VIX Manipulation Costs Investors Billions, Whistle-Blower Says." Here is the anonymous whistleblower's letter, which I found a little incoherent; CBOE says that it "is replete with inaccurate statements, misconceptions and factual errors, including a fundamental misunderstanding of the relationship between the VIX Index, VIX futures and volatility."

Oh crypto.

There is no end to dizzying fractal dumbness in the crypto space. So for instance BitConnect was a "lending and exchange platform that was long suspected by many in the crypto community of being a Ponzi scheme" and that shut down in January. Some of the geniuses who gave BitConnect their money have a cunning plan to get it back. The cunning plan is of course a new cryptocurrency:

They decided to take justice into their own hands. They’re calling themselves Crypto Watchdogs, and while they’re being secretive about their identities, they’re offering a bounty for information on anyone involved with BitConnect. Eventually, they say, payment will be made in JusticeCoins, which they will mint.

Here I will just write the sequel for you. They will get some information, though not enough to actually get any money back from BitConnect. The people who give them the information will demand their JusticeCoins and not get them. They will start their own Crypto Watchdog Watchdogs group, and offer a bounty to unmask the Crypto Watchdogs, with payment to be made in ExtremeJusticeCoins. And then this process will repeat, until 99 percent of the market capitalization of all cryptocurrencies consists of bounties on anonymous cryptocurrency scammers. It makes a lot of sense. They are cryptocurrencies backed by grievance, an asset that is both inexhaustible and highly valued.

What else? "Arizona Senate Passes Bill To Allow Tax Payments In Bitcoin." There is a popular theory that fiat currency derives its value from the fact that you have to use it to pay taxes: There is nothing intrinsically valuable about the green pieces of paper that we call dollars, but if U.S. citizens always need dollars to pay their taxes, then there will always be demand for dollars. But if U.S. citizens don't need dollars for taxes, then ... maybe now is when Bitcoin will take over the world? Meh. The real news will be when states levy taxes denominated in Bitcoins.

And "Russian Scientists Arrested for Crypto Mining at Nuclear Lab." Sure that sounds bad! But the optimistic interpretation is, maybe it is better than whatever else they were getting up to? If Bitcoin mining diverts computing power that would otherwise be used for cancer research into pointless puzzle-solving, then that is bad. But if it diverts computing power that would otherwise be used for nuclear weapons, then maybe that's a good thing?

And "Bitcoin Industry Grapples With Age-Old Problem of Inheritance," though really the problem is not so much about inheritance as it is about people losing their, or their dead relatives', bitcoins.

And Yamana Gold Inc. did a blockchain thing:

Yamana, a global precious metals mining company, is the first to license Emergent's blockchain technology supply chain solution, which traces the provenance of Conflict-Free Gold from mines to refineries, and through to vaults. The solution uses blockchain technology to administer smart contracts among the parties involved in the delivery of gold-bearing material, including miners, refineries, logistics providers and insurance companies.

The stock was up only 6 percent, perhaps because the word "blockchain" doesn't appear until the second paragraph.

Things happen.

The Tax Law Is About to Make Analyzing Earnings Trickier. White House plans to scale back powers and budget of CFPB. No Quick End to Steve Wynn’s Legal Fight With Ex-Wife Over Stock. Good IBD associate goodbye email. Bannon Wanted Yellen to Stay Fed Chair, Calling Her ‘My Girl.’ Wall Street trading desks get fillip from return of volatility. Retail Investors Piled In Just Before the Stock Rally Fizzled. Citi, Goldman Plan ETFs Tied to Riskiest Bank Bonds. Sky-High Salaries Are the Weapons in the AI Talent War. Self-Driving Cars Will Kill Things You Love (And a Few You Hate). Sony Apologizes After ‘Peter Rabbit’ Movie Exploits a Food Allergy, Upsetting Parents. Furby organ.

If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Thanks!

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matt Levine is a Bloomberg View columnist. He was an editor of Dealbreaker, an investment banker at Goldman Sachs, a mergers and acquisitions lawyer at Wachtell, Lipton, Rosen & Katz and a clerk for the U.S. Court of Appeals for the Third Circuit.

To contact the author of this story: Matt Levine at mlevine51@bloomberg.net.

To contact the editor responsible for this story: James Greiff at jgreiff@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.

©2018 Bloomberg L.P.