Rule-Based Monetary Policies Will Keep Volatility Low

(Bloomberg View) -- The global economy is enjoying its first synchronized upswing since 2007. As a result, more central banks are looking to retreat from quantitative easing and other unconventional monetary policies implemented in the wake of the worst financial crisis since the Great Depression. The latest example is the European Central Bank, which will likely announce on Thursday that it will cut its monthly bond purchases by as much as half to 30 billion euros ($35.3 billion).

The ECB follows the Federal Reserve, which this month started to shrink its $4.5 trillion balance sheet by reinvesting fewer proceeds from the bonds that it holds back into the market. Despite these moves, measures of volatility have stayed low, and will likely remain so as this transition unfolds. That's not the conventional wisdom, but it makes sense when you think about how these new policies are being communicated and implemented. In other words, central banks are moving toward a rules-based playbook, and when policies are guided by rules there tend to be fewer surprises. And when policies are predictable, volatility drops and financial conditions become easier.

A clear example is the Fed’s balance sheet normalization principles published in June. Markets know exactly what to expect from the Fed over the next couple of years when it comes to unwinding the balance sheet. Beyond QE measures, other central banks, including the Bank of Canada, are relying less on so-called forward guidance to determine the level of interest rates and more on actual data. When economies are stable and growing, prescriptive policy rules such as those suggested by Stanford University economist John Taylor, who is on President Donald Trump’s shortlist to lead the Fed, could work to foster growth because monetary policy becomes predictable. When economies weaken, however, policies that are too predictable could have an adverse impact.

Markets are already reacting to the Fed's move toward a more rules-based policy, as seen in the large gap between declining volatility and easier financial conditions. The flip side is that concerns about investor complacency may only deepen under rules-based central bank policies as volatility stays low, leverage increases and financial conditions loosen to potentially extreme levels. In the past, such super loose conditions eventually led to quicker monetary policy tightening that slowed the economy.

Volatility and Financial Conditions

Predictable monetary policies also have implications for the yield curves. In 2005, when the Fed was in the midst of raising rates from 1 percent to 5.25 percent in increments of 25 basis points, then-Governor Ben S. Bernanke noted the increasing flatness of the yield curve was causing financial conditions to loosen despite the central bank's efforts to tighten monetary policy.

A similar situation exists today, with the relatively flat yield curve keeping financial conditions loose. But that has created a sort of dichotomy in markets. On one hand, the economy is doing well as reflected in rising stock indexes and looser financial conditions. But the flattening of the yield curve also has historically foreshadowed a slowdown in the economy.

Yield Curve Slope and Financial Conditions

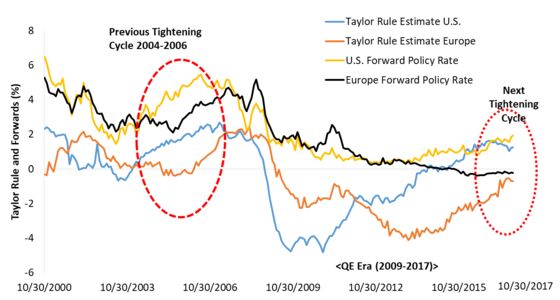

Although markets have responded positively to what they see as predictable monetary policy, that could change if rule-based policies result in too much tightening. The risk is that the more predictable monetary policy becomes, the greater the likelihood of another financial crisis like the one a decade ago. No policy rule can easily resolve such a crisis.

Taylor Rules and Market Expectations

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ben Emons is chief economist and head of credit portfolio management at Intellectus Partners LLC. The opinions expressed are his own.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.

©2017 Bloomberg L.P.