Fed Leadership Changes May Bring a GDP-Focused Agenda

(Bloomberg View) -- Federal Reserve Vice Chair Stanley Fischer’s decision to resign in October with nine months remaining on his term could mean the potential is high for central-bank policy to be reshaped much sooner than many investors expected. Fischer’s departure will leave four of the seven seats on the Fed Board of Governors vacant, and that doesn’t include the one held by Chair Janet Yellen, whose term expires in February.

Given the list of names being floated as possible replacements for Yellen, which includes candidates with commercial banking backgrounds and economists whose academic work embodies policy rules and tax issues, it’s not hard to imagine that new leadership at the Fed could start to focus on nominal gross domestic product targets instead of full employment and inflation. That’s something the Trump administration has suggested would be desirable.

The question is, how would policy have to change under a regime that targets GDP? First, the Fed would have to address remittances to the Treasury Department and the interest it pays to banks on excess reserves. The Fed currently transfers the interest income from the government securities it has purchased through open market operations to the Treasury. Those remittances are sizable, and are equivalent to more than 20 percent of the government’s corporate tax receipts. Interest on excess reserves amounts to more than 1 percent of total bank assets in the U.S. (see Fig. 1). Given that more than $2.1 trillion of reserves sit idle at the Fed, there is a lot of political appetite to get that money cycled back into the economy.

Ideas proposed by former Fed Chairman Ben Bernanke may also help to shape a new balance-sheet policy. Bernanke suggested that the Fed credit the Treasury’s account at the central bank with reserves instead of remitting it back the interest the central bank receives from its bond holdings. In return, the Treasury would pledge Treasury bills as collateral, allowing it to spend the reserves any way it sees fit. The Fed and Treasury could strike a new “accord” whereby reserves from the banking system fund public-private partnerships for infrastructure spending. With tax reform and deregulation, a business-friendly environment could generate the needed investment and boost productivity.

Fig. 1: Federal Reserve Remittances and Interest on Excess Reserves

(Source: Bureau of Economic Analysis, NIPA Table 3.2. St. Louis FRED research.)

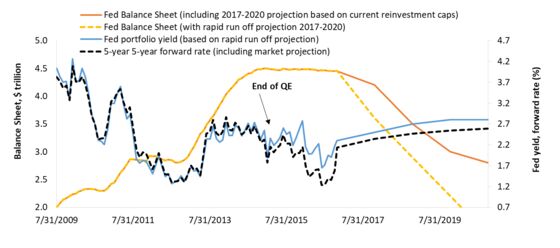

Of course, there is no such thing as a free lunch. To get the ideal mix of public and private partnerships, the economy and markets have to cooperate. Redirecting reserves from the banking system to the Treasury would negate the need for an increase in the issuance of Treasury securities. Less supply would temper any rise in long-term borrowing rates, offering the Fed more flexibility to shrink its $4.5 trillion balance sheet at a faster pace (see Fig. 2).

Bond markets would not necessarily be averse to that scenario. The duration risk -- or sensitivity to higher rates -- of the Fed’s balance sheet has fallen since quantitative easing ended in 2014, and the yield of the Fed’s portfolio and market forward rates have decoupled (see Fig. 2). This development comes after the Fed reinvested proceeds from maturing debt across the yield curve rather than solely in longer-term debt, while actual bond yields fell. Based on a rapid run-off scenario (the dotted line in Fig. 2), the yield of the Fed’s portfolio would only marginally rise above the current five-year rate traded five years forward. This suggests that at least for the time being the forward yield curve has priced in little risk from a change in the Fed’s balance sheet.

Fig. 2: Fed Balance Sheet and Interest Rates

(Source: Bloomberg, New York Federal Reserve. Fed portfolio yield is the duration weighted average of the yields of Treasuries held in the portfolio. Fed’s portfolio yield rises as the % weight of long-maturity bonds increases relative to shorter-maturity bonds as those run off faster than current projections based on reinvestment caps.)

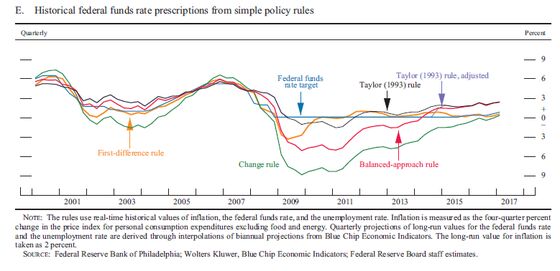

Much depends on what the Fed decides to do with the federal funds rate. In that respect, the Monetary Policy Report from July 2017 showed the Fed’s current “balanced approach” to policy (the red line in Fig. 3) is not much different from the “Taylor rule,” originated by economist John Taylor in 1993. The rule describes how the Fed would adjust the federal funds rate to changes in inflation, employment and output. Taylor was one of those mentioned on the list of six candidates to replace Yellen as Fed chair. If Taylor were to be appointed by the Trump administration, he may find there is not much to change to policy because it has been following the Taylor rule as shown in Fig. 3.

Fig. 3: Fed July Monetary Policy Report on Policy Rules

(Source: Federal Reserve Monetary Policy Report, July 2017.)

Markets have thus far not read much into Fischer’s sudden departure other than pricing in a reduced chance of another rate increase before year-end because of the uncertain impact on the economy from hurricanes Harvey and Irma and the new debt ceiling deadline in December. The Fed has ample time to drive expectations of a hike to a 100 percent probability, especially when a pro-growth agenda begins to shape policy framework. Changes at the Fed are on the horizon, and they may be bigger than the market currently discounts.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Ben Emons is chief economist and head of credit portfolio management at Intellectus Partners LLC. The opinions expressed are his own.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.