The ‘All Clear’ Memo Didn’t Reach Emerging Markets

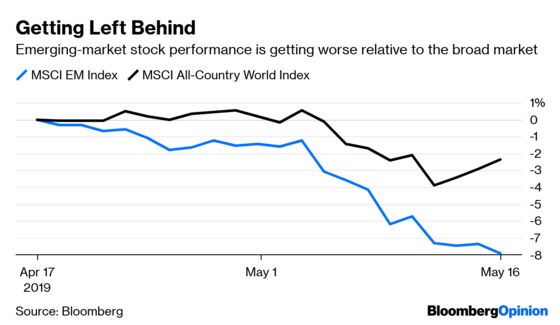

(Bloomberg Opinion) -- Regulatory filings show that hedge funds in the first quarter more than doubled their investments in the three largest exchange-traded funds that buy stocks in emerging markets. Too bad. On Thursday, the MSCI EM Index fell to its lowest since mid-January even as the broader MSCI All-Country World Index surged the most since the start of April.

There are some valid explanations for the underperformance, namely the renewed strength in the dollar and gains in oil, both of which are seen as a drag on emerging-market economies. Even so, it’s still a bit shocking to see emerging-market assets post an outright decline when the broader market is enjoying a strong rally. And this isn’t a one-time phenomenon. The MSCI EM Index has severely underperformed the broader market since mid-April, declining almost 8% despite a dovish Federal Reserve. As a general barometer of risk sentiment, this should be concerning to anyone betting that the escalating trade war between the U.S. and China will be resolved in short order and the fallout contained. “Even if these trade tensions are solved for now, I think in the future there will be further escalations,” Jim O’Neill, the former Goldman Sachs Group Inc. chief economist and coiner of the BRIC acronym, told Bloomberg News. “Economics can be criticized for a lot of things, but one essential core aspect of international economic theory is that trade is in aggregate a win-win and less trade is a lose-lose.”

There may also be something structural to account for the poor performance of emerging markets. The Institute of International Finance in Washington said Thursday that a measure of what it calls “true” foreign direct flows to emerging markets — because it excludes reinvested earnings — has fallen to the lowest in 20 years. Low Group of 3 “interest rates pushed a ‘Wall of Money’ to EM over the last decade, so that there is now a positioning overhang” that needs rebalancing, the organization said in a report.

MASTERS OF THE OBVIOUS

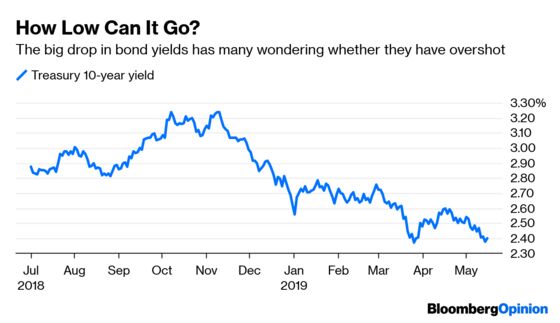

To say the rally in bonds this year is surprising would be an understatement. Yields on 10-year Treasuries dropped as low as 2.35% on Thursday from 3.25% in November. To put that in context, the median estimate of more than 50 economists and strategists surveyed by Bloomberg in December forecast the yield would be somewhere between 3.20% and 3.27% by now. But even with the escalation of the U.S-China trade war expected to lead to a slower economy and the Fed’s dovish pivot, there’s a sense that the bond market has gone too far. “In the short term, while you have these tensions and this uncertainty, of course you could potentially see yields grind lower,” James Ashley, the head of international market strategy at Goldman Sachs Asset Management International, told Bloomberg TV on Thursday. “But by the end of the year, something closer to 2.7%-ish is somewhere where we would be expecting the U.S. 10-year.” But the case could be made that bonds may even be cheap. As Medley Global Macro Managing Director Ben Emons put in a note Thursday, yields reflect expected growth and inflation plus a premium to account for the time to maturity. On that basis, “fair value” for 10-year yields is about 2.15%, Emons wrote.

SEEKING PROTECTION

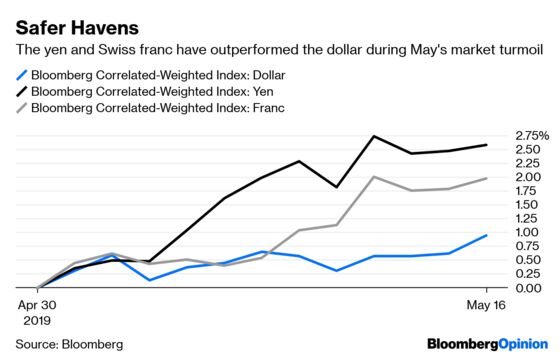

The Bloomberg Dollar Spot Index rose for the third time in four days Thursday, putting the greenback near its strongest levels since December. Much like with the rally in bonds, this move higher is most likely less a referendum on the U.S. and more likely the result of investors seeking a haven from a slowing global economy, an intensifying trade war and rising tensions in the Middle East. As evidence, the dollar has appreciated even though the Federal Reserve Bank of Atlanta’s GDPNow index, which attempts to track the economic growth in real time, has slid to 1.165% from as high as 2.789% in mid-April. But those investors looking to do a little de-risking would do better to hide out in the yen and Swiss franc even though the Bank of Japan and Swiss National Bank may take verbal action to prevent their currencies from rapid appreciation, Morgan Stanley’s currency strategists wrote in a report Thursday. Indeed, the yen has gained 2.54% this month against a basket of nine developed-market peers, while the franc has strengthened 1.96%, compared with a 0.95% gain in the dollar.

ETERNAL OPTIMISTS

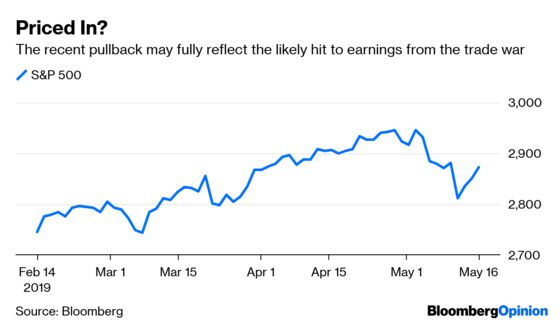

The S&P 500 Index rose for a third consecutive day on Thursday. At one point, it was 2.86% during the period for its best three-day gain since early January. Does that mean the escalating trade war between the U.S. and China is little more than a tempest in a teapot? Of course not, but nobody seems to know how this will all play out. As Medley’s Emons also points out, the options market shows there’s been a large increase in open interest on contracts with strike prices both 10% above and below the S&P 500’s current level. But that activity hasn’t been symmetrical, with the open interest in contracts that would pay off if the benchmark rose 10% almost four times as large as the open interest in contracts that would profit if it fell 10%. If anything, that goes to show that equity investors are eternal optimists. The equity strategists with Bloomberg Intelligence figure that the worst case from a trade war i s probably priced into stocks. According to them, if the U.S.-China rift escalates to include all trade between the two nations, the downside would represent about a 50 basis-point reduction in gross profit margins and a 3% hit to earnings before interest and taxes— a scenario that the 3.5% decline in stocks from the recent highs appears to assume. For those wondering what that would mean for the bottom line, 2019 profits in aggregate for members of the S&P 500 would be reduced by $129 billion to $4.66 trillion.

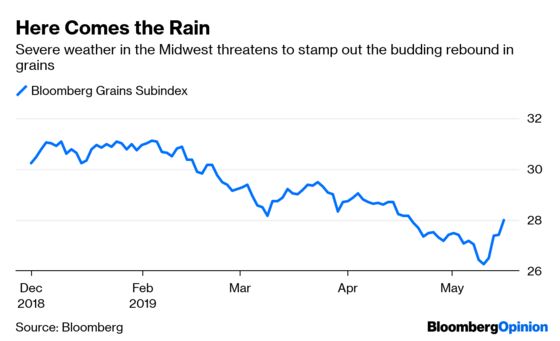

THE GRAIN OUTLOOK IS STORMY

In the commodities market, grains are having a moment. The Bloomberg Grains Subindex has risen for four consecutive days, gaining 6.67%. Impressive, but little solace to long-suffering commodities bulls who are still down 7.42% for the year in grains and haven’t seen a winning year since 2012. And there’s no reason to think that this recent rebound is the start of a turnaround. That’s because any hopes of getting corn and soybean planting back on track in the U.S. may be washed away starting Friday as a pair of storms threatens to deliver a “one-two punch” of soaking rain and tornadoes across the Great Plains and Midwest through next week, according to Bloomberg News’s Brian K. Sullivan. As much as 3 to 5 inches (8 to 13 centimeters) of rain will soak soils from South Dakota and Minnesota south to Texas, Oklahoma and Arkansas, according to the U.S. Weather Prediction Center in College Park, Maryland. Widespread severe thunderstorms that can spark tornadoes are also expected across the region from Friday through May 21, Sullivan reports. Floods and rains have mired planting progress across the Great Plains, Mississippi Delta and Midwest for months with corn, soybeans, cotton and rice all lagging behind the five-year average through May 12, according to the U.S. Department of Agriculture weekly crop progress report released Monday.

TEA LEAVES

U.S. consumer confidence took a big hit in January, with the University of Michigan’s preliminary January sentiment index dropping to its lowest since October 2016. The government shutdown was blamed for the decline, but the steep drop in the stock market at the end of 2018 also likely played a role. After the big decline in stocks to start this month, will there be a repeat when the sentiment index for May is released Friday? Economists don’t think so, with the median estimate of those surveyed by Bloomberg calling for little change, forecasting a reading of 97.1 compared with 97.2 in April. Nevertheless, don’t sound too confident in their estimates. “Consumer sentiment could get a modest dent from the latest stock market swoon driven by the trade-war tensions and the increase in tariffs,” the team at Bloomberg Economics wrote in a research note. “While modest, the latest slide in stock prices will serve as a painful reminder of the year-end market rout, which not only moved consumer sentiment lower in January — 7.1 index point decline— but also affected growth in consumer spending.”

DON’T MISS

Pick a Stagnant Economy or More Globalization: Noah Smith

The Disconnect Underlying This Economic Miracle: Daniel Moss

Looking for a Trade War Winner? There Aren’t Any: Shuli Ren

Trump Still Has Germany and the EU in His Sights: Lionel Laurent

Getting Rich by Investing in Art Is So Easy: Barry Ritholtz

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.