There's a Lot of Gasoline, But Not Enough for Trump

(Bloomberg Opinion) -- Some good news for President Donald Trump ahead of the midterm elections: There is plenty of gasoline sitting around. Some bad news: Average pump prices are still almost $3 a gallon. Some worse news: Pump prices have more to do with Middle East intrigue than Midwest inventory.

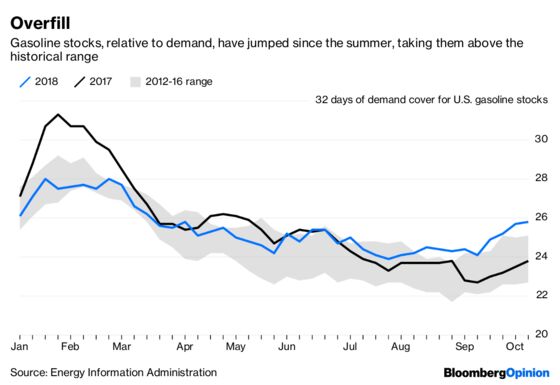

Gasoline inventories have, unusually, been rising since the end of July. They now cover almost 26 days of U.S. demand, according to the Energy Information Administration, significantly higher than a year ago and even above the the top end of the range for this time of year:

Even so, pump prices have kept rising.

Refiners aren’t getting the benefit. The spread between West Texas Intermediate crude oil and gasoline futures – a proxy for refining margins – has collapsed. It went below $10 a barrel this week for the first time since November 2016.

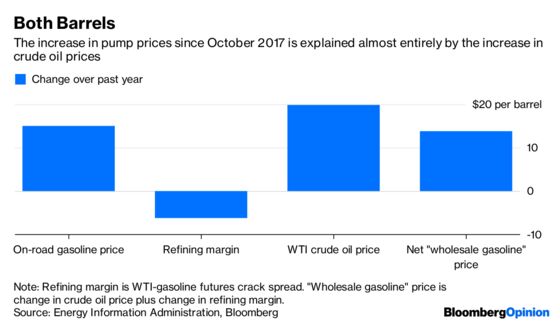

Spreads tend to drop away after the summer. But a year-over-year comparison shows just how much margins on gasoline have weakened. The average on-the-road gasoline price has risen by about 36 cents per gallon over the past year, or almost $15 a barrel. Yet the refining margin has actually dropped by $6 and change. The culprit is crude oil, up almost $20, meaning a change in the implied “net wholesale” price of gasoline of about $13.75 – or more than 90 percent of that increase at the pump.

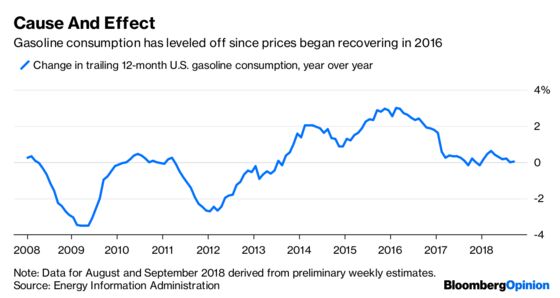

Refineries ran very hard over the summer, though largely chasing margins on diesel, where demand is stronger and stocks are tighter. This, along with the lighter crude oil coming in from U.S. shale basins, boosted gasoline output. But with pump prices rising on the back of crude oil, demand hasn’t kept pace, flattening out over the past year or so after the robust growth spurred by oil’s fire sale in 2015 and 2016:

As refineries finally take some downtime for maintenance, gasoline inventories could follow, helping to stabilize margins (crude demand would also ease). The latest data, released Wednesday morning, showed a two million barrel drop in gasoline inventories last week. Weak demand, however, meant days of cover actually ticked up.

Looking ahead, much could depend on the weather. Colder temperatures would boost demand for distillate, perhaps pushing refineries to chase margins there and sending more gasoline into storage again.

Higher demand would cure all, of course, but that isn’t likely to happen unless prices fall. And the big factor there is geopolitics rather than anything being done in refineries. The diplomatic crisis sparked by the disappearance of journalist Jamal Khashoggi is the latest sign Saudi Arabia’s vaunted narrative of reform comes with a more familiar reactionary subplot.

Intertwined with this, of course, is Trump’s decision to withdraw from the U.S. nuclear agreement with Riyadh’s rival, Iran, and reimpose sanctions, tightening oil supply. That’s the real fuel on the fire when it comes to prices, and all that extra gasoline can’t douse it.

-- Gasoline stocks chart by Elaine He.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.