Biden Stocks Will Have History and Fed on Side, Not Much Else

Going by history, buoyant markets tend to stay that way after a presidential election, at least for a while.

(Bloomberg) -- First the good news for Joe Biden in the stock market. Going by history, buoyant markets tend to stay that way after a presidential election, at least for a while.

Data is positive for president-elects when it comes to momentum. Since 2000, every time the S&P 500 was higher heading into Election Day, November and December came in green, too. The first years of presidential terms have also been good ones of late. Since 1986, according to Leuthold Group data, they’ve seen average gains of 18.6%.

Equally reassuring, if you’re hoping for a Biden rally, is the steadfast presence of the Federal Reserve, which has been instrumental in preventing equities from collapsing and just reaffirmed it has no plans to turn off a money spigot that has been flowing all year. The possibility of a federal stimulus package for the economy also exists, though Democratic and Republican lawmakers reiterated opposing positions on Friday.

Now for the bad news. Standing against the cause of Biden in equity markets is a portfolio of trouble that has loomed for 10 months: the coronavirus and its attendant hardships, sky-high corporate valuations. Add to that political pressure to dismantle at least some of Donald Trump’s policies that helped keep markets aloft.

“It’s incrementally going to get tougher for Biden. He’s got bad fundamentals and expensive stocks. That’s a recipe for short-term disaster,” said Mike Bailey, director of research at FBB Capital Partners. “The stock market is going to be walking on eggshells waiting for Biden to drop the tax bomb at some point. It’s just going to be a very different type of dynamic.”

While a resurgent pandemic and high price-earnings multiples would create headaches for anyone regardless of party, it’s the more abstract issues that have given bulls pause when it comes to Biden. For months they’ve been struggling to figure out how seriously to take his frequent bashing of Trump’s equity obsession, which coincided with a 55% jump in the S&P 500 and the fourth-best return for a first-term president

Some of his utterances, while not exactly anti-market, have been ominous, if your worldview is dictated by equity prices. “Where I come from,” he said in the last debate, “people don’t live off of the stock market.” Criticizing Trump’s championing of the Dow Jones Industrial Average, he said: “That the stock market is booming is his only measure of what’s happening.”

While it’s possible to write off the talk as sloganeering, pressure exists within the Democratic party to translate it into action, particularly when it comes to tax policy. According to Kamala Harris, a Biden administration would on “day one” take aim at the 2017 Tax Cuts and Jobs Act, the Trump administration’s most explicit gift to investors.

Whatever its social merits, the tax cut mattered for markets. A year after it was enacted, profits for S&P 500 companies surged more than 20% in three consecutive quarters, a rate not seen since the financial crisis ended, as earnings in aggregate for large public companies rose to a record. While Wall Street sees several scenarios in which Biden’s pledge to roll back the cuts dies on the vine, particularly if Congress remains split, some worst-case models see its enactment cutting S&P 500 profit growth by close to half in 2021.

For his part, alongside pledging to raise the corporate tax rate to 28% from 21%, Biden has expressed desire for a higher minimum wage. His tax plan also includes raising long-term capital gains tax rates for high earners.

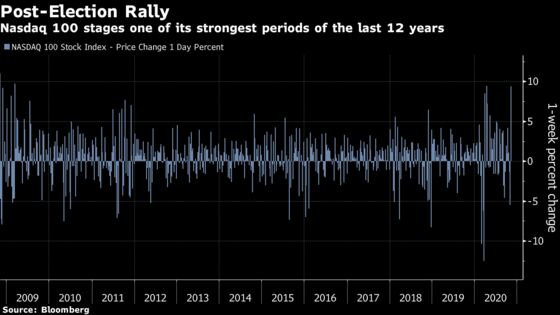

To date, of course, the stock market has evinced nary a sign of skepticism. The S&P 500 surged 7.3% this past week, while the tech-heavy Nasdaq 100 jumped 9.4%, the most since April. In a four-day period encompassing election night, the S&P 500 rose more than 1% each day, a streak that’s only occurred three other times in history.

While rare, such buoyancy has correlated with strong 12-month returns in the past, with an average S&P 500 gain of 26% one year later, according to Ryan Detrick, chief market strategist for LPL Financial.

In justifying the optimism, pundits cited the likelihood of divided government, even after saying a week earlier that a Democratic sweep would bode well for markets. With diminished odds of a blue wave -- a Biden presidency and a Democrat-controlled Congress -- Peter Tchir, head of macro strategy at Academy Securities, predicts Biden and his party will have to govern more with a centrist tilt, starting with a smaller aid package to offset the virus’ hit to the economy.

In his view, that means policy reform including a corporate tax hike and the implementation of a higher capital gains tax face an uphill battle.

Another question of interest to markets is Biden’s approach to Covid-19 and how willing his administration would be to sacrifice the economy to control its spread. The former vice president hasn’t always been clear about his plans, pledging to rely on science and saying it’s possible to “walk and chew gum at the same time.” Total daily cases in the U.S. surpassed 100,000 this week.

“The biggest factor investors have to be aware of and the biggest thing that’s going to determine returns in the short-term is Covid,” said Chris Gaffney, president of world markets at TIAA Bank. “It’s not going to be who’s in the White House, it’s not going to be if we get a stimulus package or not. It’s all about Covid right now.”

Then there’s nosebleed valuations at which the stock market is perched. Interest rates may be low, giving cover to stretched equity multiples, but at the end of September, the S&P 500 fetched 36 times profits under standard accounting, more than double the usual at that point of the election cycle. When multiples were near that in the past, stocks averaged 5% annual gains in the ensuing decade -- a subpar rate -- according to S&P 500 Dow Jones data compiled by Bloomberg since 1936.

History shows that presidents matter little for equity prices, or at least their party affiliation: S&P 500 returns are similar regardless of who’s in power, and usually they’re positive. The bigger influence has tended to be what’s going on in the economy and markets themselves. And right now, not only are a pandemic and recession raging, but stocks, particularly tech stocks, are trading at prices that even hardened bulls struggle to justify.

While valuations are a poor tool for timing, they’re a consideration in expected returns, meaning Biden could face an uphill battle keeping equities aloft no matter what he does.

“It seems very unlikely given where we are with valuations and rates that asset returns will match what we saw with Obama or with Trump just because we’re at a higher level and with potentially weaker growth,” said Elliott Savage, portfolio manager at YCG Investments. “Assets are priced to probably give lower returns going forward.”

©2020 Bloomberg L.P.