Why Asia’s Banking Hubs Are Making Virtual a Reality

Allowing virtual banks to operate means more competition, which may eventually lead to a price war.

(Bloomberg) -- Long gone are the days when banking meant having to stand in line at crowded branches to cash a check or apply for a loan. Automated teller machines, the internet and mobile apps mean many people hardly ever step foot inside their bank. So-called virtual banks question the need for brick-and-mortar branches altogether. With catchy names such as Ally and Simple in the U.S., Monzo in the U.K. and WeBank and MYbank in mainland China, these digital-only upstarts have been signing up lots of customers, especially among the young. Now Asia’s financial hubs, Hong Kong and Singapore, are getting ready to hop on the bandwagon, issuing licenses for new entrants.

1. What’s a virtual bank?

The Hong Kong Monetary Authority defines it as a bank that delivers services through the internet or other electronic channels instead of physical branches. That means not only facilitating payments but accepting deposits and making loans, just like traditional ones. Other terms used interchangeably include digital or digital-only banks or neobanks. By contrast, so-called digital wallets or e-wallets such as Apple Pay, PayPal or Google Pay usually serve as intermediaries between a consumer’s traditional account or credit card and a merchant, usually via a smartphone or computer.

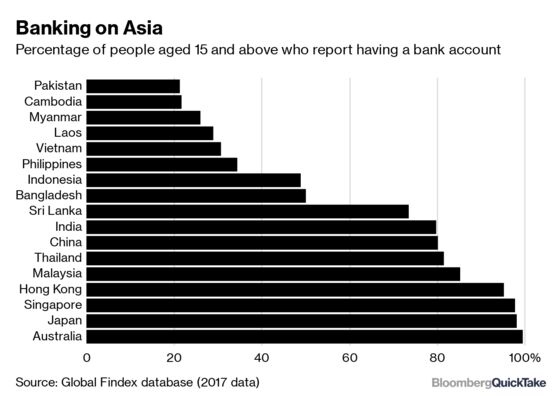

2. What’s the draw in Asia?

Hundreds of millions of people under-served by traditional institutions, for one thing. In China, India and elsewhere, digital wallets such as Alipay, WeChat Pay and Paytm have already become ubiquitous, offering millions of people an easy way to store and spend their money via mobile phone. Indonesia, Vietnam and the Philippines are also among the world’s biggest under-banked countries; together they have almost half a billion people.

3. Are Hong Kong and Singapore short on banks?

No, but the two cities are among the most cash-reliant major economies, leaving room for newcomers to disrupt the entrenched industry. Ant Financial, an Alibaba Group Holding Ltd. affiliate that runs Alipay and MYBank, and Tencent Holdings Ltd., the company behind WeBank and WeChat Pay, are among the owners of the eight ventures licensed to create virtual banks in Hong Kong, with operations expected to start as early as the end of the year. The Monetary Authority of Singapore will invite applications in August for as many as five virtual banking licenses. Taiwan joined in as well, approving in July the creation of three virtual banks.

4. How do virtual banks work?

Customers do everything from opening accounts to borrowing money to wealth planning using their mobile phone or computer. Some allow cash deposits or withdrawals from others’ ATM networks, using debit or credit cards. In Japan, Seven Bank, a unit of Seven & I Holdings, has its ATMs in 7-Eleven convenience stores. In the U.S., some even provide checkbooks. The new entrants in Hong Kong have yet to announce what their specific offerings will be.

5. What’s the advantage?

More people can gain access to financial services in under-served markets. Increased competition is also expected to lead to lower service charges and higher interest paid on savings accounts. From the banks’ perspective, operating only digitally reduces costs as they don’t need to rent or acquire space for branches and hire tellers to run the operations, although they will still need back-office and support staff. And yes, Hong Kong and Singapore are among the world’s most-expensive office markets.

6. Are they safe?

In most places, they are subject to the same set of supervisory requirements applied to conventional institutions. While banks in Hong Kong are required to have at least HK$300 million (about $40 million) in paid-up capital, the new virtual entrants have lined up an average HK$1.9 billion each, according to the HKMA.

7. Who are they targeting?

Along with the general public, the HKMA has told the licensees also to focus on small- and medium-sized enterprises. Some small-business owners without a long track record have had difficulty opening accounts at major traditional banks, which have been stepping up compliance efforts to meet mounting regulatory requirements. The HKMA warned banks in 2016 about the risk of excluding legitimate businesses from financial services by being too heavy handed with due diligence.

8. Are traditional banks threatened?

Maybe. Allowing new firms to operate means more competition, which may eventually lead to a price war. Traditional banks already offer many online or digital transactions. HSBC Holdings Plc says its digital wallet PayMe has more than 1.5 million users in Hong Kong. Some have already begun to scrap fees they charge accounts with low balances, in a bid to hold on to customers. An analysis by Bloomberg Intelligence found the eight new entrants may reach a combined profit of 7% of HSBC’s in Hong Kong in five years’ time. Analysts at Citigroup Inc. estimate around 10% of existing banks’ revenue is at risk over the next decade.

Licensed virtual banks in Hong Kong |

Ant SME Services (Hong Kong) Ltd.

|

Fusion Bank Ltd.

|

Insight Fintech HK Ltd.

|

Ping An OneConnect Co.

|

Welab Digital Ltd.

|

Livi VB Ltd.

|

SC Digital Solutions Ltd.

|

ZhongAn Virtual Finance Ltd.

|

The Reference Shelf

- Bloomberg Intelligence sees growth for North Asia’s online banks.

- S&P Global Ratings report on virtual banking in Asia-Pacific.

- HSBC’s dominance in Hong Kong is a juicy target for virtual banks.

- Bloomberg Opinion on HSBC’s race with virtual banks.

- "Rare" wave of hiring in Hong Kong as virtual banks staff up.

- In rush to be Uber of finance, this mobile bank tests the limits.

- Banks waking up to fintech threat throw billions into digital.

- Jack Ma’s $290 billion loan machine is changing Chinese banking.

To contact the reporter on this story: Alfred Liu in Hong Kong at aliu226@bloomberg.net

To contact the editors responsible for this story: Sam Mamudi at smamudi@bloomberg.net, Paul Geitner, Jeanette Rodrigues

©2019 Bloomberg L.P.