The Great British Retail Selloff Beckons the Bears: Taking Stock

The Great British Retail Selloff Beckons the Bears: Taking Stock

(Bloomberg) -- The clouds keep accumulating above European equities. The S&P 500 got hit again yesterday, closing down more than 2% to its lowest level since October 2017. Asian Markets are following through and Euro Stoxx 50 futures are 0.5% lower ahead of the European open.

The list of sectors in the grip of a bear market is growing fast. After banks depressed by low interest rates and trading difficulties, come autos, basic resources, chemicals, technology and personal goods affected by tariffs and slower global growth. Now another one is about to slip: retail.

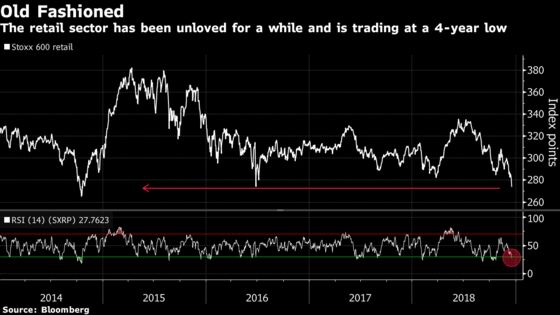

The rout yesterday in online retailers following a profit warning from Asos was another push that brought the sector near to bear-market territory. The Stoxx 600 retail index (SXRP) is now at its lowest level in four years, down 19 percent since its peak in June, and back into oversold territory.

Retail woes aren’t new. The sector has been trading range-bound since 2016 with depressed consumer spending and confidence, and has been resorting to large discounts to try to reduce growing levels of stock. Unlike the broader market, the Stoxx 600 Retail never recovered from 2015’s slump.

Asos’s latest warning is another sign that the outlook isn’t getting any brighter. The British online giant was hit by unseasonably warm weather and also confirmed that consumer spending was slowing not only in the U.K., but in France and Germany, too. Looking across Europe, it’s clear that the problem lies deeper in the U.K. The weak pound, Brexit shambles as well as consumers getting squeezed for years by government austerity policies, have taken their toll on a sector relying on consumers to spend more.

What’s the wider European picture then? It’s grim: low growth, low inflation, low demand. Since the ECB’s Governing Council devised plans in the summer to halt quantitative easing at 2.6 trillion euros ($3 trillion) by the end of the year, the economy has shown signs of weakening momentum. Output contracted in two of the region’s three largest economies in the third quarter, and confidence in a strong rebound have diminished amid trade tensions, the threat of a no-deal Brexit and Italy’s fiscal troubles. If you remove food and energy from the latest CPI numbers, inflation in Europe is about 1 percent.

So is it a buying opportunity? Well, the problem with most of these fashion outlets is that they’re still pricey. Even after a glum year, the sector has been trading at a premium to the broader market for most of 2018. If the price-to-earnings ratios remain high after this year’s drop, it means that profit expectations have tumbled too. Grim again.

So will Christmas sales bring some respite? Not much. Trading has been way too tough, and a last-minute shopping spree is not likely to save the sector from a year to forget.

“The set up for peak trading for the European retailers looks weak with retailer commentary and industry data suggesting a severe slowdown in November and insufficient time to recover ahead of Christmas,” wrote Citi analyst Adam Cochrane in a note. “It appears the U.K. consumer weakness we have discussed is now spreading to Europe with increased inventory clearance an additional headwind. Whilst valuations across the sector are approaching trough levels, the negative earnings momentum will likely continue in January and the catalyst for the re-rating is hard to identify at this stage.”

The U.K. Parliament’s vote on the Brexit plan has been set for Jan. 14, which could give a clearer direction to where the country is going. But retailers will need a real improvement in consumer confidence and spending to recover. A glimmer of hope for their share prices could be a “not-that-bad-outlook” from some large chains after the new year. That could trigger a short squeeze in a sector that is the darling of short sellers, as shown below.

| Stock | SI (% of free float) | Days to Cover |

| H&M | 16.8% | 33 |

| Zalando | 14.0% | 26 |

| Asos | 8.9% | 12 |

| Source: Markit data, as of Dec. 14 | ||

- Watch the pound and U.K. stocks as another no-confidence motion in Prime Minister Theresa May has been proposed by Jeremy Corbyn, leader of the opposition Labour Party, only hours after he declined to propose such a motion in the House of Commons. Although unlikely to pass, it provides yet another reason for investors in U.K. assets to remain on tenterhooks.

- Watch oil stocks as the oil price took another move lower after a new report indicating expanding stockpiles in the U.S. reignited concerns about a supply glut in the market. This nervousness looks unlikely to end in 2018 or at least until there is some clarity about to what extent OPEC countries and Russia will trim production to underpin prices, or indeed how far they will go to meet the promises set out.

- Watch rates and impact on equities as the U.S. Federal Reserve set to begin another pivotal policy meeting on Tuesday, before announcing its rate decision on Wednesday, President Donald Trump barreled back into the debate about the hiking cycle. Trump said it was “incredible’’ the Fed would even consider another interest rate hike given the “very strong dollar and virtually no inflation,’’ not to mention that the “world is blowing up around us.’’ Trump’s broadside aside, markets may remain in a holding pattern for the next two days until the Fed announces its decision.

- Watch technology stocks, particularly cloud providers and software, after expectation-busting numbers overnight from U.S. firms Oracle and Red Hat. Oracle is a bellwether for the industry and its forecast for stronger sales growth as it transitions over to cloud services should have a positive read-across for SAP. Red Hat, meanwhile, should also provide a little boost for enterprise software names like Micro Focus International after its third-quarter earnings outpaced analyst consensus.

COMMENT:

- “Post QE world has unleashed political risk on financial markets; this has fueled enhanced investor uncertainty, elevated volatility and stiffened headwinds to economic/EPS growth in Europe and around the world,” Citi strategists write in a note. “Equity markets could fall ~5%-10% in 1Q 2019 on weaker data and various political risks (Brexit, Italy, France), but we expect 2019 to deliver positive returns and target Stoxx at 400 for end-2019; no 2019 recession, extending cycle, modest DPS growth and re-rating.”

COMPANY NEWS AND M&A:

- Eiffage bought 5.03% of Getlink on the market, the company says in an emailed statement on Monday after the close of trading in Paris.

- Royal Dutch Shell is in negotiations to buy Endeavor Energy Resources for about $8 billion, according to people familiar with the matter.

- Elliott Could Weigh Raising Stake in Telecom Italia: MF

- EE Intressenter Offers SEK87 for Each Cherry Share

- Nordex Gets 83MW Follow-Up Order For Vientos Neuquinos Wind Farm

- Nordea Says It Has Been Misused for Money Laundering in Past: JP

- Figeac Aero Confirms Short and Mid Term Targets

- Nissan CEO Is Said to Travel to Alliance Meeting Amid Tensions

- Unicaja, Liberbank Mull Selling Stakes in Caser: Expansion

- Salini, Fincantieri, Italferr to Build Genoa Bridge: Repubblica

- Voltalia Reaffirms Confidence in Ability to Reach ’20 Targets

- DNB Buys Oslo Office Building From Bane NOR Eiendom for NOK1.7B

- Thule Buys Tepui Outdoors for $9.5m on Cash/Debt-Free Basis

- Idorsia’s P2Y12 Phase 2 Clinical Studies Meet Objectives

- Rockwool’s Russian Business Is Doing Well, CEO Tells Borsen

- Glencore Lifts Stake in Australian Coal Mines W/ Mitsubishi Deal

- Wolfgang Porsche Doesn’t See Porsche IPO as A Topic Now: FAZ

NOTES FROM THE SELL SIDE:

- RBC outlines its 30 global stock ideas for 2019, saying its analysts are maintaining a pro-cyclical, pro-growth bias but with a focus on “quality cyclicals.” ABN Amro and Cineworld both upgraded to top picks in Europe. Sees opportunities in financials after challenging 2018, plus “unwarranted discounts” in pockets of energy sector. For Europe, ABN Amro upgraded on likelihood for a meaningful rise in shareholder returns from 2019 on; Cineworld upgraded as Regal acquisition provides co. with much larger footprint on which to use its proven management skills. Other European picks include miner Fresnillo, retailer Inditex, take-out delivery firm Just Eat, insurer Legal & General and industrial turnaround co. Melrose Industries.

- Berenberg lowered JCDecaux’s 2019 forecasts, as the French advertising company’s 1H results are likely to look more like those in 2018 than previously expected as Spanish airports continue to weigh on profits and a contract in Paris has yet to produce revenue.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 353.2 (50% Fibo); 362 (March low)

- Support at 341.2 (61.8% Fibo); 326.5 (74.4% Fibo)

- RSI: 38.4

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,072 (61.8% Fibo); 3,172 (50-DMA)

- Support at 2,985 (Dec 2016 low); 2,921 (76.4% Fibo)

- RSI: 40

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- ABN Amro GDRs upgraded to top pick at RBC; Price Target 30 Euros

- Cineworld upgraded to top pick at RBC; Price Target 3.50 Pounds

- CompuGroup raised to buy at Baader Helvea; Price Target 49 Euros

- Eiffage upgraded to hold at Kepler Cheuvreux; PT 91 Euros

- JCDecaux raised to equal-weight at Morgan Stanley; PT 24 Euros

- Remy Cointreau raised to market perform at Bernstein

- Technotrans upgraded to buy at HSBC; PT 34 Euros

- Zalando upgraded to buy at DZ Bank; PT 28 Euros

DOWNGRADES:

- Asos downgraded to hold at Santander; PT 40.79 Pounds

- Coface downgraded to hold at Kepler Cheuvreux; PT 7.50 Euros

- Nemetschek downgraded to reduce at Kepler Cheuvreux; PT 85 Euros

- Pfeiffer Vacuum downgraded to hold at HSBC; PT 127 Euros

INITIATIONS:

- BioInvent International rated new buy at Pareto Securities

- Cewe Stiftung rated new buy at Kepler Cheuvreux; PT 94 Euros

- Colonial rated new neutral at Citi

- IG Group rated new buy at Peel Hunt; PT 7.75 Pounds

- Logitech rated new outperform at Wedbush; PT 40 Francs

- M1 Kliniken rated new buy at Commerzbank; PT 19 Euros

- Merlin rated new neutral at Citi

- Plus500 rated new hold at Peel Hunt; PT 15 Pounds

- SGL rated new hold at Deutsche Bank; PT 7 Euros

- Zooplus rated new underperform at MainFirst; PT 114 Euros

MARKETS:

- MSCI Asia Pacific up 0.3%, Nikkei 225 down 1.8%

- S&P 500 down 2.1%, Dow down 2.1%, Nasdaq down 2.3%

- Euro down 0.09% at $1.1338

- Dollar Index up 0.03% at 97.13

- Yen up 0.17% at 112.64

- Brent down 1.7% at $58.6/bbl, WTI down 1.7% to $49/bbl

- LME 3m Copper down 0.3% at $6107/MT

- Gold spot little changed at $1245.4/oz

- US 10Yr yield down 1bps at 2.84%

MAIN MACRO DATA (all times CET):

- 9am: (SP) 3Q Labour Costs YoY, prior 0.7%

- 10am: (GE) Dec. IFO Business Climate, est. 101.7, prior 102

- 10am: (GE) Dec. IFO Expectations, est. 98.4, prior 98.7

- 10am: (GE) Dec. IFO Current Assessment, est. 105, prior 105.4

--With assistance from Hanna Hoikkala and Lisa Pham.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2018 Bloomberg L.P.