(Bloomberg Opinion) -- Just over a week ago, Elon Musk was tweeting about flying cars. On Friday, he did something much more like a run-of-the-mill car executive: He announced layoffs.

Tesla Inc. is cutting 7 percent of its full-time staff. This follows a 9 percent cut in the middle of last year. Remarkably, despite that earlier round of reductions, Musk said in his latest update that headcount expanded 30 percent last year. Having ended 2017 with about 37,500 employees, the CEO tweeted an updated figure of 45,000 last October. So the latest cuts should affect around 3,000 to 3,500 people.

What makes this unusual is that Tesla is also supposed to be expanding at a rapid clip. Its pipeline includes a new factory in China (also the subject of much tweeting earlier this month), a pickup truck, the semi truck, the Model Y and, lest we forget, those solar roofs. Plus, as Musk writes himself:

Tesla will need to make these cuts while increasing the Model 3 production rate and making many manufacturing engineering improvements in the coming months.

When General Motors Co. announced sweeping cuts a couple of months ago, its stock actually jumped. Investors in automotive stocks are a fairly miserable bunch, you see; hardened by decades of wrenching cycles, they judge companies chiefly on how quickly management accepts the essential grimness of their reality. Plus, GM trades at just 6 times forward GAAP earnings. Tesla, however, trades at a somewhat sunnier 133 times earnings. Hence, its stock was down about 7 percent in pre-market trading Friday.

This isn’t because of worries about profits. Musk wrote that “preliminary, unaudited results” indicate Tesla made a GAAP profit in the fourth quarter of 2018, but lower than the previous quarter’s 4 percent margin. Consensus forecasts imply a margin of 3 percent anyway.

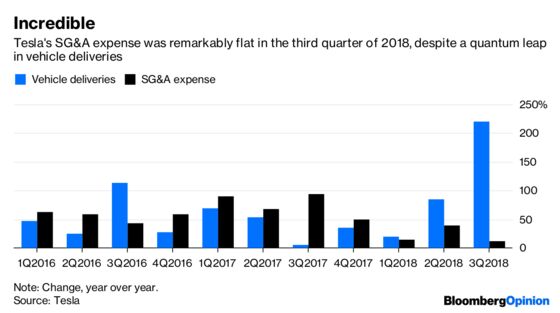

The problem is dissonance. When Tesla reported surprisingly robust third-quarter results in November, it helped for many to draw a line under the “funding secured” debacle. Yet doubts about the sustainability of that performance linger, given Tesla sold a big slug of emissions credits and was selling higher-spec, higher-priced versions of the Model 3. Meanwhile, Tesla’s operating expenses were remarkably flat despite a huge increase in vehicle deliveries.

To a Tesla bull, that quarter represented the pivot point, when economies of scale from surging Model 3 production kicked in. Yet, as Friday’s latest announcement shows, that is still a work in progress. For the current quarter, Musk hopes selling higher-end Model 3s in Europe and Asia will, with “some luck,” result in a “tiny profit.” The $35,000 Model 3, first teased almost three years ago, remains an elusive objective, with Musk’s statement suggesting it won’t appear until the second half of this year at the earliest (he wrote that the need for “lower priced variants” would increase as tax incentives, which fell at the start of the January, fall further in July and at the end of the year). Tesla’s recent decision to cut prices across the fleet also undercuts the story of limitless growth.

For Tesla to fulfill the staggering growth required to justify its valuation, spending and capex should be increasing. Striving to be more efficient is laudable. The problem for Tesla bulls is that big staff cuts are what ordinary car companies do.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.