Tesla Bull Case Raised at Morgan Stanley After Just Three Weeks

Tesla Bull Case Raised at Morgan Stanley After Just Three Weeks

(Bloomberg) -- Morgan Stanley increased its bull-case price target for Tesla Inc. for the second time in three weeks, saying it’s “increasingly obvious” the firm’s revenue might exceed that of traditional automakers like Toyota Motor Corp. and Volkswagen AG within a decade.

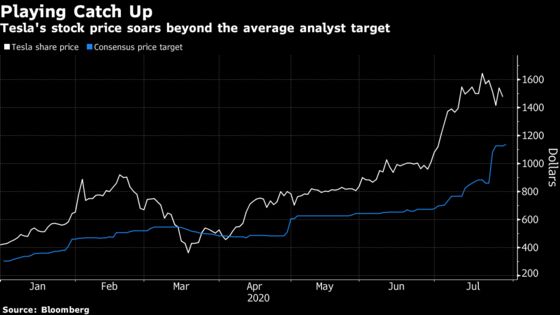

But despite a best-case valuation target of $2,500-- compared with Tuesday’s closing price of $1,476.49 -- the broker still recommends selling the electric car-manufacturer’s shares.

“One year ago, we believed the legacy original equipment makers would have had a far more advanced strategic position to pressure Tesla market share,” analyst Adam Jonas wrote in a note. “However; Tesla has had, in our opinion, much more freedom to expand than we initially thought.”

Jonas updated his volume projections following second-quarter results after Chief Executive Officer Elon Musk reiterated a desire to prioritize growth over profit. The analyst lifted his 2030 unit forecast to 3 million from 2.3 million previously after including new vehicles like the Cybertruck and Multipurpose Van and accounting for an additional three full factories of production.

Morgan Stanley upped its best-case scenario target to $2,500 from the $2,070 valuation given July 7, while increasing its regular target to $1,050 from $740. With the latter suggesting 29% downside for the shares, the analysts maintained an underweight rating.

Jonas “would need much more” to upgrade the stock, in terms of volume and autonomous vehicle revenue, while at the same time ignoring near-term risks like U.S.-China relations and potential future competition from the largest U.S. technology companies, he wrote.

©2020 Bloomberg L.P.