Strong Conviction Needed to Be Long European Banks

Strong Conviction Needed to Be Long European Banks

(Bloomberg) -- What’s in it for us? The question could be raised by banks as, according to a survey of economists, the European Central Bank is set to cut its deposit rate this week, again in December, and will re-start asset purchases. Banks are still by far the worst-performing sector in Europe this year, and even if the ECB provides some specific support for the industry, a brighter future still seems out of sight.

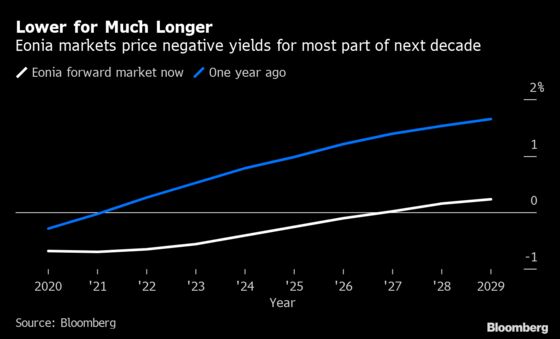

“Lower for longer” is the motto. Interest rate curves are pointing to negative ECB rates until 2030, and the new wave of monetary policy easing “represents a significant input cost shock for Europe’s banks, which face the real prospect of declining revenues,” UBS analysts write. The consequences could be “an autumn of disappointing strategic updates” as consensus profit estimates suggest almost all banks will miss their return-on-tangible-equity targets, they say.

No wonder bank chiefs have started to prepare the market. Last week the CEO of Deutsche Bank warned against the “grave side effects” of negative rates for the region with a similar tone taken by UBS.

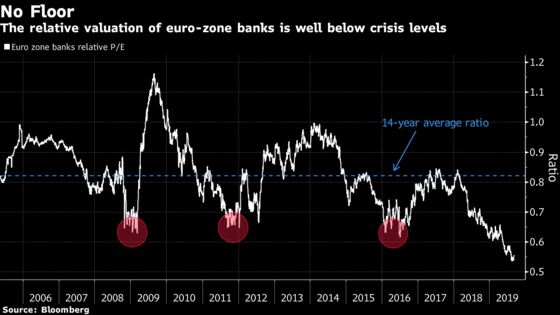

Banks’ relative valuations have fallen deeper into uncharted territory, with a discount to the market well below the 2009, 2011 and 2016 levels. If banks look like a screaming value call, they might well be a value trap, according to strategists at BNP Paribas. The fall in interest rates and the penalty associated with negative rates in Europe remain bitter headwinds, and the potential short-term ECB relief for the industry in the form of tiering won’t be enough to change the structural issues, they say.

Still, tiering provides hope: it would create exemptions from the negative yields on money deposited by lenders at the central bank. This could lift the industry’s return on equity by as much as 46 basis points depending on the size and scope of the tiering features, Scope analyst Chiara Romano wrote in a report Friday. For German lenders, the impact could even be bigger, up to 71bps, given the high reliance on net interest income, Romano says.

The 7% bounce of the sector since mid-August perhaps offers a “technical” silver lining, as banks avoided falling back into their long-term downtrend. The banking sector is bouncing from a very important support and it could develop a positive reaction for a few months, according to technical analysts at Day By Day.

After that, the picture isn’t so bright, say the chartists, as technically, there’s nothing to suggest that the relative strength of the banking sector has met its ultimate bottom. Indeed, European bank stocks have never really recovered from the credit crunch and every bounce was short-lived, leading to new lows as sentiment failed to recover.

In the meantime, Euro Stoxx 50 futures are up 0.1% ahead of the European open, while S&P 500 contracts are up 0.2%.

- Watch oil stocks after Saudi Arabia ousted its long-time energy minister just before an OPEC+ committee that monitors compliance with output cuts meets this week in Abu Dhabi.

- Watch the pound and U.K. stocks after Prime Minister Boris Johnson said he still plans to push ahead with his plan to make sure the U.K. leaves the European Union on Oct. 31, despite a woeful week of defeats and another major resignation. Even pound traders already prefer Labour’s Jeremy Corbyn.

- Watch Hong Kong-exposed stocks as leader Carrie Lam’s biggest concession yet to protesters did little to stem scenes of violence that have become the norm on weekends in the Asian financial hub.

COMMENT:

- “Growth companies’ valuations are at all-time highs, and further earnings momentum is needed to sustain gains, in our view,” Bloomberg strategists Laurent Douillet and Tim Craighead write in a note. “Factor rotation during the summer months has put momentum and growth back into the top spots, while value continues to struggle in the face of energy- and financial-sector earnings cuts.”

NOTES FROM THE SELL SIDE:

- European flavor and fragrances stocks are not as attractive compared to staples as they once were, but the organic growth offered by the segment is still superior and deserving of a premium, Berenberg says in a note upgrading Givaudan to buy from hold, with PT raised to CHF3,150. Symrise is kept at hold as good growth already reflected.

- ABN Amro’s rating is raised to overweight from equal-weight after underperformance made co. look appealing, Morgan Stanley says, keeping KBC as its top pick among Benelux banks.

- The container sector may struggle in FY20 to fully mitigate the 15%-20% higher bunker costs from IMO 2020, with market conditions seen as stable at best, Jefferies says, double-downgrading Hapag-Lloyd to underperform following a tripling of the share price.

- Mitchells & Butlers’ like-for-like sales should continue to outperform an improving U.K. pub market, while intense efficiencies are helping offset costs pressures, Morgan Stanley writes in note; upgrades to overweight from equal-weight.

COMPANY NEWS AND M&A:

- British Airways Cancels Hundreds of Flights Over Pilot Strike

- Thyssenkrupp CEO Said to Prefer Minority Sale for Elevator Unit

- Air France-KLM Aug. Group Passenger Traffic Rises 2.1%

- Deutsche Bank Reorganizes Domestic Corporate Banking Unit: HB

- Swiss Re Sees More Rate Increases for Loss-Affected Businesses

- Nissan CEO Saikawa Plans to Resign: Nikkei

- Carige Seeks Minority Investors’ Backing on Share Sale: Sole

- VTB in Talks With Chinese Cos. Over Possible En+ Investment: FT

- Vukile Prepares EU700M Offer for LAR Espana: El Confidencial

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 395.1 (July high); 397.9 (June 2018 high)

- Support at 381.2 (50-DMA); 372.2 (200-DMA); 365.5 (50% Fibo)

- RSI: 64.1

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,515 (May high); 3,596 (May 2018 high)

- Support at 3,436 (50-DMA); 3,403 (61.8% Fibo); 3,316 (200-DMA)

- RSI: 63.2

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Altice Europe raised to overweight at JPMorgan; PT 5.50 Euros

- Berkeley upgraded to buy at HSBC; PT 45.40 Pounds

- Givaudan upgraded to buy at Berenberg

- McCarthy & Stone upgraded to buy at HSBC; PT 1.60 Pounds

- Mitchells & Butlers upgraded to overweight at Morgan Stanley

- Moncler upgraded to buy at HSBC; PT 43 Euros

- NetEnt upgraded to buy at SEB Equities; PT 40 Kronor

- Nordex upgraded to outperform at Macquarie

- Ultra Electronics raised to equal-weight at Barclays

DOWNGRADES:

- Deutsche Wohnen Cut to Underweight at Barclays; PT 32 Euros

- Entertainment One downgraded to hold at Berenberg

- Hapag-Lloyd downgraded to underperform at Jefferies

- Orange downgraded to neutral at JPMorgan; PT 15 Euros

- Recordati cut to neutral at Goldman; Price Target 42 Euros

- Verbund downgraded to hold at HSBC; PT 56 Euros

- Wizz Air downgraded to neutral at Davy

INITIATIONS:

- Bigblu Broadband Rated New Overweight at Barclays; PT 2 Pounds

- Judges Scientific rated new buy at Liberum; PT 41.35 Pounds

- Kojamo rated new buy at SEB Equities; PT 16 Euros

- MorphoSys rated new outperform at MainFirst; PT 140 Euros

- Spire Healthcare rated new outperform at RBC; PT 1.49 Pounds

MARKETS:

- MSCI Asia Pacific up 0.6%, Nikkei 225 up 0.6%

- S&P 500 up 0.1%, Dow up 0.3%, Nasdaq down 0.2%

- Euro down 0.02% at $1.1027

- Dollar Index up 0.04% at 98.44

- Yen up 0.06% at 106.86

- Brent up 1% at $62.1/bbl, WTI up 1.1% to $57.1/bbl

- LME 3m Copper down 0.3% at $5814.5/MT

- Gold spot up 0.3% at $1510.8/oz

- US 10Yr yield little changed at 1.56%

ECONOMIC DATA (All times CET):

- 8:30am: (EC) Bloomberg Sept. Eurozone Economic Survey

- 8:30am: (FR) Aug. Bank of France Ind. Sentiment, est. 96, prior 95

- 8:35am: (GE) Bloomberg Sept. Germany Economic Survey

- 8:40am: (FR) Bloomberg Sept. France Economic Survey

- 8:45am: (IT) Bloomberg Sept. Italy Economic Survey

- 8:50am: (SP) Bloomberg Sept. Spain Economic Survey

- 10:30am: (UK) July Index of Services MoM, est. 0.1%, prior 0.0%

- 10:30am: (EC) Sept. Sentix Investor Confidence, est. -13.3, prior -13.7

- 10:30am: (UK) July Industrial Production MoM, est. -0.2%, prior -0.1%

- 10:30am: (UK) July Industrial Production YoY, est. -1.2%, prior -0.6%

- 10:30am: (UK) July Manufacturing Production MoM, est. -0.2%, prior -0.2%

- 10:30am: (UK) July Manufacturing Production YoY, est. -1.25%, prior -1.4%

- 10:30am: (UK) July Monthly GDP (3M/3M), est. -0.1%, prior -0.2%

- 10:30am: (UK) July Construction Output YoY, est. 0.0%, prior -0.2%

- 10:30am: (UK) July Monthly GDP (MoM), est. 0.1%, prior 0.0%

- 10:30am: (UK) July Index of Services 3M/3M, est. 0.1%, prior 0.1%

- 10:30am: (UK) July Visible Trade Balance GBP/Mn, est. £9.9b deficit, prior £7.01b deficit

- 10:30am: (UK) July Trade Balance Non EU GBP/Mn, est. £3.0b deficit, prior £186.0m deficit

- 10:30am: (UK) July Trade Balance GBP/Mn, est. £1.25b deficit, prior £1.78b

- 10:30am: (UK) July Construction Output MoM, est. 0.2%, prior -0.7%

To contact the reporters on this story: Jan-Patrick Barnert in Frankfurt at jbarnert3@bloomberg.net;Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.