SoftBank Debtholders Hope For More Caution After WeWork Woes

SoftBank Debtholders Hope For More Caution After WeWork Woes

(Bloomberg) -- Many bond market participants still think billionaire Masayoshi Son’s SoftBank Group Corp. is a relatively safe bet, but a bumpy few weeks for the corporate investor has prompted some to pine for a bit more caution.

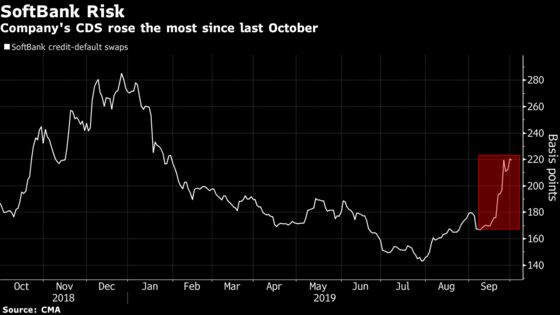

The cost to insure the firm’s debt against nonpayment climbed the most in nearly a year last month after WeWork’s efforts to go public failed and Uber Technologies Inc.’s valuation sagged. The value of SoftBank’s stake in Alibaba Group Holding Ltd. also plunged about $6.1 billion in a single day following a tumble in the Chinese company’s shares on news that the White House is weighing limits on U.S. portfolio flows into China.

SoftBank Group is having to face volatile market moves as its business increasingly takes on the characteristics of an investment firm, and it’s committed $38 billion of its capital for a new technology fund. But in spite of scares related to its marquee investments like WeWork and Alibaba, a debt gauge that analysts look at to judge SoftBank’s financial health suggests it remains in decent shape.

“SoftBank was like a vehicle that was going too fast,” said Toshiyasu Ohashi, chief credit analyst at Daiwa Securities Group Inc. in Tokyo. “But it would be positive for its credit if these problems prompt SoftBank to be more cautious in its investments through its Vision Fund.”

See also: WeWork woes wipe out SoftBank gains from $5 billion buyback

SoftBank Group’s focus on investment after splitting off its telecom business has prompted analysts to look at its loan-to-value ratio, which measures net interest-bearing debt against the value of investments, to judge its leverage. Son has said he wants to keep the gauge below 25%. It stood at 18% as of Tuesday, according to company data.

While WeWork’s woes have been big news recently, some say its impact on SoftBank’s finances should be limited considering the sheer size of Son’s investments. Even if WeWork’s value falls to zero, SoftBank’s LTV ratio will only rise by a few percentage points, according to Ohashi at Daiwa Securities.

SoftBank spokesman Kenichi Yuasa declined to comment.

Still, market data suggest that investor concern about SoftBank’s outlook is increasing.

Read more: SoftBank’s WeWork distress drags Asia communication shares

The company’s credit-default swaps rose 42.5 basis points to 222 in September, the biggest increase since October last year, according to CMA data. Some traders expect the swaps to rise back up to 250 basis points, a level they last touched at the start of the year.

Alibaba’s 5.2% share plunge on Friday highlights other risks. With a 26% stake in the Chinese e-commerce firm, that cut the value of SoftBank’s holdings by $6.1 billion in a single day. The shares dropped 1.2% on Tuesday, after rebounding 0.8% on Monday.

SoftBank may also face losses of as much as $5 billion on its investment in WeWork, according to Kentaro Harada, a Tokyo-based senior credit analyst at SMBC Nikko Securities Inc.

Alibaba’s share moves are of concern for S&P Global Ratings, but the stock would have to drop more sharply to affect its credit score, which is one step below investment grade at BB+.

“Since Alibaba accounts for nearly half of the value of SoftBank Group’s portfolio, negative news related to the company may put pressure on SoftBank’s credit,” said Hiroyuki Nishikawa, associate director at S&P in Tokyo. “But there is room before we start considering a downgrade.”

To contact the reporter on this story: Ayai Tomisawa in Tokyo at atomisawa@bloomberg.net

To contact the editors responsible for this story: Andrew Monahan at amonahan@bloomberg.net, Ken McCallum

©2019 Bloomberg L.P.