Oil’s Biggest Threat Isn’t Tesla But Aversion

Oil’s Biggest Threat Isn’t Tesla But Aversion

(Bloomberg Opinion) -- A friend and energy expert recently asked: What’s the bigger threat to the oil industry, electric vehicles or renewable energy? My answer – which has taken on an added dimension amid the uproar over the killing of Jamal Khashoggi – was that the real challenge is something more amorphous, but bigger: aversion.

That isn’t to dismiss the two technologies he asked about – although it was a bit of a trick question. Electric vehicles using conventional power sources such as coal or natural gas don’t fully displace the carbon emissions of regular cars. Just as the marriage of automobiles with gasoline challenged the horse in early 20th-century transportation, so the marriage of electric vehicles with renewable energy challenges the internal combustion engine.

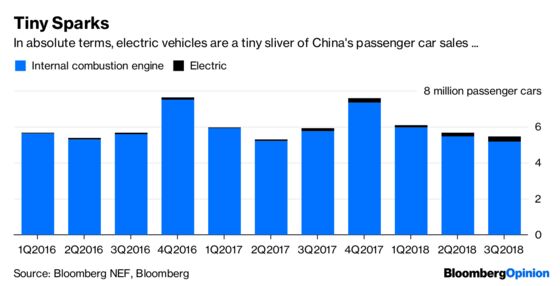

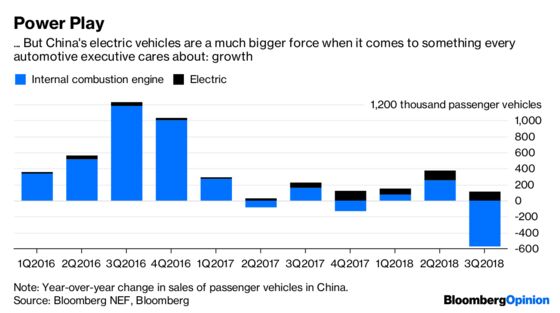

This is happening already in the market that, perhaps more than any other, will determine the shape of the 21st-century energy market: China. Sales of light-duty vehicles in the Chinese market – the world’s biggest since 2009 – fell 12 percent in September, year over year, the third monthly decline in a row. Yet sales of electric vehicles (including plug-in hybrids) jumped by 75 percent. They may constitute only 5 percent of the market, but in three of the past four quarters, they’ve accounted for half or all of the growth.

China’s rapid industrialization has taken an environmental toll, and Beijing has tried to address the resulting social discontent. Pollution in Chinese cities has decreased but last year remained far above World Health Organization standards. Encouraging renewable power and electric vehicles – as well as natural gas muscling in on coal – makes sense and will continue to do so.

Another consideration is strategic. Unlike the U.S., China isn’t an oil and gas powerhouse, and its rising import dependence leaves it at the mercy of the navy of a certain superpower currently waging a trade war on it. It also makes China dependent on that notably less-predictable regime in Riyadh. These are not positions Beijing relishes. The country’s strength is in manufacturing, not extraction. So it has a vested interest in not repeating the 20th-century model of Western industrial development and instead doing for electric vehicles and batteries what it did for solar panels: manufacturing their costs into the ground.

Leaving China’s strategic considerations aside, aversion to oil has also crept in around the edges of the capital markets. At the extreme, this involves ditching fossil-fuel-linked investments altogether, usually on environmental or social grounds or concern that “peak demand” will undermine their value. More prosaically, the oil and gas industry is coming off a decade of poor returns teed up by the last investment boom. Desertion of the sector may not be quite at the levels of the Future Investment Initiative that limped into action in Saudi Arabia on Tuesday, but it hasn’t been winning any popularity contests:

My regular readers will know my skepticism about the valuation of a certain electric-vehicle maker. Tesla Inc. is festooned with red flags. The past few months alone have involved the CEO tweeting about a non-existent takeover deal; getting sued by regulators for it; then settling with them while also taunting them on Twitter. The stock has dropped by almost a third since early August.

Yet despite all this, Tesla’s market cap is still at $44.5 billion. Oil executives should ponder that the next time they get dragged for raising their capex budget 5 percent. This may seem absurd; but then, from a purely financial perspective, you could have said the same thing about the pre-2014 fracking boom.

The real problem here is that investors’ aversion – whatever the cause – is constraining investment in new oil and gas production; which could, in turn, tee up price spikes and economic damage. And who will get blamed for that? Somehow, I don’t think it will be Tesla.

Saying “it’s different this time” is a good way of eventually looking like an idiot. But it’s safe to say at least that the world around the oil and gas business has changed in several fundamental respects.

Long-term demand is no longer a mere function of economic projections. Competition between energies has gathered momentum, even in previously untouchable markets such as transportation.

That aversion has a powerful and implacable impetus: the existential threat of climate change. The latest report of the Intergovernmental Panel on Climate Change was a reminder that what has been implicitly treated as our descendants’ problem (a morally indefensible position anyway) requires urgent action now.

Efforts such as the Oil and Gas Climate Initiative show that at least some in the industry recognize the problem. Yet, as I wrote here, decades of foot-dragging by many companies contributed to the dangerous transformation of climate science into a form of political theology, making it tough to even debate solutions.

And now, as Khashoggi’s death and aftermath illustrate, the ground beneath the energy market’s feet is shifting to an extent not seen in decades. This isn’t about the killing of one journalist. It’s about previous geopolitical certainties such as America’s muscular commitment to free trade or Saudi Arabia’s cautious, consensus-driven politics (within the House of Saud, anyway) being upended. How could any planner in Beijing (or New Delhi) look at recent events and feel comfortable about long-term dependence on the energy status quo?

It’s a loss of hearts and minds that challenges energy’s incumbents. Renewable energy and electric vehicles are just tools enabling that to happen.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.