Tesla Deliveries Beat Everyone’s Forecasts: Morgan Stanley

Tesla Deliveries Beat Everyone’s Forecasts: Morgan Stanley

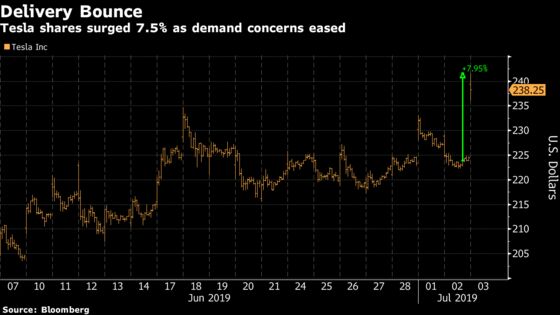

(Bloomberg) -- Tesla Inc. surprised Wall Street with record second-quarter deliveries that beat estimates, easing concerns over waning demand for the company’s electric cars that had pressured shares so far this year.

“While there were a good amount of ‘leaked’ emails and reports prophesizing a potential ‘record quarter’ for deliveries, we had not spoken to any investors that expected deliveries to be this high,” Morgan Stanley analyst Adam Jonas wrote in a note. “We expect the stock to squeeze and then fade on this news.”

Other analysts said the automaker’s beat on deliveries and inventory levels at the end of the quarter bode well for its cash position, and incoming orders for third quarter appeared strong.

Tesla shares surged as much as 7.6% Wednesday, to almost $242. That’s the highest intraday price for the stock in nearly two months. Shares had fallen 33% this year through Tuesday’s close amid concerns about demand and worries that the cheaper Model 3 is cannibalizing the company’s more lucrative vehicles.

Here’s a look at what analysts are saying:

Bernstein, Toni Sacconaghi

(Market perform, $325)

- Could be profitable this quarter on a non-GAAP basis even with materially pressured automotive gross margins, but models negative free cash flow of about -$200 to -$300 million.

- Questions sustainability of Model 3 demand and gross margin, considering U.S. accounted for almost 70% of Model 3s sold this quarter compared to less than 50% in the first quarter, suggesting domestic sales got a boost by expiring Federal tax credit, making full-year delivery goal challenging.

- Raises eyebrows at Tesla’s decision to stop reporting vehicles-in-transit metric, which in the first quarter represented 17% of quarterly shipments.

Cowen, Jeffrey Osborne

(Underperform, PT $140)

- Deliveries beat expectations, but profitability and long-term demand questions remain unanswered.

- Expects near-term boost, but shares likely to fade into earnings as attention shifts to financials, which are concerning given 2019 guidance of 360,000-400,000 units was not reiterated, and because of lack of disclosure regarding “the steady state of demand.”

- Second quarter is expected to be unprofitable with slightly negative free cash flow due to stronger margin headwinds relative to profitable quarters in 2018, as there was a shift in mix from the Model S/X to the Model 3 in addition to pricing reductions to the Model S/X.

Morgan Stanley, Adam Jonas

(Equalweight, PT $230)

- It isn’t clear how much of the beat was due to underlying demand, more attractive pricing, sales bonuses or pull-forward from third quarter after tax credit reduction.

- Based on year-to-date deliveries, if Tesla achieves 95,000 units in the third and fourth quarters it would take them to about 350,000 units for 2019, just shy of guidance of 360,000-400,000 units.

- Suggest investors get ready for a bounce, but doesn’t expect to see bears on the name capitulate; concerns about sustainable demand, competition and risks in China will weigh on stock.

Nomura, Christopher Eberle

(Neutral, PT $300)

- “Tesla noted that orders generated during the quarter exceeded deliveries, implying the company enters 3Q19 with an increase in its backlog.”

- Still, Eberle lifted his third-quarter Model 3 delivery estimate by just 5% to 80,000 units, as deliveries outpaced production in the second quarter, and the company had an additional 7,400 cars in transit at the quarter end.

JMP, Joseph Osha

(Market perform, PT $347)

- “Overall, the message we hear is that Tesla’s weak first quarter was not, in fact, an indicator of real end demand in the U.S. market. The combination of U.S. demand and export volume appears sufficient to support an outlook of ~380,000 deliveries this year, and our outlook for the second half of the year remains unchanged.”

- Osha expects to see Tesla’s cash balance rise to $2.67 billion in the second quarter, from $2.2 billion in the prior period after drawing down on inventory it had stockpiled earlier this year, and the company’s free cash flow may be running near breakeven on a normalized basis.

Loup Ventures, Gene Munster

- Deliveries “mark a turning point for underlying demand” and the record-high Model 3 production and deliveries should largely put an end to fears about weak demand.

- Expect the company to reiterate its target of a minimum of 360,000 deliveries for 2019, while investor expectations are around 300,000. Tesla should “comfortably exceed” that.

Wedbush Securities, Daniel Ives

(Neutral, PT $230 PT)

- Strong 2Q delivery numbers “a clear step in the right direction” and will help restore credibility to CEO Elon Musk’s story.

- The most important number in the release was the key Model 3 deliveries, which came in above the Street’s 74,100 estimate, as this remains the linchpin of the Tesla growth story for coming years.

Goldman Sachs, David Tamberrino and Mariel Kennedy

(Sell, PT $158)

- Second-quarter deliveries and order flow were helped by release of Tesla’s Standard Model 3 variant, right-hand drive Model 3s and the upcoming phasing out of U.S. tax incentives.

- Expects “sequential” stepdown in demand in third quarter

- Says move to offering a lower-priced Standard Model 3 variant and leasing option could have negative impacts on Model 3 program gross margins and FCF generation.

--With assistance from William Canny.

To contact the reporters on this story: Penny Peng in Beijing at ppeng18@bloomberg.net;Courtney Dentch in New York at cdentch1@bloomberg.net

To contact the editors responsible for this story: Chris Nagi at chrisnagi@bloomberg.net, Will Daley, Scott Schnipper

©2019 Bloomberg L.P.