Nerves of Steel Are Needed If Iron Rally Is Over: Taking Stock

Nerves of Steel Are Needed If Iron Rally Is Over: Taking Stock

(Bloomberg) -- Consolidation: day 11. The Stoxx Europe 600 is still stuck in a tight range as the earnings season is getting in full swing. The first results have been generally ok so far, albeit with a low bar. Looking at sector performances, the mining sector is still the top this year and miners have been partying on soaring iron ore prices. But there’s a shift in the newsflow this week, which could crash the party.

Rio Tinto was first to cut its production targets, in a widely expected move. BHP Group followed through with a similar warning. This isn’t a big deal given soaring iron ore prices were still guaranteeing a decent margin improvement that would largely compensate lower volumes and cost inflation. Vale’s unexpected swift restart of production may be a game changer.

Among the members of the Stoxx 600 basic resources index (SXPP), Rio and BHP are the most impacted by iron ore price moves, with 43 and 35 percent of 2018 revenues respectively, while Anglo American has a 13 percent exposure. Outside the sub-index, Ferrexpo is the main pure-play.

Iron ore shipment issues might not be over just yet, the risk could lie in prices getting ahead of themselves in anticipation of massive shortages that may not materialize in the end. It will impact the SXPP as Rio, BHP and Anglo have a 49 percent weight in the index. Analysts have yet to adjust their forecasts, while all three stocks already trade near or above consensus price targets.

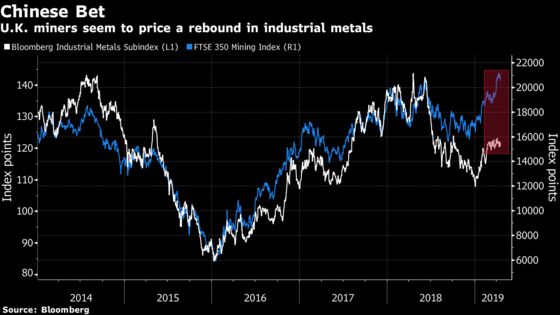

It’s not just iron ore, though. Copper is still one of the main drivers of miners’ performance. Prices stalled since the end of February, but seemed to have broken out yesterday. Voices are also warning that the market will go into deficit this year. In fact, opportunities might arise from other metals’ moves, especially as China’s growth held unexpectedly well in the first quarter, and further stimulus measures are still on the table.

HSBC analysts wrote in a note this week that EPS sensitivity is relatively high to base metals for South32 and Glencore, seeing significant potential EPS upside from spot in aluminium, copper, nickel and thermal coal prices. Both stocks have substantial leverage to changes in these commodities’ spot prices, they said.

In the meantime, Euro Stoxx 50 futures are trading down 0.3% ahead of the open, while investors are getting more skeptical about the rally, seeing the Stoxx Europe 600 falling almost 9 percent by the end of the year, as our latest survey shows.

SECTORS IN FOCUS TODAY:

- Watch aluminum-exposed miners after Alcoa cut its aluminum demand outlook but the metal rallied on falling stockpiles in China. Watch Rio Tinto, which generates about 29% of group revenue from aluminum, and South32, which makes about 27% in group revenue from the metal, as well as aluminum pure-play Norsk Hydro.

- Watch Samsung suppliers after some test models of the company’s new foldable phone suffered defects after only days of use. Watch STMicroelectronics, Siltronic, ASML, Aixtron, Infineon and Dialog Semi.

- Watch trade-sensitive stocks after the U.S. trade gap narrowed to an eight-month low following a surge in aircraft exports, a measure likely to come under pressure amid the woes faced by Boeing Co. which has increased optimism about the U.S. GDP outlook. All eyes on a planned deal announcement in early May.

- Watch U.K. stocks after the head of a manufacturing industry lobby group said he could see “no good news” in the extension to the Brexit deadline and U.K. house prices stagnated in March as the number of home transactions dropped, blamed, as much is, on Brexit-related anxiety.

COMMENT:

- “De-equitisation remains a key global investment theme for the next 12-18 months,” Citi strategists write in a note. “As the cost of equity remains high relative to the cost of debt, it makes sense for companies to de-equitise – use cheap financing to buy back their own shares. Since 2011, global non-financial corporates have bought back ~$4.8trn of their own shares, equivalent to 15% of average market cap over the period.”

COMPANY NEWS AND M&A:

- Kering’s Sales Narrowly Beat Estimates as Gucci Growth Cools

- Deutsche Bank Processed EU175m in Dirty-Money Saga: FT

- Nestle First0Quarter Organic Revenue Beats Estimates

- Pernod Ricard Raises Profit Goal to Top End of Range

- Schneider Electric 1Q Rev. EU6.31B; Est. EU5.25B

- Edenred 1Q Total Rev. up 14.1% Lfl to EU383M

- Saipem First-Quarter Revenue 4.3% Above Estimates

- Watch Galp Energia Shares as Portuguese Trucker Strikes Bite

- Spain’s Repsol Suspends Swap Deal for Venezuela’s Oil: Reuters

- Lonza Portfolio Review Continues; Forecasts Confirmed

- LafargeHolcim Proposes New Board Members, Details Dividend

- Genfit Says Elafibranor Won FDA Breakthrough Therapy Designation

- Democrats Said to Subpoena Nine Banks in Probe of Trump Finances

- First Japan-Built Airliner in 50 Years Takes on Boeing, Airbus

- Proximus Won’t Cut Dividend to Save on Costs: L’Echo

- BoomBit’s IPO Miss Confirms Warsaw Market Remains Lethargic

NOTES FROM THE SELL SIDE:

- Morgan Stanley says EssilorLuxottica’s initiation of a search for a future CEO should be “taken well” by investors, given recent corporate governance problems at the newly merged French and Italian eye-wear company. Keeps an equal-weight rating as further clarity will be required for investors to fully regain confidence on the governance situation.

- Kering’s first-quarter results came in ahead of its industry but not the analyst consensus, Citi wrote in a note, adding that it may not be enough for further earnings momentum and re-rating.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July high); 403.7 (100% Fibo)

- Support at 385.7 (76.4% Fibo); 374.5 (61.8% Fibo)

- RSI: 68.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,516 (76.4% Fibo); 3,596 (May high)

- Support at 3,403 (61.8% Fibo); 3,309 (50% Fibo)

- RSI: 72.4

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Countryside upgraded to neutral at JPMorgan; PT 3.75 Pounds

- Grammer upgraded to hold at Quirin Privatbank AG; PT 38 Euros

- ING FP raised to overweight at Morgan Stanley; PT 78 Euros

- Ludwig Beck upgraded to buy at Montega; PT 35 Euros

- Vopak upgraded to hold at Bank Degroof Petercam; PT 43 Euros

DOWNGRADES:

- ASML downgraded to hold at Nord/LB; Price Target 195 Euros

- Atlas Copco cut to reduce at Kepler Cheuvreux; PT 247 Kronor

- Ericsson Downgraded to Sell at SEB Equities; PT 70 Kronor

- KWS Saat downgraded to hold at Nord/LB; Price Target 65 Euros

- Nordex downgraded to neutral at Goldman; PT 15.30 Euros

- Proximus downgraded to neutral at JPMorgan; PT 25 Euros

INITIATIONS:

- Fluxys Belgium rated new buy at Kepler Cheuvreux; PT 28.50 Euros

- Medicrea rated new buy at Kepler Cheuvreux; PT 3.15 Euros

- Securitas reinstated underweight at Morgan Stanley

MARKETS:

- MSCI Asia Pacific up 0.2%, Nikkei 225 down 0.8%

- S&P 500 down 0.2%, Dow little changed, Nasdaq down 0.1%

- Euro up 0.04% at $1.13

- Dollar Index down 0.02% at 96.99

- Yen up 0.16% at 111.88

- Brent down 0% at $71.6/bbl, WTI little changed at $63.8/bbl

- LME 3m Copper down 0.4% at $6530/MT

- Gold spot down 0.1% at $1272.5/oz

- US 10Yr yield down 3bps at 2.57%

MAIN MACRO DATA (all times CET):

- 9:15am: (FR) April Markit France Manufacturing PMI, est. 50, prior 49.7

- 9:15am: (FR) April Markit France Services PMI, est. 49.8, prior 49.1

- 9:15am: (FR) April Markit France Composite PMI, est. 49.7, prior 48.9

- 9:30am: (GE) April Markit/BME Germany Manufacturing PMI, est. 45, prior 44.1

- 9:30am: (GE) April Markit Germany Services PMI, est. 55, prior 55.4

- 9:30am: (GE) April Markit/BME Germany Composite PMI, est. 51.7, prior 51.4

- 10am: (EC) April Markit Eurozone Manufacturing PMI, est. 48, prior 47.5

- 10am: (EC) April Markit Eurozone Composite PMI, est. 51.8, prior 51.6

- 10am: (IT) Feb. Industrial Sales WDA YoY, prior 0.6%

- 10am: (IT) Feb. Industrial Sales MoM, prior 3.1%

- 10am: (IT) Feb. Industrial Orders NSA YoY, prior -1.2%

- 10am: (IT) Feb. Industrial Orders MoM, prior 1.8%

- 10am: (EC) April Markit Eurozone Services PMI, est. 53.1, prior 53.3

- 10:30am: (UK) Bank of England Credit Conditions & Bank Liabilities Surveys

- 10:30am: (UK) March Retail Sales Ex Auto Fuel MoM, est. -0.3%, prior 0.2%

- 10:30am: (UK) March Retail Sales Ex Auto Fuel YoY, est. 4.0%, prior 3.8%

- 10:30am: (UK) March Retail Sales Inc Auto Fuel MoM, est. -0.3%, prior 0.4%

- 10:30am: (UK) March Retail Sales Inc Auto Fuel YoY, est. 4.5%, prior 4.0%

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.