Corporate Executives Are Buying Stocks. Do They Know Better?

Corporate Executives Are Buying Stocks. Do They Know Better?

(Bloomberg) --

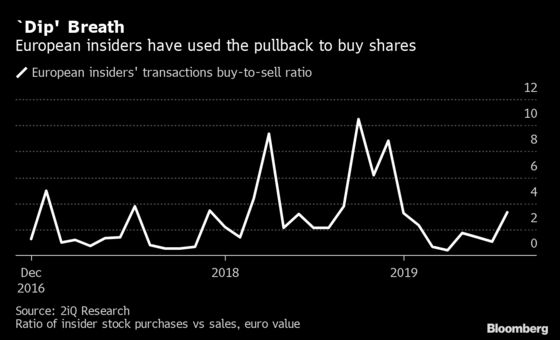

When equity markets tumbled in August, one group of investors showed unshakable confidence: company insiders. So much that the buy-to-sell ratio of corporate executives in Europe reached its highest level since December, according to data compiled by 2iQ Research.

Such spike in the ratio -- it reached 3.3 in August -- is usually seen by market strategists as a contrarian buy-signal for equities. Top-level managers are considered to have superior knowledge of their businesses, and know when their company’s stock trade at bargain prices.

When markets sank in the fourth quarter last year, insiders piled up their own stocks, with the buy-to-sell ratio surging to 10.4 in October and staying high in November and December. That was followed by a 16% rally in the Stoxx 600 in the next four months of 2019.

Last month saw “a lot of buying activity in Europe, and the U.S. too,” says Patrick Hable, managing partner at 2iQ.

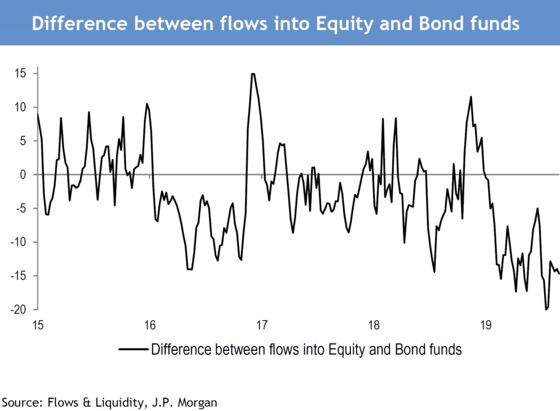

The insider buying activity contrasts with other investment flows and the light equity positioning among fund managers. JPMorgan strategists including Mislav Matejka write that they haven’t seen inflows into stocks returning, from neither retail nor institutional investors. Their prime-brokerage services indicate a subdued net exposure to shares across all regions, which could somehow limit the downside.

The strategists have just turned positive on stocks, arguing momentum has improved. They had previously called for two tactical corrections, in May and August, and now expect the market will be higher by the end of the year. Their “template” remains the 2015-2016 correction that was turned around by the Fed pausing its hikes, a peak in the dollar and Chinese stimulus -- a similar pattern to the current situation. The view concurs with another buy signal from last week, when the BofAML Bull & Bear model showed its first bullish reading since early January.

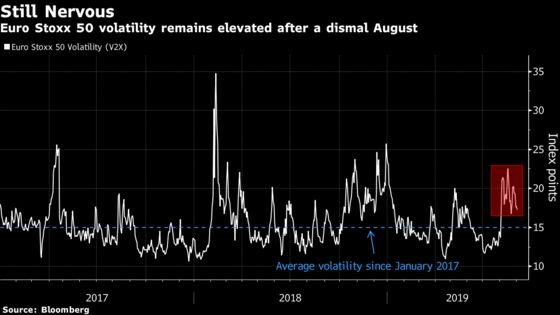

That said, many remain skeptical, particularly on the buy-side, with concerns recently expressed by UBS Wealth Management and Legal & General. The volatility of the Euro Stoxx 50 is still elevated compared to its average since 2017, as investors remain cautious about trade tensions, and await further signals from central banks.

Next week will be crucial on that front: traders expect a broad package of measures from the ECB meeting. That might be a problem, according to UBS economists, who see room for disappointment, particularly on the extent of a rate cut.

In the meantime, Euro Stoxx 50 are little changed ahead of the European open, while S&P 500 futures are down 0.7%.

- Watch U.K. retail stocks after a report from the British Retail Consortium and KPMG showed a 0.5% decline in overall like-for-like retail sales in August. Note the report comes after GfK reported U.K. consumer sentiment fell to its lowest level in six years.

- Watch the pound and U.K. stocks: Members of Parliament are planning to pass legislation Tuesday evening to force the prime minister to delay Brexit until Jan. 31 unless he can get a new agreement with the European Union by mid-October. Johnson will try to trigger a snap election on Oct. 14 if he loses the crunch vote in Parliament.

- Watch trade-sensitive sectors as Chinese and U.S. officials struggled to agree on scheduling for a planned meeting this month. That’s after Washington rejected Beijing’s request to delay tariffs that took effect over the weekend.

COMMENT:

- “In equity, while FTSE MIB seems to have lagged the rally of BTPs, this is mostly due to its sector composition, which is skewed towards banks,” Goldman Sachs strategists write in a note. “Controlling for sector exposure, the excess returns of FTSE MIB have been in line with the decline in spreads and its valuation discount does not look excessive now.”

NOTES FROM THE SELL SIDE:

- MTG is raised to equal-weight from underweight at Morgan Stanley after its portfolio company ESL said it’s partnering with streaming platform Huya in order to expand in China.

- U.K. health-care marketing and communications firm Huntsworth should benefit from various secular trends in the pharmaceutical industry and should be valued more like a health stock, RBC says in a note initiating co. at outperform with 130p PT.

- Thyssenkrupp has scope to unlock meaningful value by restructuring its portfolio, although execution risk is high and the company must address cash burn, Morgan Stanley says, resuming coverage at equal-weight.

- Enel has become leaner, with improved returns and better cash deployment, but the shares are now fully valued with little upside scope following recent interest rate declines, Berenberg says in note downgrading stock to hold from buy.

COMPANY NEWS AND M&A:

- Deutsche Boerse Regains Euro Stoxx 50 Membership After Surge

- Dealmaker Franklin Said to Near $2.9 Billion APi Group Purchase

- Just Eat Shareholder to Vote Against Takeaway.com Merger: FT

- Marks & Spencer Group May Be Demoted From FTSE 100: LSE

- Glencore Wins Tax Dispute Over Australia’s CSA Copper Mine

- Iliad First Half Ebitda Misses Estimates

- Stadler Rail Sees Full Year Ebit Margin 7%

- Home24 Sees Full Year Adjusted Ebitda Margin -6% To -9%

- Nordex: Order for 10 N133/4.8 Strong-Wind Turbines in Scotland

- Telia Offers Concessions as EU Probes Bonnier Deal: Reuters

- DNA Board Recommeds Accepting Telenor Offer; Warns on Synergies

- Sweden May Use Resolution Fee System to Introduce Bank Tax: TT

- Santhera First Half Loss CHF26.9 Mln

- Zumtobel First Quarter Net Income EU10.9 Mln

- BKW Boosts Full Year Adjusted Ebit Forecast

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 381.2 (50-DMA); 395.1 (July high)

- Support at 371.5 (200-DMA); 365.5 (50% Fibo)

- RSI: 56.7

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,435 (50-DMA); 3,515 (May high)

- Support at 3,403 (61.8% Fibo); 3,310 (200-DMA); 3,239 (June/August low)

- RSI: 56.2

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- MTG upgraded to equal-weight at Morgan Stanley; PT 100 Kronor

- Metso Oyj upgraded to buy at Kepler Cheuvreux; PT 39 Euros

- NEL upgraded to buy at SpareBank; PT 10 Kroner

- Scatec Solar upgraded to buy at Kepler Cheuvreux; PT 120 Kroner

- Telefonica upgraded to outperform at Macquarie

- UBM Dev upgraded to buy at Raiffeisen Centrobank; PT 50 Euros

DOWNGRADES:

- Dustin downgraded to hold at ABG; PT 95 Kronor

- EasyJet downgraded to reduce at Kepler Cheuvreux; PT 8.20 Pounds

- Enel downgraded to hold at Berenberg

INITIATIONS:

- Barratt Reinstated at Deutsche Bank With Hold; PT 6.48 Pounds

- Bellway Reinstated at Deutsche Bank With Buy; PT 35.38 Pounds

- Berkeley Reinstated at Deutsche Bank With Sell; PT 34.28 Pounds

- Bovis Homes Reinstated Hold at Deutsche Bank; PT 10.85 Pounds

- Countryside Reinstated at Deutsche Bank With Buy; PT 3.53 Pounds

- Crest Nicholson Reinstated Hold at Deutsche Bank; PT 3.71 Pounds

- Glaxo resumed at citi with Neutral; PT 18.40 Pounds

- Huntsworth rated new outperform at RBC; PT 1.30 Pounds

- Knorr-Bremse Rated New Sell at Bankhaus Lampe; PT 72 Euros

- McCarthy & Stone Reinstated Hold at Deutsche Bank

- Persimmon Reinstated at Deutsche Bank With Buy; PT 23.86 Pounds

- PVA TePla rated new buy at Deutsche Bank; PT 18 Euros

- Redrow Reinstated at Deutsche Bank With Buy; PT 7.28 Pounds

- Sanofi Rated New Outperform at Bernstein; PT 95 Euros

- ThyssenKrupp resumed equal-weight at morgan Stanley

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 up 0.1%

- S&P 500 up 0.1%, Dow up 0.2%, Nasdaq down 0.1%

- Euro down 0.21% at $1.0947

- Dollar Index up 0.36% at 99.27

- Yen little changed at 106.24

- Brent little changed at $58.7/bbl, WTI down 0.4% to $54.9/bbl

- LME 3m Copper up 0.2% at $5633/MT

- Gold spot down 0.2% at $1526.5/oz

- US 10Yr yield up 2bps at 1.52%

ECONOMIC DATA (All times CET):

- 9am: (SP) Aug. Unemployment Change, prior -4,253

- 10:30am: (UK) Aug. Markit/CIPS UK Construction PMI, est. 46.5, prior 45.3

- 11am: (EC) July PPI MoM, est. 0.2%, prior -0.6%

- 11am: (EC) July PPI YoY, est. 0.2%, prior 0.7%

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.