IPO Values Are the Other Thing That Sank in 2018: Taking Stock

IPO Values Are the Other Thing That Sank in 2018: Taking Stock

(Bloomberg) -- U.S. stocks closed at their lowest level since April on Friday, on mounting concerns about the economy. U.S. futures are bouncing this morning, while stocks are trading mixed in Asia. Euro Stoxx 50 futures are trading up 0.2% ahead of the European open.

The volatility this year hasn’t just been bad for the listed stocks -- it’s also been an ugly period for initial public offerings in Europe. Everything turned against European stock issuers this year: growth started slowing, global markets collapsed, U.S. President Trump’s trade tweets, Italy’s struggles and Brexit spooked investors. Plus, investors just aren’t sticking around: no other major region in 2018 has seen such a mass exodus of equity investors, with European stock funds losing about $67 billion in outflows this year.

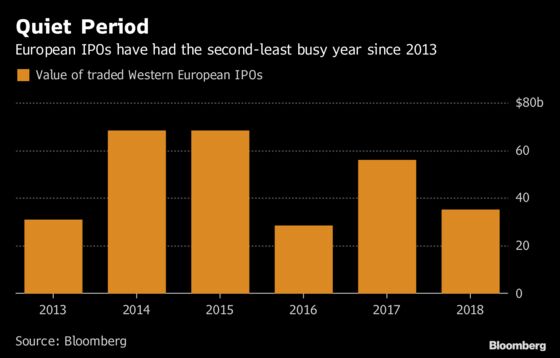

Europe welcomed just $35 billion worth of new European company listings this year, a drop of 37 percent compared with last year. That’s making 2018 the second-weakest year in terms of IPOs by value since 2013 (yes, it’s hard to imagine, but 2016 was even worse), data compiled by Bloomberg show.

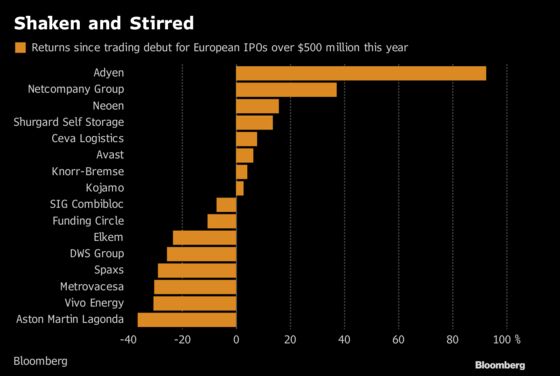

And not only were there very few IPOs, but the brave souls that did come to the market were punished with a lackluster performance, which averaged a drop of 1.7 percent. (To be fair, that’s still much better than the Stoxx Europe 600’s slump of 11 percent.)

So what about 2019?

“Global equity volatility is set to continue next year,” Eric Arnould, global head of equity capital markets at Natixis, said in an interview. “The first quarter is likely to be rather quiet for equity deals. Issuers will wait for more clarity on geopolitics and economics and then decide when to sell shares."

The outcome of Brexit is a key event for share transactions on the entire continent, said Arnould, and the approval of a withdrawal from the European Union with a deal would bring “a big relief” to investors. However, even in the event of what he would describe as a positive Brexit outcome, IPO activity in London is set to decline, according to a report by Baker McKenzie and Oxford Economics. That would be a major blow for the country that accounted for more than a quarter of the total Western European IPO market.

If Theresa May’s deal passes through Parliament, borrowing costs in the U.K. are likely to stay low. That would support IPO activity in the coming years, but the value of offerings would still fall 16 percent in 2019 as issuers steer through the divorce, according to Baker McKenzie. However, if a no-deal Brexit occurs, U.K. equity deals will plummet by 60 percent in 2019, according to the report.

“A no-deal Brexit will exponentially increase uncertainty,” Adam Farlow, EMEA head of capital markets at Baker McKenzie, said. “This will deter listings and result in an alarming slowdown in IPO activity in 2019. Equity markets will remain cautious going forward as investors navigate from one uncertainty to another, with better prospects only from 2021.”

One of this year’s blockbuster London offerings also turned out to be Europe’s biggest flop. Aston Martin’s stands out as this year’s dog among European equity IPOs above $1 billion in value -- the stock is down about 40 percent since its October listing. The carmaker has struggled to reassure investors after selling shares on a par with larger rival Ferrari, an aspiration that’s brought immediate pressure as the Italian company is more profitable with a stronger balance sheet.

Ceva Logistics was another stock which had a disappointing performance after its debut. In a fragmented market hit by slower growth and price pressure, the Swiss company lost 33 percent of its value in just over six months of trading. It only owes its recovery to takeover attempts from Danish competitor DSV and French container line CMA CGM looking to consolidate the market.

But not every placement had a somber outcome even if the road seems often bumpy. The stock price of the Dutch payments provider Adyen has tripled this year amid appealing growth prospects, before recently paring its gains as some analysts said the valuation was stretched.

With all the issues affecting financial markets at the moment, the outlook for 2019 primary listings may appear grim. Let’s hope we’ll get some decent news by February to set the trend.

- Watch U.K. housebuilders and travel firms. Housebuilders may be active after two weak sets of data on the country’s housing market, while travel firms could also be in focus following a report of a warning for people not to book any trips due to concerns about a no-deal Brexit. Watch Housebuilders Barratt Developments, Bellway, Taylor Wimpey, Berkeley Group and Persimmon. Watch travel experts TUI, Thomas Cook, On the Beach and Saga.

- Watch the pound and U.K. equities after the team around Prime Minister Theresa May has pushed back against the notion they are warming to the U.K. holding a second referendum. May herself plans to tell Parliament today that it would be a breach of trust. Additionally, May has returned from Brussels with little to show from the trip.

- Watch Italian shares and government bonds after officials confirmed weekend reports that Italy had reached an agreement on trimming its budget deficit, though with few details of what has been agreed. This could impact Italian BTPs and cause a reaction for Italian banks including UBI Banca, UniCredit, Intesa Sanpaolo and Mediobanca and across the benchmark FTSE MIB index.

COMMENT:

- “Last week saw a net outflow of $39b from equity funds, the largest weekly outflow in dollar terms in the history of our weekly dataset,” Bernstein strategists write in a note. “Specifically, this has had a material impact on two of our sentiment indicators. Our flow indicator has dropped sharply into buy territory, while our Composite Sentiment Indicator that brings together a broader set of sentiment signals is at -0.93 standard deviations (a ‘weak buy’ signal, but close to the -1 standard deviations that we typify as a ‘strong buy’). Four out of the five inputs to our Composite Sentiment Indicator now signal a ’buy’.”

COMPANY NEWS AND M&A:

- Renault is pushing Nissan to call a shareholder meeting as soon as possible to discuss the Japanese automaker’s indictment, governance and the French company’s appointees on Nissan’s board, people familiar with the matter said.

- Hitachi is making its biggest-ever acquisition by agreeing to purchase the power grid division of ABB, a deal that’s aimed at turning the Japanese conglomerate into a top global provider of equipment for electricity networks.

- BinckBank, a Dutch online brokerage, agreed to a 424 million-euro takeover offer from closely held Saxo Bank.

- H&M Fourth Quarter Sales Miss Lowest Estimate

- Asos Cuts FY Sales Growth Outlook on ‘Significant Deterioration’

- SSE Says Deal With Innogy Not Proceeding

- Zurich to Transfer Gross Liabilities of $2b to Catalina

- BBVA to Sell Real Estate Loan Portfolio to CPPIB: Confidencial

- Investor AB Says It Supports ABB’s Divestment of Power Grids

- ForFarmers Sees ‘Modest’ Underlying Ebitda Decline in 2018

- Roche’s Risdiplam Gets EMA Priority Medicines Status

- Aasta Hansteen Gas Field Starts Production, Equinor Says

- Fabege Says CEO Hermelin to Resign Next Year

- Just Eat Shareholder Asks Board to Consider Non-Core Asset Sale

- Siemens to Build New Digital Factory in Nanjing, China

- Novartis May Team With Reinsurers to Cut Drug Costs, FT Reports

- Salini Can Rebuild Genoa Bridge in a Year, CEO Tells Repubblica

- Anglo American Request to Resume Brazil Pipeline Granted

- Subsea 7 Gets U.K. Contract With Shell for Shearwater FGL

NOTES FROM THE SELL SIDE:

- Morgan Stanley downgraded Swatch to underweight, and Richemont to equal-weight, as market is underestimating short- and medium-term pressure. The bank said supply chain inefficiencies led to significant inventory build-up across industry, particularly true to Swatch, and magnified by a structural change in the distribution channel.

- Morgan Stanley named Wirecard and Dassault Systemes as top picks in payments, software and services sector for 2019, while Worldline among several stocks cut to underweight in note.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 353.2 (50% Fibo); 362 (March low)

- Support at 341.2 (61.8% Fibo); 326.5 (74.4% Fibo)

- RSI: 42

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,181.9 (50-DMA); 3,193.5 (50% Fibo)

- Support at 3,072 (61.8% Fibo); 2,921 (76.4% Fibo)

- RSI: 43.2

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Moncler upgraded to overweight at Morgan Stanley

- Senvion upgraded to overweight at JPMorgan; Price Target 5 Euros

DOWNGRADES:

- Dometic downgraded to hold at Kepler Cheuvreux; PT 65 Kronor

- Elia downgraded to neutral at Citi

- Indra downgraded to underweight at Morgan Stanley; PT 9 Euros

- NNIT downgraded to underweight at Morgan Stanley; PT 190 Kroner

- Oriflame downgraded to add at AlphaValue

- Richemont downgraded to equal-weight at Morgan Stanley

- Salvatore Ferragamo downgraded to underweight at Morgan Stanley

- Sopra Steria cut to underweight at Morgan Stanley; PT 75 Euros

- Swatch downgraded to underweight at Morgan Stanley

- Worldline cut to underweight at Morgan Stanley; PT 43 Euros

- Zealand Pharma downgraded to neutral at Goldman; PT 92 Kroner

INITIATIONS:

- Central Asia Metals rated new outperform at RBC; PT 2.80 Pounds

- Garofalo Health Care rated new neutral at Credit Suisse

- Gresham House rated new buy at Jefferies; PT 6.40 Pounds

- KAZ Minerals rated new sector perform at RBC; PT 5.90 Pounds

- Novozymes rated new hold at Kepler Cheuvreux; PT 280 Kroner

- SMCP rated new hold at Jefferies; PT 17.20 Euros

- Scandic rated new buy at Kepler Cheuvreux; PT 105 Kronor

- Solvay rated new hold at Berenberg

MARKETS:

- MSCI Asia Pacific down 1.4%, Nikkei 225 up 0.6%

- S&P 500 down 1.9%, Dow down 2%, Nasdaq down 2.3%

- Euro up 0.05% at $1.1312

- Dollar Index down 0.02% at 97.42

- Yen down 0.06% at 113.46

- Brent down 0.2% at $60.2/bbl, WTI up 0.1% to $51.2/bbl

- LME 3m Copper up 0.2% at $6142/MT

- Gold spot down 0.1% at $1237.5/oz

- US 10Yr yield little changed at 2.89%

MAIN MACRO DATA (all times CET):

- 10am: (IT) Oct. Trade Balance Total, prior 1.27b

- 11am: (EC) Oct. Trade Balance SA, prior 13.4b

- 11am: (EC) Nov. CPI YoY, est. 2.0%, prior 2.2%

- 11am: (EC) Nov. CPI MoM, est. -0.2%, prior 0.2%

--With assistance from Hanna Hoikkala.

To contact the reporters on this story: Ksenia Galouchko in London at kgalouchko1@bloomberg.net;Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2018 Bloomberg L.P.