Distressed Debt Gurus Get a 90 Percent Scorching

Distressed Debt Gurus Get a 90 Percent Scorching

(Bloomberg Opinion) -- When a company’s bonds trade near 30 cents on the euro, that would usually be the moment for distressed debt specialist Centerbridge Partners to show up and put the heat on the owners. The private equity firm holds some of bankrupt U.S. utility PG&E Corp.’s notes, for example.

But Centerbridge has found itself on the other side of the table in the case of the struggling wind turbine manufacturer Senvion SA. It is the owner of the listed German company.

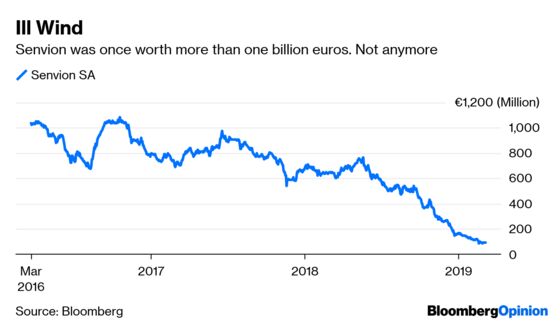

A succession of profit warnings and worries about Senvion’s financial stability have wiped out more than 90 percent of the value of the Centerbridge funds’ majority equity stake. Meanwhile, the manufacturer’s 400 million euros ($452 million) of 3.875 percent coupon bonds, due in 2022, yield a staggering 40 percent.

Talks with the lending banks and bondholders now loom large and Centerbridge may have to sink more money into the company. It shouldn’t dally too long.

Centerbridge bought Senvion from India’s Suzlon Energy Ltd. in 2015 for about 1 billion euros, when the seller was trying to cut its large debt load. Together with co-investor Arpwood Partners, the private equity firm sold about one-quarter of the shares to investors the following year, allowing Centerbridge to recoup some of its original equity outlay. Since then, Senvion’s problems have piled up.

Competition has intensified in the wind farm industry and contract auctions have put downward pressure on pricing. Senvion has already closed several factories and cut hundreds of jobs.

Last year the company compounded its troubles by failing to deliver projects on time, triggering penalty payments and a big jump in working capital. It’s had bad luck too. The discovery of a live bomb from World War II held up installation at one of its sites. The chief executive and finance director have been replaced.

In February, Senvion said it had commissioned a restructuring opinion and would delay the publication of its full-year earnings. It had almost 150 million euros of cash at the end of September, but a 125 million-euro revolving credit line has since been drawn, which suggests liquidity became tight. Net debt is at least 5.5 times 2018 Ebitda, estimates Remi Ramadou of Spread Research.

The company and its lenders have hired financial advisers and lawyers, Bloomberg News has reported, cementing the impression that a capital restructuring lies ahead. In view of Centerbridge’s debt expertise and the likelihood that hedge funds now hold quite a lot of the distressed bonds, the restructuring talks should be lively.

Senvion needs financial relief but it’s not clear who’s going to provide it and on what terms – hence the sorry state of the bonds. It raised 62.5 million euros in fresh capital from Centerbridge and others last year but it has burned through much of that.

The liquidity pressures should ease once delayed orders are completed, inventory decreases and customer payments are received. However, Senvion is smaller than market leaders such as Vestas Wind Systems A/S, General Electric Co. and Siemens Gamesa Renewable Energy SA, which might make it difficult to achieve the economies of scale needed to stay competitive. While it has won orders in places like India and Chile, its sales are too skewed toward stagnating European markets.

Centerbridge has publicly backed the new management’s turnaround plan, but hasn’t yet matched that rhetoric with more funds. Writing a check would avert the risk that Senvion’s customers use the restructuring as a pretext to try to recoup project prepayments from its banks. The company has a 825 million euro letter of guarantee facility, which might allow just that. And more than half of it has been pledged, according to Jefferies analyst Stephen Lienert.

The fact that Centerbridge hasn’t yet stumped up the extra cash might indicate that it wants more breathing space from the banks and for bondholders to take a haircut, perhaps in return for equity. It’s also possible that a white knight will emerge – the wind-turbine servicing contracts might be attractive – but any bidder may wait to see if Senvion fails first.

Another option is for Centerbridge to buy some of the company’s debt itself, an approach that investment firm Brait SE took during the restructuring of British retailer New Look. Those involved shouldn’t hang around. Senvion depends on cash advances from customers when they place orders. The longer its bonds look distressed, the bigger the chance that clients will shop elsewhere.

Wind turbines are rightly beloved by those still hoping we can avoid the cataclysm of an over-heating planet. In this case, though, it’s private equity that’s been scorched.

Centerbridge was forced to scale back its ambitions. The owners originally hoped to raise as much as 700 million euros but the share sale brought in just 294 million euros.

The guarantees are senior to Senvion’s high-yield bond. It’s probable, though, that any customers who did ask for their money back would be hit with a break-fee, which might deter some of them.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.