Companies Seem Unable to Provide a Quality Beat: Taking Stock

Companies Seem Unable to Provide a Quality Beat: Taking Stock

(Bloomberg) -- About half-way into this earnings season, it’s time for a health check. We’ve seen a flurry of bad headlines -- with Bayer saying this morning its outlook for the year is “increasingly ambitious,” but we also got good figures from the likes of Nestle and Sanofi. Overall, the numbers don’t look too bad, although the bar was set low. Better-quality beat could be key to get the Stoxx 600 out of its recent range.

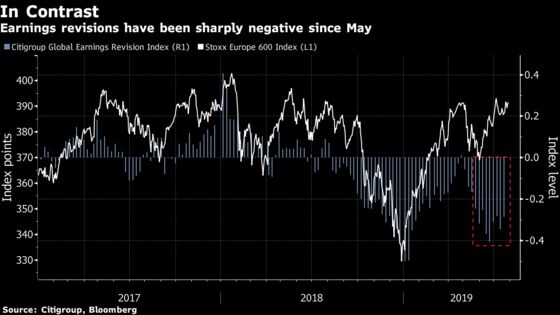

The second-quarter earnings breadth, the strongest in two years, is largely due to a 5% downgrade of estimates ahead of the start of the season, Morgan Stanley say. Looking at the earnings revision index, analysts have been busy trimming forecasts since late May, but the market rose over the same period. That’s in sharp contrast to what happened during last year’s fourth-quarter.

Morgan Stanley strategists write that earnings revisions in Europe have kept deteriorating, not only on second-quarter earnings but also on estimates for the rest of the year, with all major sectors seeing cuts.

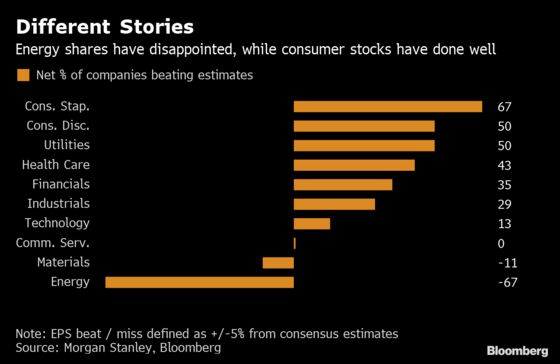

Given the amplitude of the downgrades ahead of the season, the earnings beat on aggregate is a low quality one, the strategists say. About 43% of companies have beaten EPS estimates by 5% or more, and only 21% have missed overall, but there are also sharp differences between sectors. Staples, health care and consumer discretionary have shown the best performances so far, while energy and materials have been weak.

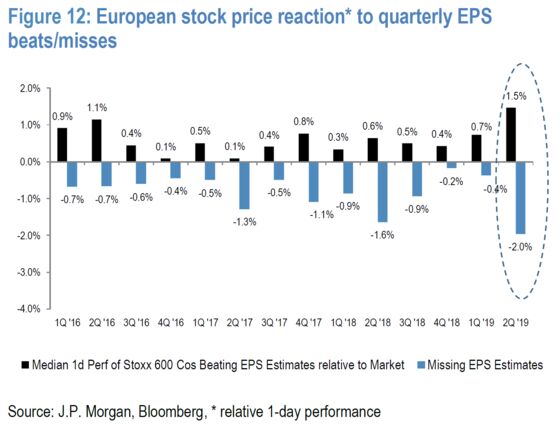

The low bar could also help explain why companies are being punished harshly when they miss. Barclays strategists highlight stock price reaction is so far “asymmetric to the downside” in Europe. An analysis shared by JPMorgan strategists, who note that earnings-day moves are the sharpest since 2016.

Earnings beats can’t hide the harsh reality that European EPS are set for another quarter of negative growth. After a 5.1% drop in the first quarter, they are down 4.8% so far this quarter, with 5 out of 11 sectors experiencing a drop in profits, according to Morgan Stanley, with financials and commodities-related sectors being hit the most.

In the meantime, Euro Stoxx 50 futures are little changed ahead of the open.

- Watch investment banks after people familiar with the matter said Citigroup is set to cut hundreds of trading jobs. Watch for any read-across for Deutsche Bank, BNP Paribas, UBS, Barclays and Societe Generale.

- Watch the pound and U.K. stocks after Boris Johnson told the EU that talks on reaching a new Brexit deal won’t start again until the previously rejected divorce agreement is reopened, something the EU has consistently said it has no intention of doing. The pound dropped to the lowest in more than two years and the BOE could put yet further pressure on the currency too when it makes its rate decision this week.

COMMENT:

- “With global growth slowing to around 2.75%, in the first half of the year there has been a synchronized tilt toward easier central banks’ policies,” Goldman Sachs strategists write in a note. “However, at this stage markets have already discounted much easier monetary policy and raised the expectations for central banks to deliver. Moreover, recent improvements in US growth data could increase the risk of the Fed underdelivering relative to market pricing.”

COMPANY NEWS AND M&A:

- Lufthansa 2Q Adj. Ebit Declines 25% on Fuel Costs, ’Price War’

- Sanofi, Novo Nordisk Receive Subpoenas Over Insulin Prices (1)

- Bayer 2Q Sales Miss Ests; 2019 Outlook ’Increasingly Ambitious’

- Bayer Accused of Flea Repellent Monopoly in $114 Million Suit

- Legrand 1H Adj. Oper. Profit Rises 6%; Confirms FY Targets

- Fresenius Ups FY Rev. Forecast, Fresenius Medical Keeps Outlook

- Dialog Semi Second Quarter Adjusted EPS Beats Highest Estimate

- Siemens Gamesa 3Q Underlying Ebit Misses Lowest Est.

- Air Liquide Says Confident Can Deliver FY Profit Growth Ex-Fx

- Deutsche Bank Sets Sept. Deadline for Derivatives Book Bids: FT

- SAP To Restructure Flagship S/4 Hana Software: Handelsblatt

- PSA Says Car Cos That Miss Carbon Goals At Risk of Takeover: FT

- Rexel 1H Net Income EU163.9M, up 71%; FY Targets Confirmed

- Delivery Hero First Half Revenue EU581.7 Mln, +63% Y/y

- Schaeffler Group Cuts 2019 Revenue Growth Forecast

- Sandvik CEO Is Said to Emerge as Front-Runner for Top Job at ABB

- GAM Names Peter Sanderson CEO; 1H IM net outflows CHF7.6b

- Capgemini First Half Operating Profit EU658 Mln

- HeidelbergCement 2Q Profit Beats on Price Increases and Asia

- Dufry First Half Sales Meet Estimates

- Bawag ‘on Track’ for Goals After 2Q Profit Beats Estimates (1)

NOTES FROM THE SELL SIDE:

- The London Stock Exchange combining with Refinitiv "likely eliminates" an Intercontinental Exchange/LSE merger scenario, at least near-to-medium term, Citi writes in a note.

- Prudential is expected to formally announce plans to de-merge its U.K. business at its 1H results and this could prove a catalyst for the shares to start closing the gap with the sum-of-the-parts valuation, Morgan Stanley (overweight) writes in a note.

- Schaeffler yesterday became the latest auto supplier to issue a profit warning, with Citi saying that the company has “unsurprisingly followed suit”; its new guidance implies a 15% cut at bottom end of range. Broker says more earnings disappointments may be on the way.

- Berenberg cut Asos to hold from buy with PT slashed to 2,500p from Street-high 4,000p following the company’s latest profit warning, as the broker assesses general retail sector in note. Asos joins Next and Superdry at hold, with H&M, Inditex, Marks & Spencer and Zalando at sell, and AB Foods now the only buy.

- Citi initiates Philips at buy, saying it’s confident in the sustainability of strong momentum in diagnosis and treatment, as well as a recovery in personal health. Price target is set 49 euros, which is higher than any of the 22 analysts surveyed by Bloomberg.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 385.7 (76.4% Fibo); 382.9 (50-DMA)

- RSI: 59.9

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,549 (July high); 3,596 (May 2018 high)

- Support at 3,439 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 59.1

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Tikkurila upgraded to buy at SEB Equities; Price Target 16 Euros

DOWNGRADES:

- Asos downgraded to hold at Berenberg

- Domino’s Pizza Group downgraded to add at Peel Hunt

- Fevertree Drinks downgraded to sector perform at RBC

- Oerlikon downgraded to hold at Baader Helvea; PT 12.50 Francs

INITIATIONS:

- Akasol rated new neutral at MainFirst; PT 51 Euros

- Philips rated new buy at Citi; PT 49 Euros

- Smart Metering rated new buy at Citi; PT 7.90 Pounds

- Swiss Re rated new equal-weight at Morgan Stanley

- Ubisoft resumed at keybanc with Overweight; PT 94 Euros

MARKETS:

- MSCI Asia Pacific down 0.5%, Nikkei 225 up 0.3%

- S&P 500 down 0.2%, Dow up 0.1%, Nasdaq down 0.4%

- Euro down 0.07% at $1.1137

- Dollar Index up 0.14% at 98.18

- Yen up 0.16% at 108.61

- Brent up 0.6% at $64.1/bbl, WTI up 0.6% to $57.2/bbl

- LME 3m Copper down 0.1% at $6009/MT

- Gold spot down 0.2% at $1423.7/oz

- US 10Yr yield down 1bp at 2.06%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) June Consumer Spending MoM, est. 0.2%, prior 0.4%

- 8:45am: (FR) June Consumer Spending YoY, est. 0.0%, prior -0.1%

- 8:45am: (FR) June Budget Balance YTD, prior -83.9b

- 11am: (EC) July Economic Confidence, est. 102.6, prior 103.3

- 11am: (EC) July Industrial Confidence, est. -7.0, prior -5.6

- 11am: (EC) July Services Confidence, est. 10.6, prior 11

- 11am: (EC) July Consumer Confidence, est. -6.6, prior -6.6

- 11am: (EC) July Business Climate Indicator, est. 0.1, prior 0.2

- 2pm: (GE) July CPI MoM, est. 0.3%, prior 0.3%

- 2pm: (GE) July CPI YoY, est. 1.5%, prior 1.6%

- 2pm: (GE) July CPI EU Harmonized MoM, est. 0.3%, prior 0.3%

- 2pm: (GE) July CPI EU Harmonized YoY, est. 1.2%, prior 1.5%

* For a wrap on developments in Europe’s equity capital markets, click here.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editor responsible for this story: Blaise Robinson at brobinson58@bloomberg.net

©2019 Bloomberg L.P.