Apple Analysts See China iPhone Demand Tested by Trade Dispute

The iPhone is critically important to Apple’s fortunes, accounting for more than 60% of the company’s 2018 revenue.

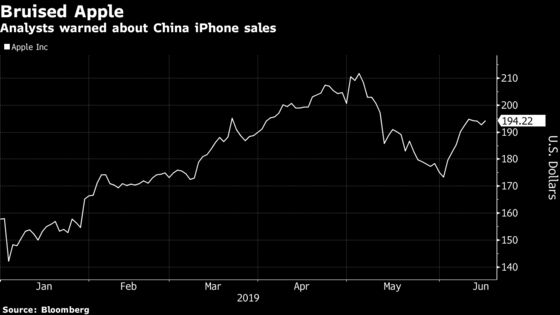

(Bloomberg) -- Apple Inc. could be seeing weaker-than-expected demand for its iPhone product line, especially in China, where trade tensions have been weighing down sales, analysts said on Monday.

Shares of Apple rose 0.7%, rebounding after a three-day decline. While the stock is up about 12% from a low hit earlier this month, Apple is still down more than 8% from a peak in early May.

JPMorgan wrote that macroeconomic uncertainty “is likely to drive greater headwinds to the smartphone market.” The bank lowered its iPhone shipment forecasts for the second quarter through the fourth quarter, dropping them by 4% to 139.5 million units. Analyst Samik Chatterjee also trimmed his price target by $2 to $233, although he kept his overweight rating.

The macro issues are “cyclical and likely resolved with a trade resolution,” Chatterjee wrote, adding that Apple could see a tailwind from its growing services business.

The iPhone is critically important to Apple’s fortunes, accounting for more than 60% of the company’s 2018 revenue, according to data compiled by Bloomberg. The company derived nearly 20% of last year’s revenue from China, and weakness there pushed Apple to cut its sales forecast in January.

JPMorgan was not the only firm to express caution about the outlook for iPhone sales on Monday. Longbow Research wrote that “concerns are rising that the ban on sales to Huawei will further impair iPhone demand in China,” and that there was a risk Apple “will not see notable share gains outside of China.” Analyst Shawn Harrison has a neutral rating on Apple, and wrote that the company’s efforts “to expand the reach and breadth of its services is key amidst a challenged iPhone demand environment, particularly in China.”

Loop Capital Markets wrote that while iPhone unit demand was “well aligned with Street expectations” for June, consensus forecasts were “too high” for the second half of the year.

“We continue to believe that risk remains to iPhone revenue through the year from mix (both units and capacity per unit), but with a stabilizing China,” analyst Ananda Baruah wrote, affirming Loop’s hold rating and $190 price target.

A more optimistic view on the iPhone came from Credit Suisse, which wrote that China iPhone sales were becoming “less bad.”

“The pace of decline for iPhone shipments in China has significantly improved” so far this quarter, analyst Matthew Cabral wrote, touting the impact of price cuts. But he noted that units were still down 4% this quarter compared with the year-ago period, and that iPhones were “lagging the overall Chinese smartphone market.”

While “less bad” is a “clear positive given the magnitude of the prior headwind, risk remains,” he wrote. Credit Suisse has a neutral rating and $209 price target.

Cabral expects trade-related uncertainty will keep the stock within a range, but that risks are “skewed to the downside.”

Even beyond trade, he added that “aggressive local competition and a narrower ecosystem advantage in China remain deeper structural challenges for Apple, with no easy near-term fix.”

To contact the reporter on this story: Ryan Vlastelica in New York at rvlastelica1@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Scott Schnipper

©2019 Bloomberg L.P.